It’s that time of year when we dust off the crystal ball and take a look at what markets are likely to do in 2024. There are plenty of unknowns amongst fundamental drivers of sheep and lamb markets, but at least supply is something we can get some sort of handle on.

Looking back at the

forecast produced at this time last year is a little embarrassing. Lamb and mutton prices had fallen, and we

were forecasting a year of consolidation.

What we got was a year of further declines, reaching levels not seen for

seven or eight years.

Massive increases in

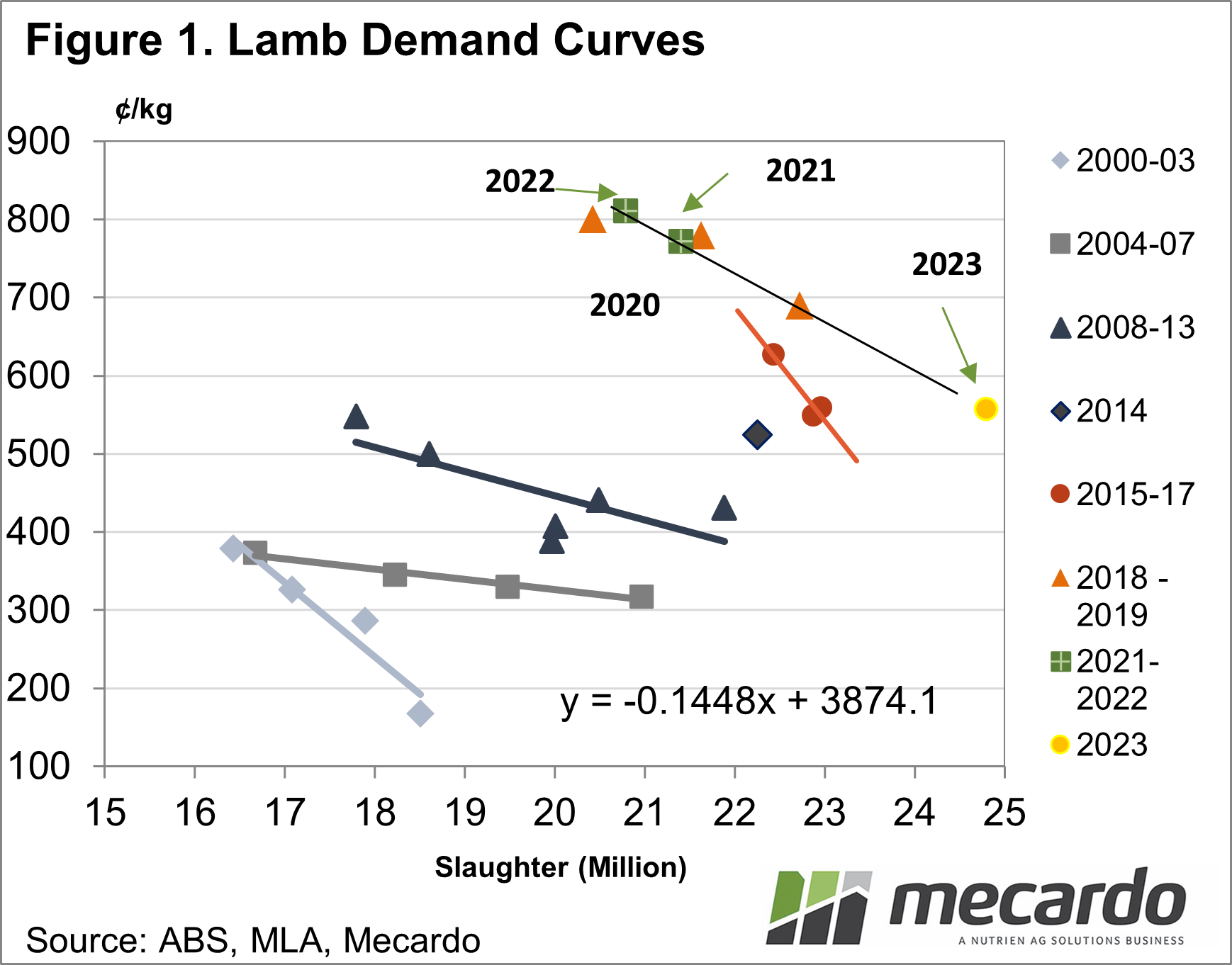

supply, combined with shifting demand have been the drivers of the lows. Figure 1, which we wheeled out a fortnight

ago shows much of the decline can be attributed to supply. The question now is where lamb will sit on

this curve next year, driven by the supply of lambs.

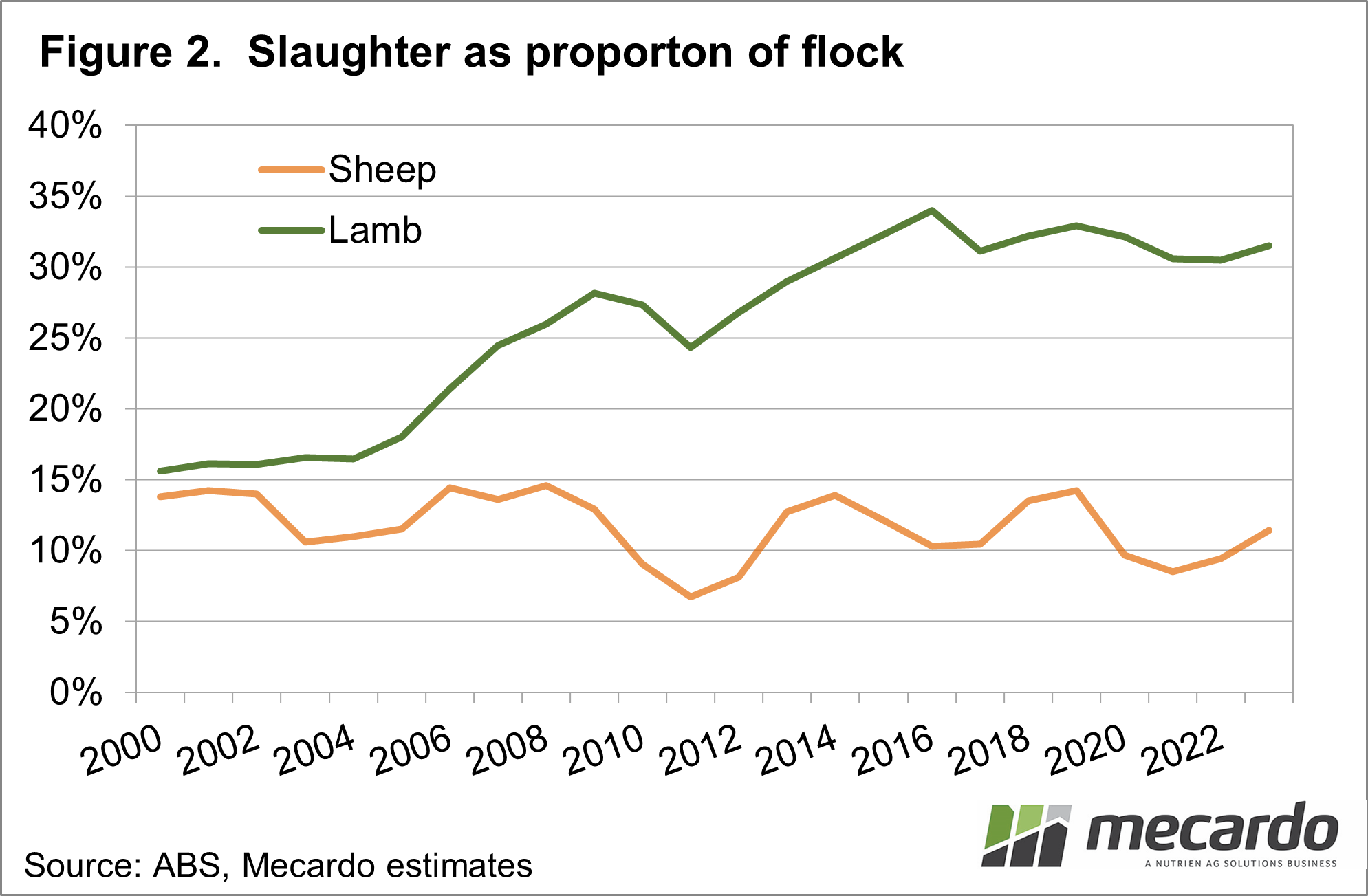

The main driver of

lamb supply is the size of the flock.

Figure 2 shows lamb and sheep slaughter as a proportion of the flock. Despite the stronger slaughter levels of

2023, the rapid increase in the size of the flock to 78 million head in recent

years means we are not really at strong liquidation levels, but we might see a small

decline. We’ll know more when official

flock numbers for 2023 are released in January.

Marking rates are the

other major driver of lamb supply. Good

seasons have led to a couple of years of strong lamb marking rates. The recent dry has been replaced by good

rains, which could boost conception rates for early lambs. There is, however, plenty to play out with seasonal

conditions from here.

We know from previous

downturns that prices rarely bounce back to highs in the short term. Back in 2013, it took 2 and a half years to

regain peaks, with relatively steady prices thereafter, with the usual seasonal

variation.

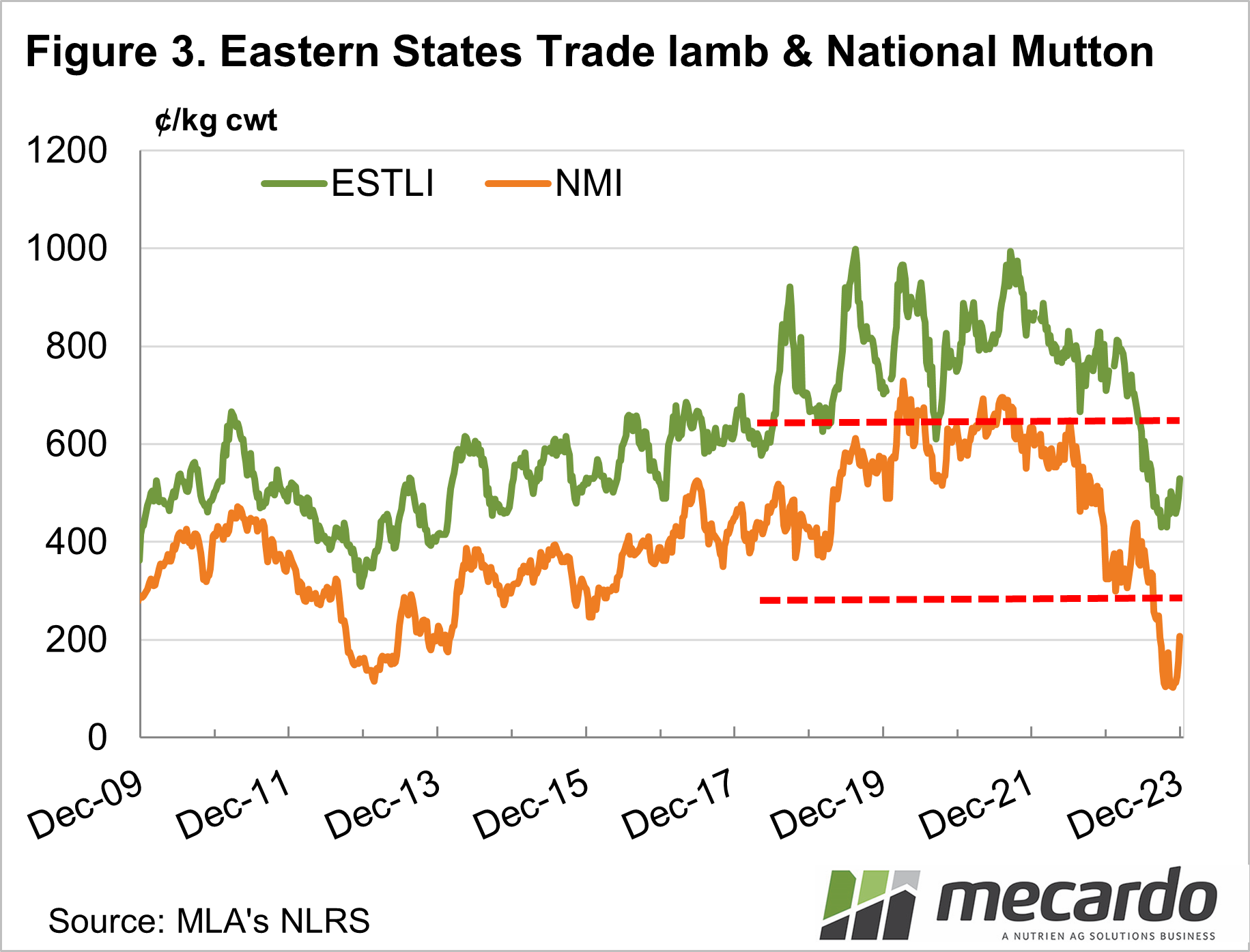

With better alignment of

supply and demand in 2024, we could potentially see a 50% retracement of 2023

falls. This would put the Eastern States

Trade Lamb Indicator (ESTLI) around an average of 625¢/kg cwt. Mutton prices around 300¢/kg cwt are nothing

like the good times, but certainly better than the $1 doldrums of the spring

just gone.

What does it mean?

Going back to Figure 1 an ESTLI at 650¢/kg will require slaughter around a million head lower than this year. This is probable, given the number of ewe lambs and merinos which have made their way to market this spring, and the need to hold more young sheep in flocks.

On the mutton front, hopefully, heavy liquidation is behind us, and we’ll see more balance between supply and demand in 2024. Prices around 300¢ are not great, but it’s not giving them away.

Have any questions or comments?

Key Points

- Heavy supply and shifting demand caused the 2023 ovine price crash.

- The coming year should see supply and demand move towards more balance.

- A 50% recovery of 2023 falls will see more reasonable rates for lamb and mutton.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: MLA, ABS, Mecardo