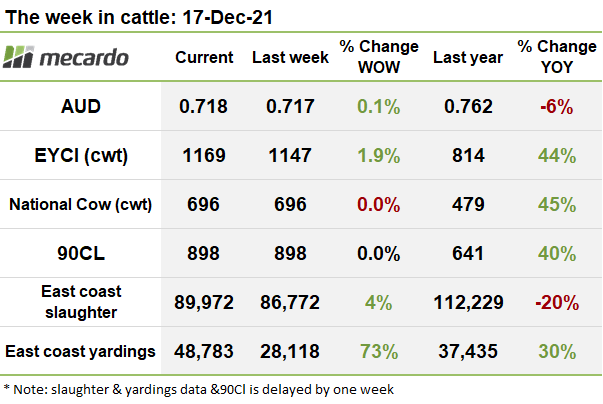

The cattle market in Australia has been red hot this year (and last year) and The Eastern Young Cattle Indicator (EYCI) has been the barometer, more than doubling since the end of 2019. And this week was no exception finishing the year on an all-time high - 1169¢/kg cwt.

The top saleyard contributing to the Eastern States Young Cattle Indicator (EYCI) was Dalby this week contributing the most head of cattle (21%) at an average of 1203¢/kg cwt. Roma Store which has been at the top of contributions more often than not for the past month, contributed 18% of EYCI eligible cattle and clocked the highest average prices for the week, at 1272¢/kg cwt. Gunnedah & Wagga were the 3rd & 4th highest contributors at 10% a piece, with averages prices north of 1,100¢/kg cwt.

Over in the west, the Western Young Cattle Indicator (WYCI) fell 29 cents on last week and is now at 1101¢/kg cwt, with just over 1,500 head the total 7-day rolling average on offer there.

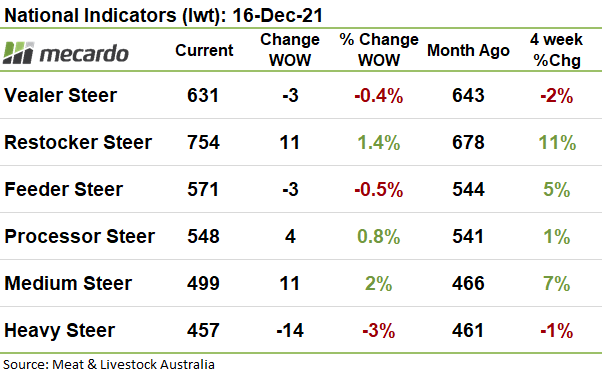

Looking at the National Indicators and there were mixed results. Restocker & Medium Steers posted the largest gains, lifting 11 cents each to finish the year on 754¢ & 499¢/kg lwt respectively. Processor Steers also lifted, by 4 cents, to 548¢/kg lwt. Meanwhile Heavy Steers dropped 14 cents to 457¢/kg lwt. The Vealer & Feeder Steer indicators dropped by 3 cents each to settle at 631 & 571¢/kg lwt.

In terms of supply, we saw a big lift on the east coast, with 48,783 head of cattle yarded for the week ending 10th of December 2021, over 20,000 or 73% more than the week prior. The biggest lifts in yardings came from QLD and NSW which saw an extra 10,000 cattle each.

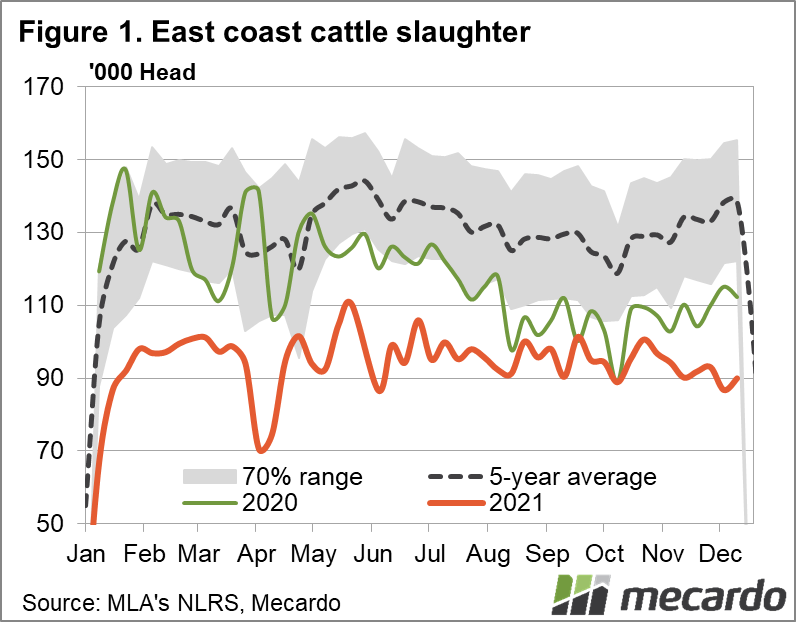

The extra supply seen in yardings, was not replicated in cattle numbers sent for slaughter however, with slaughter numbers still well below the 5-year average. There was a slight lift on the week prior, by 4%, with 89,972 cattle sent for slaughter on the east coast. Despite the lift, this is 20% below the same time last year and last year’s slaughter numbers were already well down on averages as you can see in figure 1.

The 90cl price in AUD terms stayed put, sitting at 898¢/kg swt, as the AUD shifted marginally up (0.1%) to 0.718US. The US are continuing to have trouble securing beef imports, as reported by the Steiner Consulting Group this week, import beef trade remains difficult given ongoing supply chain challenges and uncertainty about supply availability in Q1. There’s also talk of significant price inflation across many protein categories in 2022, but consequently uncertainties about the consumer response should inflation surge.

The year ahead….

Excellent back-to-back seasonal conditions for most of the country combined with strong export demand has created a new floor in cattle prices and it’s unlikely we’ll see things change much with the good seasonal outlook expected to continue into 2022.

The big uncertainties will be around food inflation and how retail trade and consumers will react to continued upward price pressure, especially with inflation expected to outpace wage growth in the first half of 2022, according to the Reserve Bank of Australia.

Having said that most of our beef is exported overseas so what happens in our key export markets influence how the year unfolds.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: MLA, NLRS, Mecardo, BOM