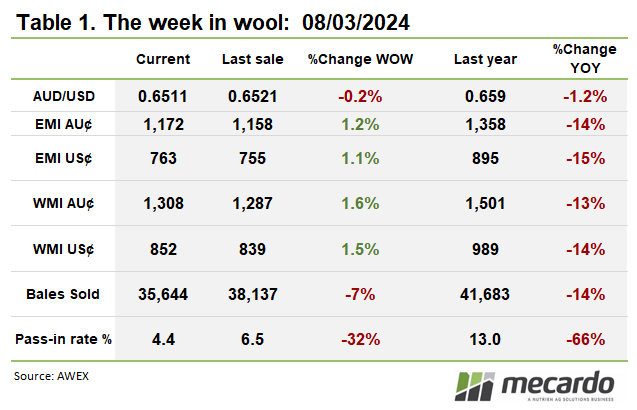

A cautious opening eventually became a solid upward trend in the wool market this week. AWEX reported the strong close in the West on the first day provided the momentum for a solid final day in the East, culminating in a stronger market across the board.

The Eastern Market Indicator (EMI) was 14ȼ better, or plus

1.21% to sit at 1172 ȼ/kg. The lift in

the EMI looked like a surge when compared to the previous 2-week period where

incremental daily increases saw a total of just 17ȼ lift. The EMI expressed in US dollars also

improved, gaining 8ȼ to 763 USȼ.

It was the Merino section that led the market, with gains of

22ȼ to 34ȼ reported, most notably were the 17.0 to 20.0 MPG categories, where

in Melbourne the increases were generally positive by around 2.0%.

Crossbreds were at best “solid”, with minimal price movements,

while the Cardings Indicators improved 7ȼ & 9ȼ in Sydney & Melbourne,

with a 1ȼ gain in Fremantle.

The Pass-in rate fell to 4.4%, the lowest % AWEX has reported

since June 2021, and with a smaller offering just 35,644 bales were cleared.

This week on Mecardo, Andrew Woods provides an update (read

here) on strength premiums and discounts. These are subject to the supply

of low tensile strength wool, and the supply of point of break in the middle of

the staple. Consequently, there will be seasons when the price effect of staple

strength is quite high, compared to the current season where the effect is

minimal. The five- and ten-year medians allow us to look through these seasonal

effects to see what the longer-term impact on price is.

The week ahead….

Next week Melbourne sells on Wednesday & Thursday, while Sydney and Fremantle sales are listed for Tuesday & Wednesday. An increased offering is rostered, with 42,394 bales listed nationally, 22,824 of these bales are in Melbourne sales.

Have any questions or comments?

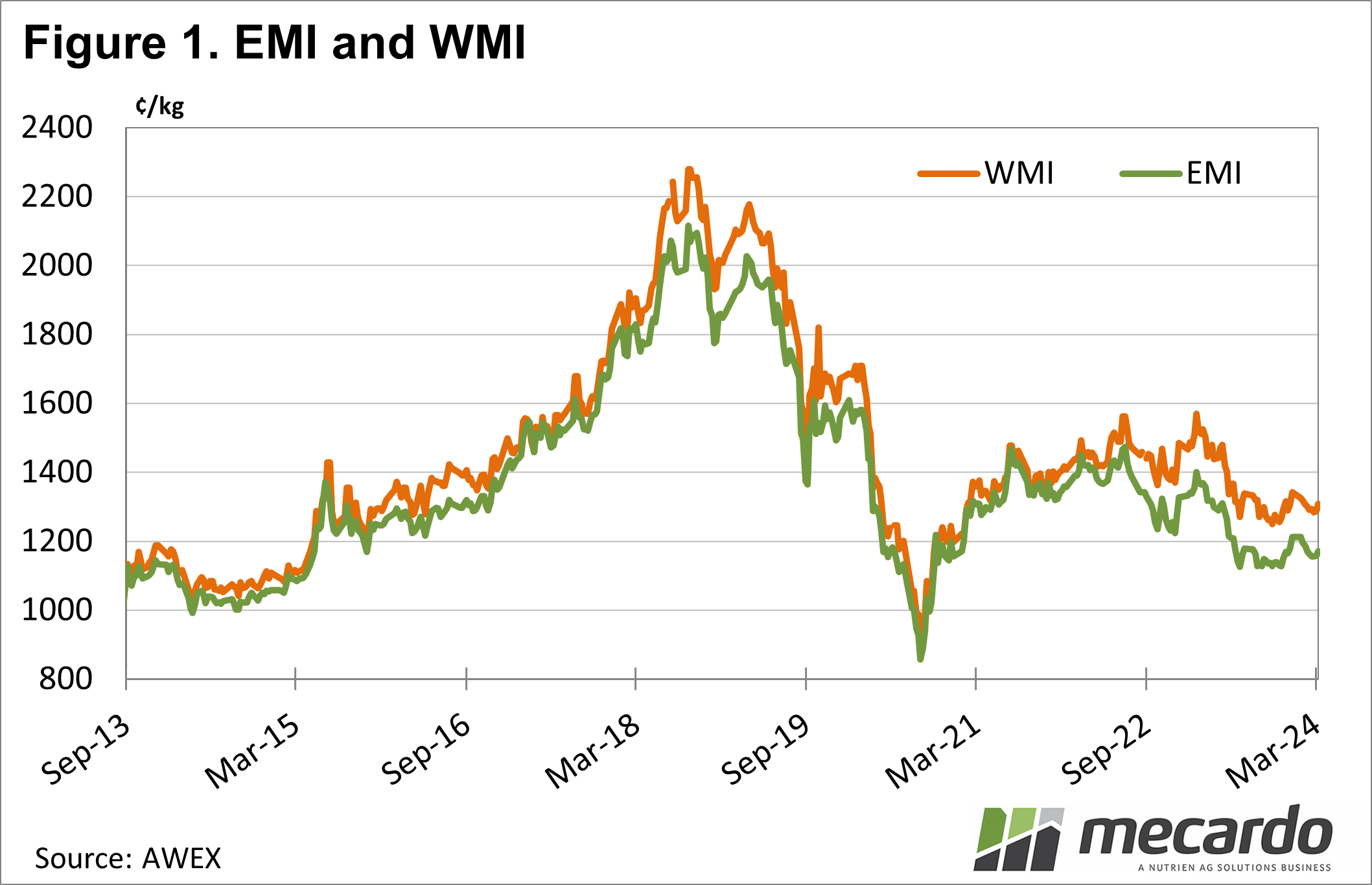

Click on graph to expand

Click on graph to expand

Data sources: AWEX, Mecardo