As the world continues to exit from the pandemic, beer sales are expected to rebound, and in turn, demand for malting barley is expected to increase also. However, drought conditions in Canada and the USA have savagely slashed yields, and reduced quality, so an opportunity to cover the shortfall may open up for Australia.

A dry start, and ongoing drought in Canada and the USA have resulted in large decreases in barley production, and may impact upon malting barley supplies, through reductions in the quantity & quality of the 2021/22 crop.

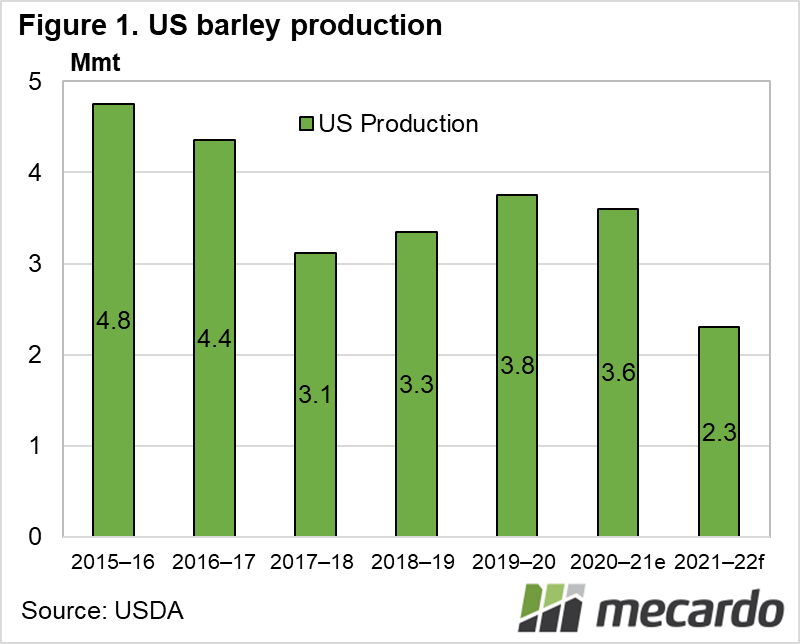

The USDA estimates that US total barley production will be slashed by 1.3mmt(36%) to 2.3mmt. According to the Montana Department of Commerce, over 57% (2mmt) of US barley production is used for malt, suggesting that the US may experience a malt barley shortfall in excess of 1mmt this year.

Yueshu Li, director of the Canadian Malting Barley Technical centre (CMBTC) stated that drought has elevated protein levels above malting barley specifications, and slashed yields, tightening supply, and creating huge production challenges for malting companies.

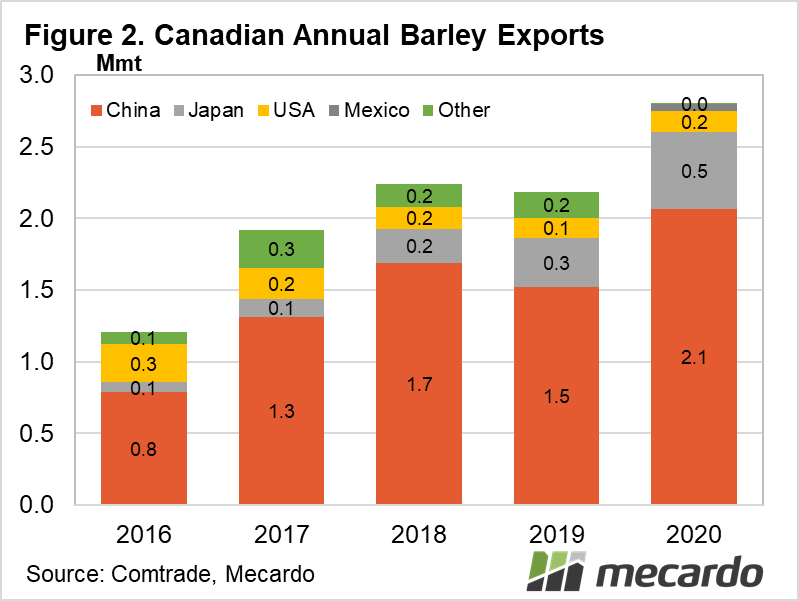

Canada’s barley crop this year was also a disaster due to the drought, with production dropping 2mmt(20%), to a forecast 8mmt for the year. Canada exported 2.8mmt of barley in 2020. Key customers were China (2mmt), Japan (530kt) and the USA (150kt). The International grains Council (IGC) is forecasting a 1mmt fall in Canadian exports to only 1.8mmt in 2021/22.

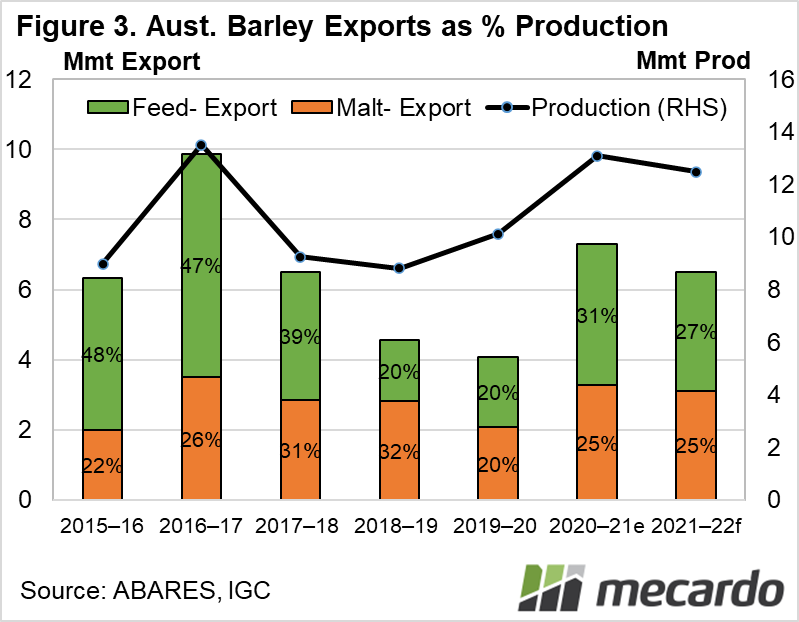

The latest September 2021 ABARES forecast for the total Australian barley crop currently sits at 12.5mmt for 2021/22, slightly less than 2020’s total. (figure 3)

AGEIC and the GRDC indicate that, typically, around 30-40% of Australian Barley production meets malting grade specifications each season, with around 75% of that exported. According to barley Australia, our domestic brewing industry’s consumption is minimal, at only 230kt grain equivalent.

If we assume that 25% of the forecast 12.5mmt barley crop for 2021/22 will be exported as malting grade, that equates to 3.1mmt, with the remaining 3.4mmt of the IGC export forecast expected to be feed grade. (figure 3)

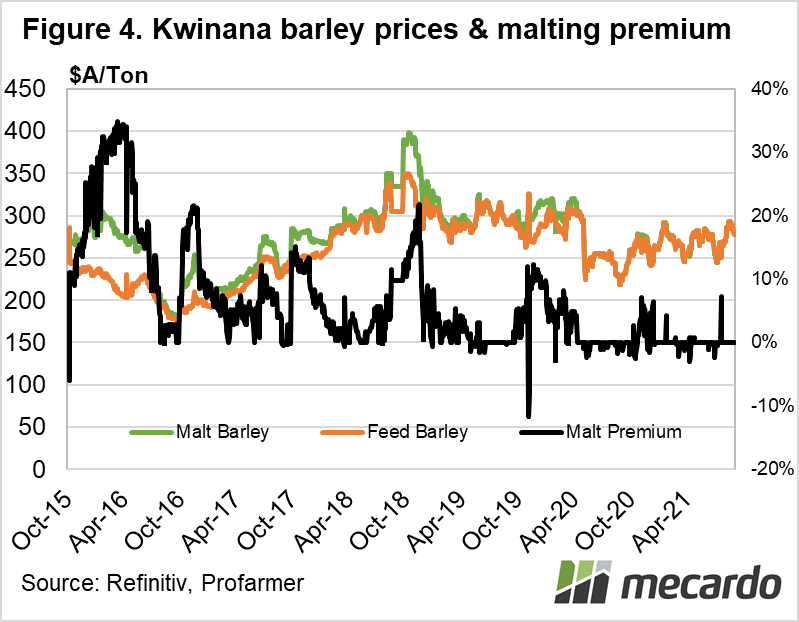

On average, malting grade barley ex Kwinana had fetched a 10% premium to feed grade barely in Australia from 2016-2018, but since 2019, premiums have been largely negligible, with occasional spikes to the 5-7% range. (figure 4)

What does it mean?

With significantly less malting quality barley likely to be produced in the US and Canada, there may be an opportunity for Australian barley and malt to fill domestic shortages in the USA, and replace Canadian exports that are normally destined for Japan. Malting premiums should be monitored closely. Reduced Canadian exports to China will also be supportive of global barley prices this season.

Have any questions or comments?

Key Points

- The US usually produces over 2 mmt of malting barley per annum.

- Drought in the US and Canada has reduced production by 1.3mmt and 2mmt respectively, with the proportion of barley making malt grade expected to take a steep fall.

- Australian producers could capitalize on a potential 2mmt shortfall in the US.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: USDA, CMC, AGEIC, GRDC, COMTRADE