The Meat & Livestock Australia (MLA) September Sheep Industry Projections update was released last week. There were some minor tweaks, but the broader story remains the same. This year is going to be the low for flock and slaughter, but the supply fundamentals remain good for pricing.

Winter lamb and sheep slaughter levels were lower than expected, which has led to the relatively minor adjustments in the flock and slaughter projections.

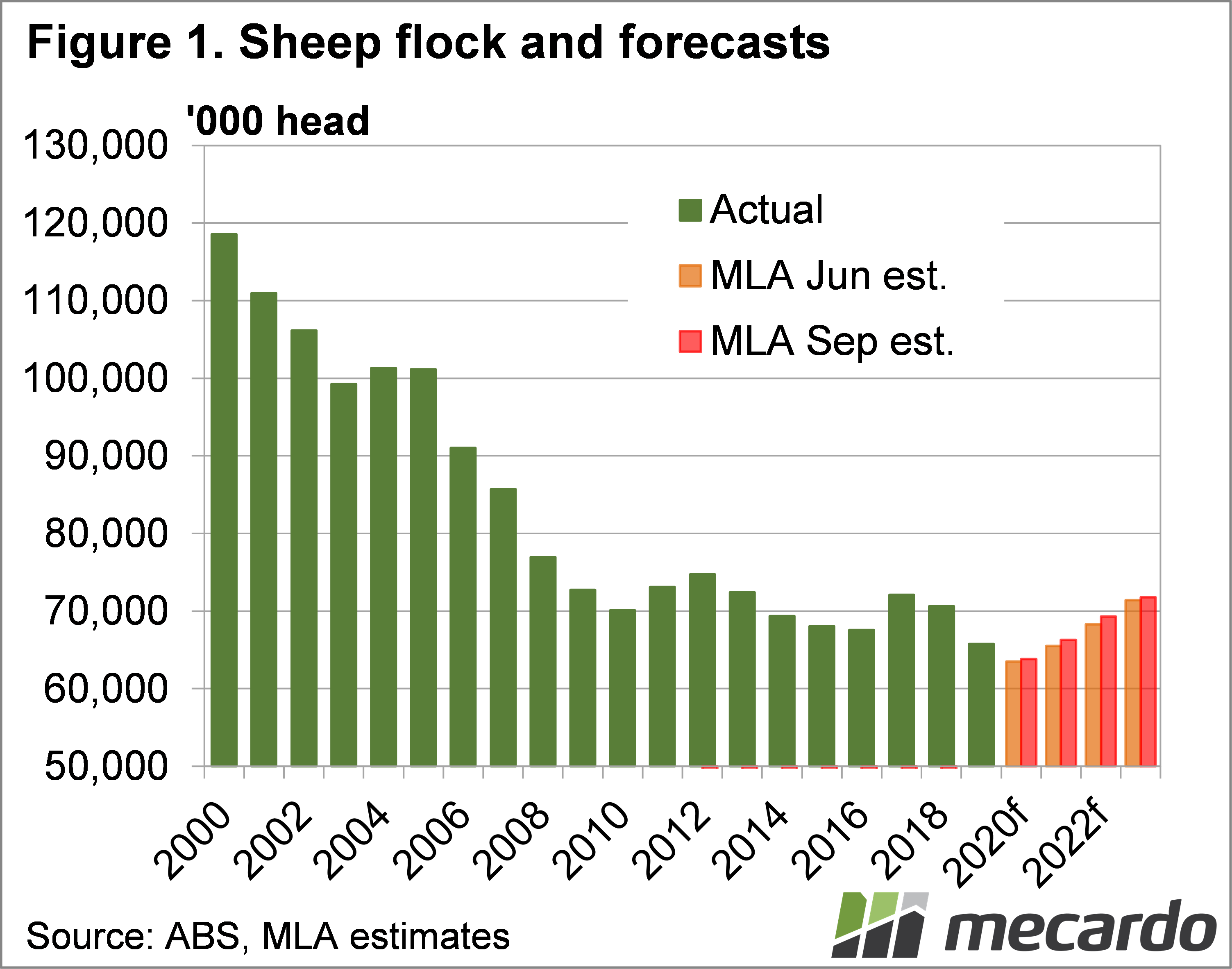

Firstly, the flock. Lower slaughter as a percentage of the flock, for both lambs and sheep, will lead to a flock expansion. MLA adjusted their flock estimate for June 30, 2020, up by 300,000 head, or 0.5%, to 63.8 million head. Figure 1 shows the flock is still expected to be just above a 100 year low, down 3% on 2019. Since 2017 the flock is down 8.3 million head, or 11.5%, which is a lot of wool and potential lamb production to lose.

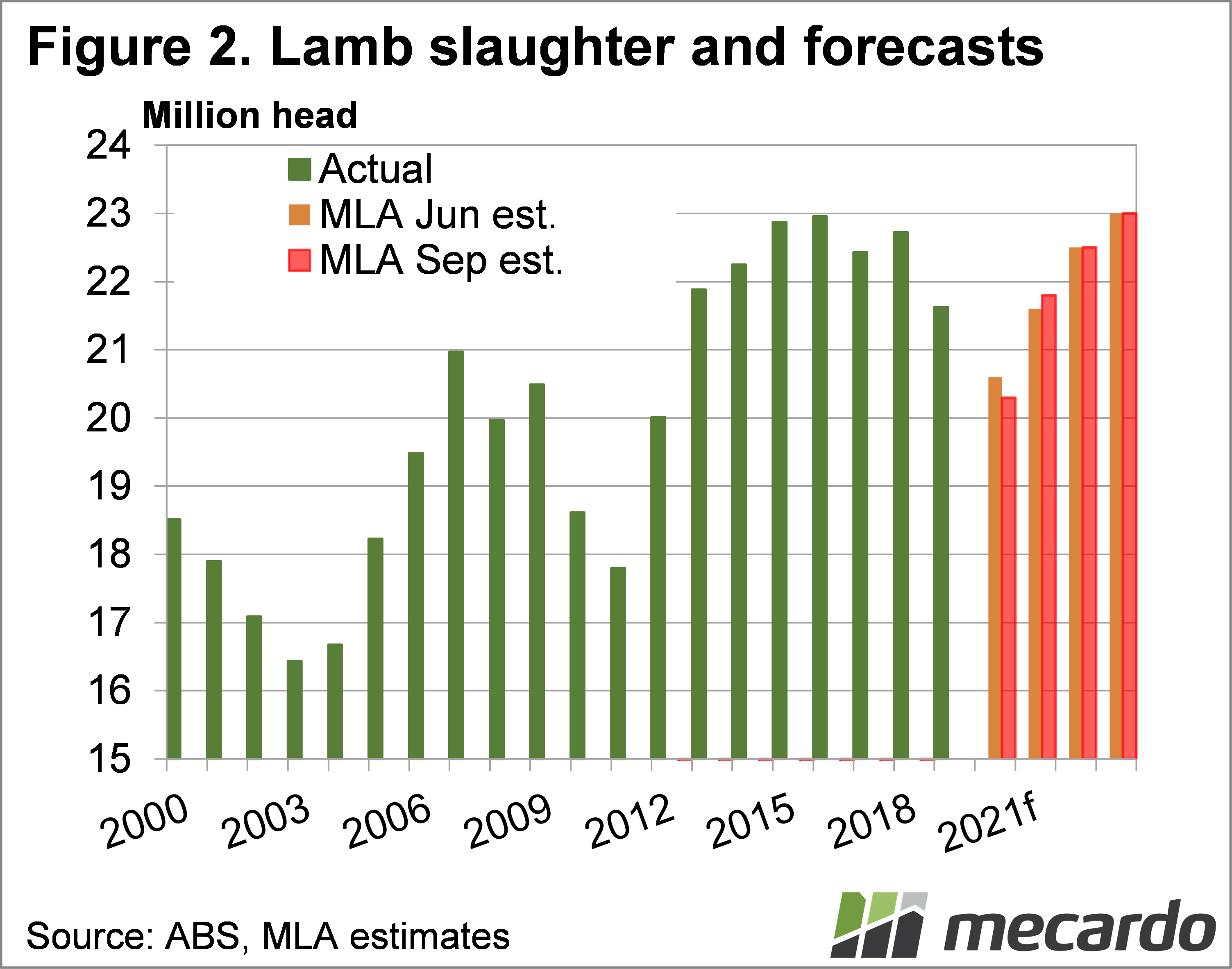

Weaker lamb slaughter rates saw MLA pull 2020 slaughter estimates back by 300,000 head, or 1.5% to 20.3 million head. We are nearing the end of an 8 year low in lamb supply, which is expected to finish 6.1% below 2019 and 11.6% below the peak of 2016. Figure 2 shows lamb supply is still expected to grow, 2021 taking a 7.5% jump higher. Further growth is expected to see record slaughter in just 3 years’ time.

Next year lamb slaughter is forecast to return to the levels of 2019, which will be by no means disastrous for prices. Demand is likely to be lower, but prices were still very good last year.

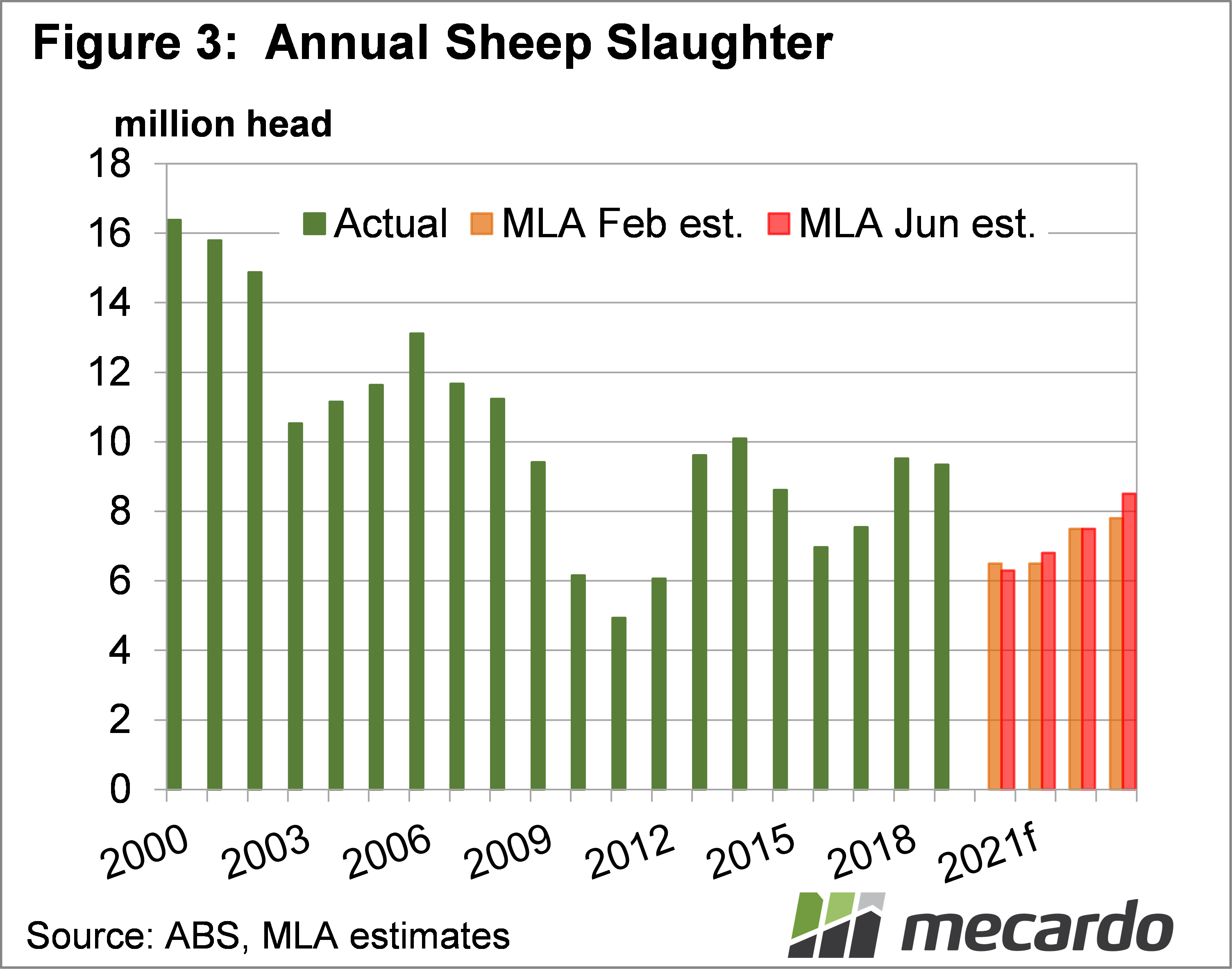

While lamb slaughter is expected to recover relatively quickly, the flock rebuild will keep sheep slaughter at low levels for at least the coming year. Figure 3 shows MLA revised down sheep slaughter for 2020 down by 3%, but these are then forecast to come forward in 2021. In 2021 sheep slaughter is expected to rise by 8%.

The biggest revision across the projections was sheep slaughter for 2023. MLA added 9% for 2023 sheep slaughter, which will take it to 8.5 million head, not as high as 2018 and 2019, but much higher than this year.

What does it mean?

It is somewhat fortunate that the Covid-19 demand issues have coincided with 8-year lows in lamb and sheep supply. This has supported prices, but rising supplies will test demand over the coming years, especially for lambs.

How wool and lamb prices track over the coming six months will impact lamb supplies in the coming years, with a possible increase in the use of terminal and maternal sires lifting lamb numbers.

Have any questions or comments?

Key Points

- MLA’s Sheep projections made some adjustments due to weaker slaughter over winter.

- This year we expect to see the flock find its low, along with lamb and sheep slaughter.

- Lamb slaughter is forecast to recover relatively quickly, which could pressure prices from 2022.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: MLA, Mecardo