Australian lamb and sheep prices are currently holding at very strong levels, but how do they compare to livestock prices in the USA, one of our most important export markets, which typically receives over 25% of our export volumes?

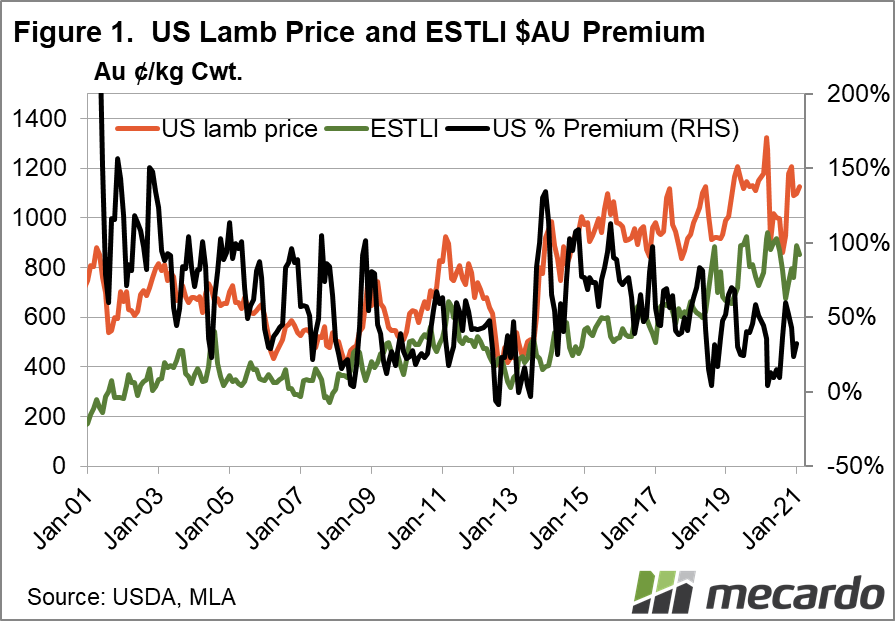

US lamb prices have been substantially higher than Australia for over a decade, with few exceptions. Since 2010, US lamb prices have operated at a level around $2.30 USD/kg, or $2.80 AUD above the Eastern States Trade Lamb Indicator (ESTLI). This equates to a huge 50% premium.

The USDA’s US Sioux Falls, Dakota live sheep price benchmark for 19kg-29kg cwt lambs for February 2021, sat at $11.25/Kg cwt AUD; a solid $2.75 AUD, or 32% above the ESTLI at $8.50/Kg cwt. A 32% premium above US prices sounds very healthy from an Australian perspective, however, in historical terms, this is near all-time record lows.

Since 2014, the price premium of US lambs over their Australian counterparts has steadily declined, from a peak of 135% in December 2013. The average US premium to the ESTLI for 2020 was only 31%, compared to 47% in 2019 – a stark contrast to 2017, where the premium averaged over 55%.

The root cause of this steady erosion of the relative international price differential is that since the start of 2014, Australian lamb prices have risen faster than US prices, bridging the gap. In short, Australian lamb has become more expensive, faster.

Over this period to 2021, in AUD terms, the US lamb price has only risen 18% (AUD), while Australian prices have jumped 110%. In USD terms, the story is the same, with US prices rising 14% while the ESTLI has risen 80%.

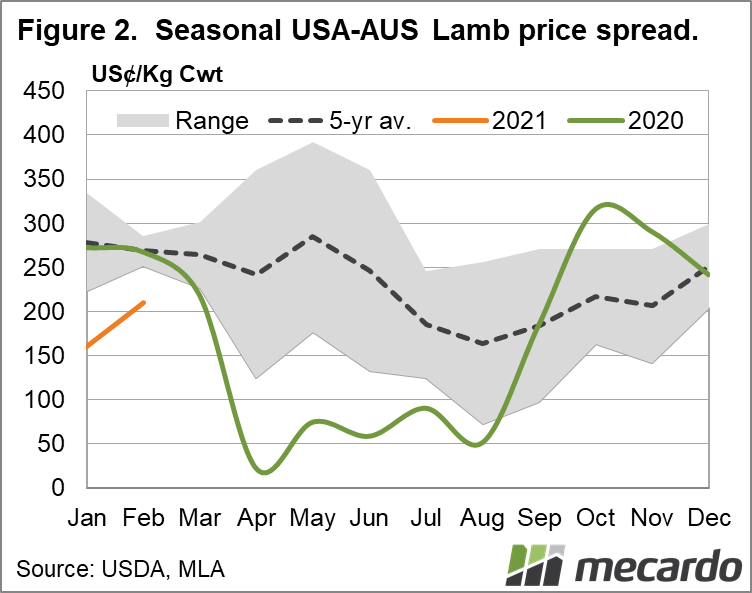

The monthly price spread differential in USD terms has been quite volatile over the past five years, ranging from only $0.22US up to $3.80US (figure 2). The current level of $2.10US is, however, not far from the five-year average of $2.30US.

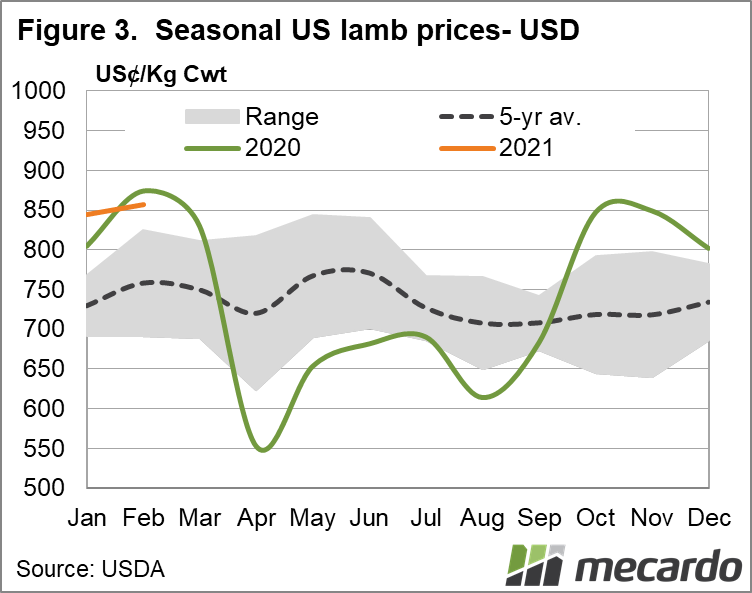

In terms of seasonality, US lamb prices tend to rise from April to July each year (figure 3), and then decline to stagnation post August, however, that typical pattern was not reflected in 2020. The influence of COVID-19 caused prices to fall sharply in April-20, before recovering strongly in September-20. The closure due to bankruptcy in July-20 of the Colorado-based Mountain States Rosen processor, which had a capacity of 800,000 head p.a, equating to around 36% of total US slaughter had a profound impact upon US domestic lamb prices. The strategic purchase of the facility by JBS and planned conversion to beef processing is expected to boost overall US lamb import volumes.

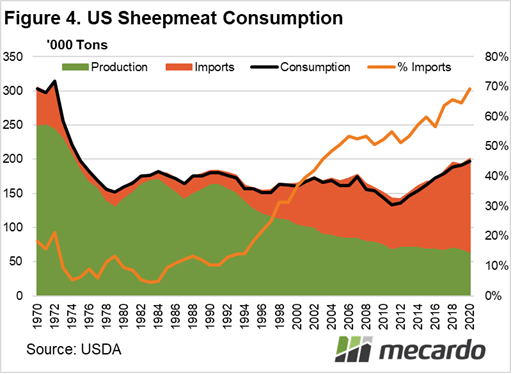

Overall, the US sheep industry is in long term structural decline. Even though US lamb consumption is expanding, domestic production and the overall flock size is falling, while imports are rising to fill the gap (Figure 4). US sheepmeat imports as a percentage of consumption have risen from 52% in 2010 to 69% in 2020. Australia is well placed to fill the void, as the trend toward imported product continues.

What does it mean?

Despite the cost of Australian lamb, the combination of a long term structural decline of the US sheep industry plus increasing demand for sheepmeat in the US points towards continued strong export fundamentals for trade of lamb from Australia to the USA.

Have any questions or comments?

Key Points

- US lamb price premium of 30-50% over ESTLI

- Relative US lamb premium is declining

- Steep rise in Australian lamb prices narrowing the price gap.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: USDA, Steiner, Mecardo, MLA