Markets have had a rough week. Concerns about financial instability around the globe became increasingly front of mind with the forced merger of Credit Suisse and UBS, and the collapse of two US banks. Add to that, the renewal of the Black Sea Grain Initiative and a big harvest in Brazil has added to price weakness in commodity markets.

Once again the Black Sea Grain Initiative has been given the go-ahead, allowing for the continued safe export of Ukrainian grain for at least the next 60 days. This is only half of the previous extension length mind you, and Russia has stated that further extensions would depend on the removal of all sanctions related to agricultural enterprises. It is important to note that there are no sanctions directly applied to Russian ag exports but there are barriers regarding finance, insurance, and agricultural imports (ie farm machinery and spare parts).

The 60-day timeline makes for an interesting juncture. It means that the end of the agreement will fall right at the start of the Ukrainian winter harvest. The world’s buyers will be marking this on their calendars as it often presents an opportunity to purchase cheaper grain and to source grain from closer origins as the northern hemisphere harvest gets underway.

We mentioned last week that the huge Brazilian crop is starting to weigh on the market. Dry conditions in central and eastern Brazil should allow these regions to catch up with delayed soybean harvests and safrinha corn planting. Furthermore, good weather conditions for safrinha corn planting and production are expected in Mato Grosso through the end of march. Argentina is experiencing its worst soybean crop in nearly 25 years due to severe drought and other localized extreme weather events. Large volumes of rain are on the near-term forecast in some regions which might stabilise some crops but also creates a risk of local flooding.

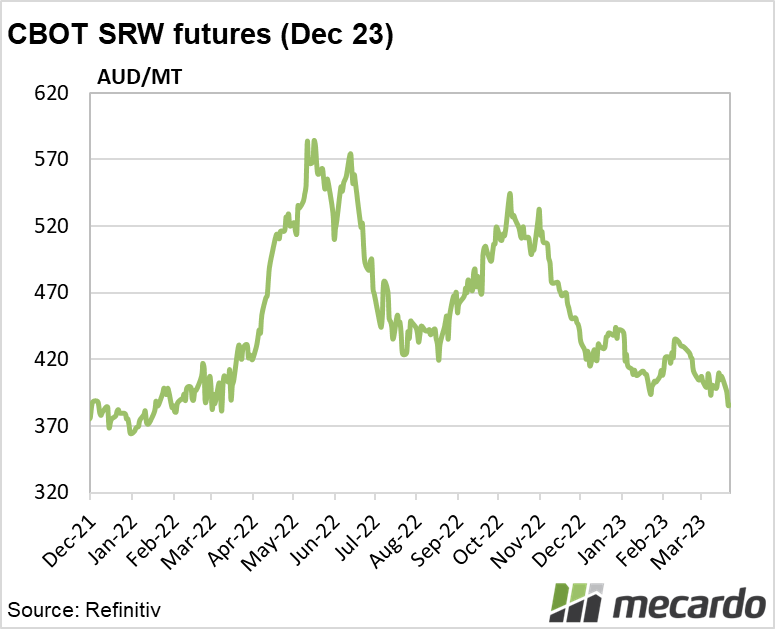

The bearish news sent the December 2023 CBOT wheat futures contract sliding over the week, in AUD terms ending Thursday at $386/MT, 5% lower than the close of last week. Locally cash APW prices were also sent lower. Geelong APW ended Thursday at $379/MT, down $14 on the close of last week.

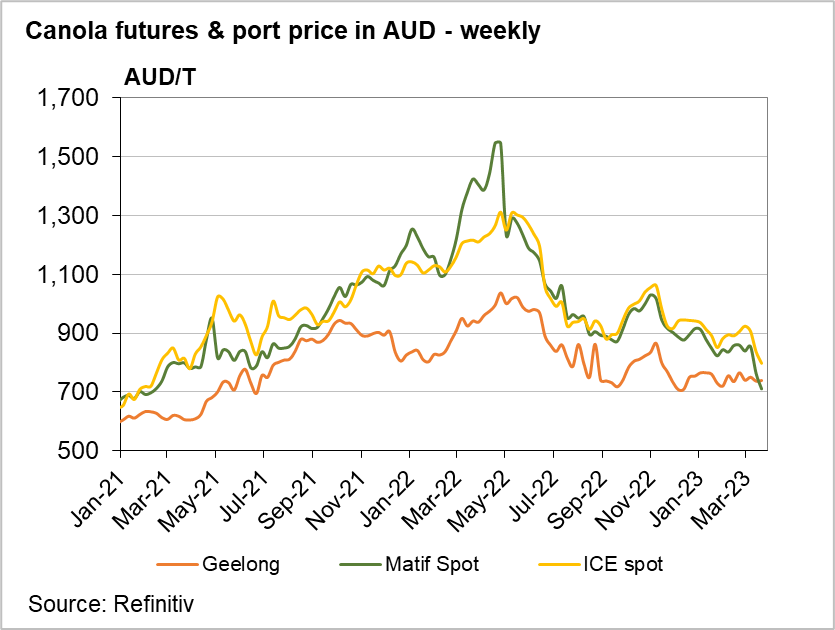

The downfall in canola prices has continued and doesn’t look as if it’s about to slow up. Geelong canola cash prices ended yesterday at $592. While Australian canola has been priced competitively globally, it is the nearby demand that has fallen off a cliff. Reduced crush demand in Europe has led to a surplus of supply. Demand simply will not pick up until that surplus has been eroded. A positive for the medium-term outlook is that global vegetable oil inventories are expected to decline into the second half of the year.

The week ahead….

The BOM 8-day rainfall is showing a 25% chance or 15-50mm for parts of WA, NSW, and Vic which may have added to the weakness in price this week. If you are looking for bullish news though, we could point to a return of El Niño impacting Australian production. A later seeding rain in Australia could see the intended area shrink if the opening pushes out beyond May.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Data sources: Reuters, Next Level Grain Marketing, Nutrien, Mecardo