Since the China ban on Brazilian beef was removed in December, trade flows of Brazilian beef have resumed with gusto, and penetration into the US has run at record pace. What could this mean for Australian 90CL exports?

Brazil produces copious amounts of lean grass-fed beef, however, market access is a constant problem.

On 21st February 2020, fresh Brazilian beef was re-approved to enter the US market on account of a favorable USDA report which ascertained that it’s meat inspection systems were on par to that of the US. Prior to this point, only heat-treated Brazilian beef products could enter the US.

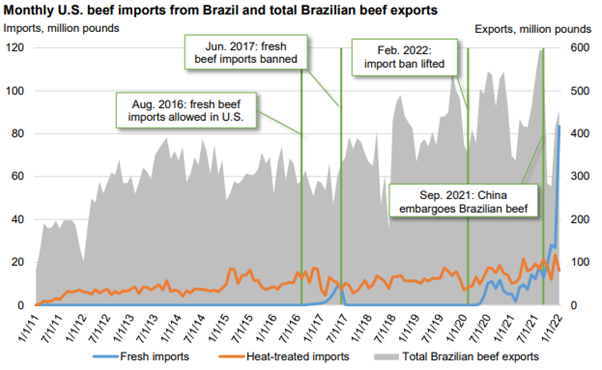

In September 2021, China banned imports of Brazilian beef in response to detection of atypical mad cow disease in geriatric cows in several states. The ban was initially tipped to only last a couple weeks but dragged on for three months, with access only restored in December 2021. The Chinese export embargo cut off the traditional export market route for over 60% of Brazil’s beef exports, and triggered a huge surge of product being diverted into the US. (figure 1) These imports are primarily composed of frozen boneless trim, which is bound for the hamburger manufacturing sector, similar to Australia’s main offering to the US in the form of 90CL.

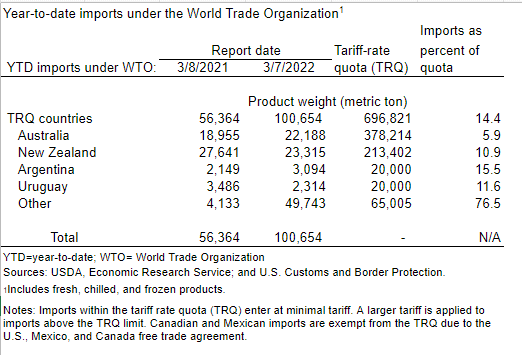

However, Brazil does not enjoy a free trade agreement with the US, and therefore accesses America via the 65,000 tonne TRQ quota, which is shared with other nations. When the quota is exceeded, a 26.4% Most Favoured Nation (MFN) tariff is applicable.

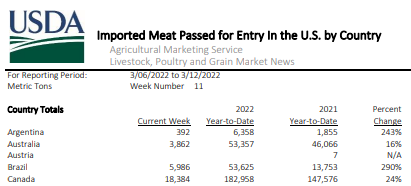

As of the 8th of March, the USDA reports that ~50Kt of the TRQ quota was filled, (figure 2) and given that average imports into the US have been around 6Kt / week, ~85% of which is fresh beef, (figure 3) the 65Kt tariff free quota will most likely be fully exhausted by the end of March. This is several weeks ahead of where some commentators like Steiner were originally tipping. Year-to-date Brazilian imports of beef into the US are up 290% on 2021 levels. (figure 3)

Worryingly though, Steiner reports that sellers of Brazilian beef are offering up product in Q2 at sharply competitive prices, suggesting that they are willing to absorb the additional tariff cost to ensure their product continues to move.

The urgency from Brazilian exporters is thought to be stemming from nervousness about Chinese demand, as a combination of rising COVID-19 cases, and a dogged pursuit of zero COVID has pulled over 51 million Chinese into hard lockdown already, with possibly more to come. With COVID on the march again, and the threat of entire communities and swathes of cities being thrown into isolation, it is likely that Chinese foodservice demand could flatline.

Ominously, Steiner claims that initial reports coming out of China foreshadow that their animal protein imports for the first two months of the year could be down as much as 33% compared to 2021. However, as Angus Brown discussed last week, demand for Australian beef may be relatively solid in comparison to other sources, as our beef export volumes to China were strong.

What does it mean?

Imports of Brazilian beef into the US have helped increase supply, and keep a lid on prices. However, with Brazil expected to exhaust its MFN quota in April, this could cause volumes to reduce, and put upward pressure on US beef prices. Of concern is that Brazil has showed initial signs that it will absorb the tariff cost.

Meanwhile COVID related jitters in beef demand from China, Brazil’s biggest customer, may set the scene for a flood of effectively subsidised hamburger beef entering the US from Q2 onwards, which will not be favourable for Australian 90CL exports. However there does need to be the appetite for US manufacturers to purchase the product, which does not match procurement standards for many large buyers.

Have any questions or comments?

Key Points

- China banned Brazilian beef imports in September 2021 for 3 months.

- Brazilian export to the US has surged since the ban.

- US TRQ quota is almost filled – 26.4% MFN tariffs will apply afterward to Brazil.

Source: USDA , Livestock, Dairy, and Poultry Outlook: March 2022 (usda.gov)

Data sources: USDA, Steiner, Mecardo