The appetite of the US for Australian beef will become evident perhaps sooner rather than later. With exchange rates continuing to play their part in Aussie export affordability and processor cow spec cattle plentiful, if the US wants it, there will be plenty of beef flowing from Australia.

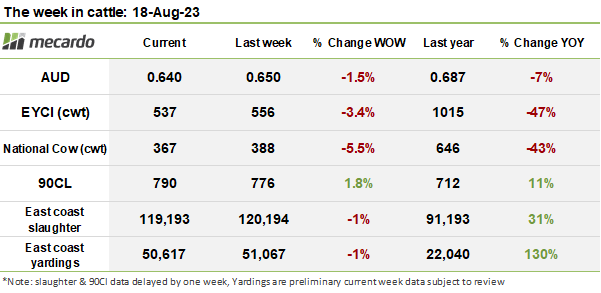

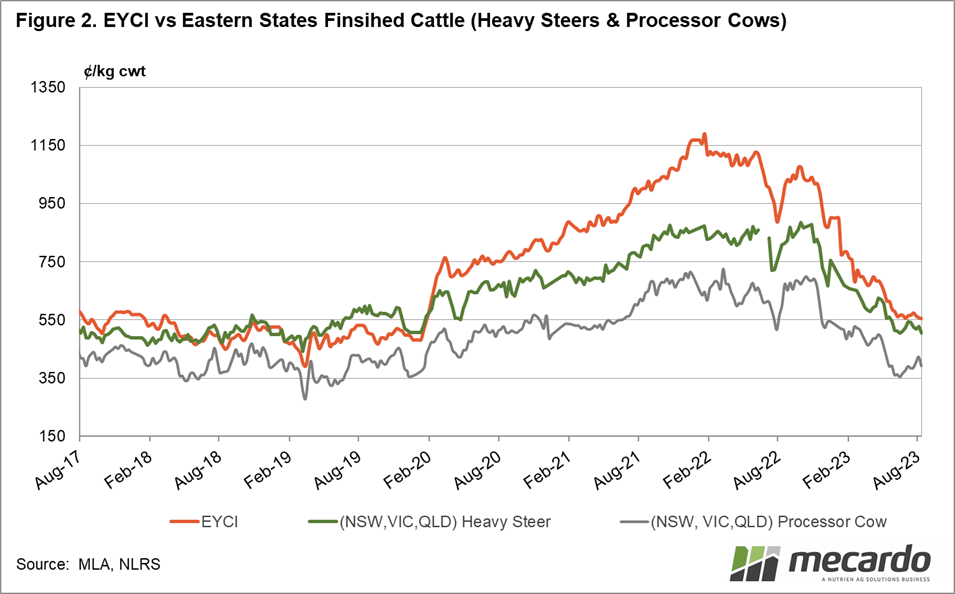

With Young cattle supply not budging this week, the pressure began to tilt prices downward again as the Eastern Young Cattle Indicator (EYCI) dropped 19¢ to 537¢/kg cwt, a fall of 3.4% and now 47% lower than this time last year. Despite fewer numbers through saleyards the Western Young cattle indicator also saw a decline, shedding 7¢ to 517¢/kg cwt.

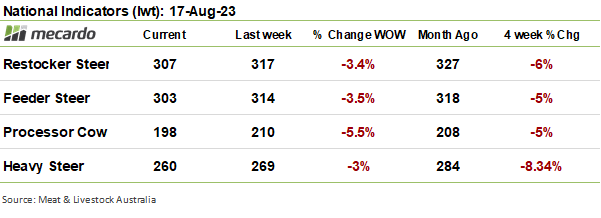

Feeders were down in NSW by 10¢ to 306¢/kg lwt, on the back of a 58% week-on-week increase in saleyard throughput of feeder spec cattle. The majority of the action was in Dubbo where 1565 head went through the yards at an average price of 314 ¢/kg/lwt. Further south to Victoria, the indicators averaged out to 278¢/kg/lwt, a 9¢ decline.

The Queensland feeder steer market was less troubled by the influx of supply, despite a 130% week-on-week jump in yarding numbers. Pricing averaged out to just a 5¢ decline to 311¢/kg lwt. Despite significant numbers (2500 head) of feeders at Dalby, the local average price increased (albeit by 1¢) to an average of 332¢/kg/lwt.

Finished cattle numbers were steady on the previous week (around the 3000 head mark) but the Heavy Steer national indicator softened by 9¢ to finish at 260¢/kg lwt, perhaps an indication that buyers were focused on other markets.

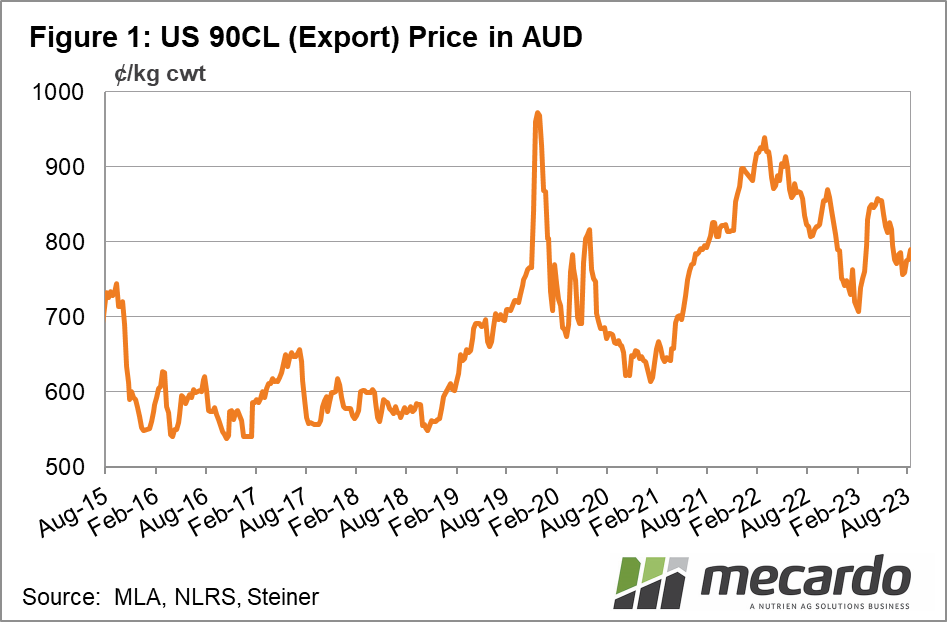

The Aussie dollar has depreciated 7% year on year and the low tide mark for the exchange rate with the US for 2023 was reached earlier this week. This will evidently benefit export pricing as the 90CL beef export price last week increased by 1.8% to 790¢/kg. The timing is excellent for processors as processor cow throughput was over 15000 head for the second consecutive week. Yardings for processor cows in August this year have been significant, with over 42000 head nationally for the month to date. This is already 45% higher than the entirety of August yardings last year.

National Processor cow pricing is down an average of 21¢/kg/cwt or 5.5% this week compared to last. In Victoria, they lost 19¢ for the week to sit at 207¢/kg/lwt. With margin to be made, more attention could swing towards this market in the coming weeks unless demand signals across the Pacific swing the other way.

The week ahead….

Early reports suggest slaughter has increased to over 123 000 head this week as the supply chain looks to manage what could be a significant logistical test this spring.

Q2 ABS slaughter data shows high female cattle turnoff and suggests that destocking is occurring in some areas (more on this next week). This sheds some light on the recent market weakness but as we know there are other demand factors at play. The only thing that will halt further slaughter growth in the coming months would be opportune rainfall.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: MLA, Steiner, ABS, Mecardo