Since the heavy fall back in March, canola prices have been relatively steady. Relative to what we have seen over the last three years (where volatility has been rife) If we compare recent moves to pre-2021 levels, they would be highly volatile.

The market perspective has changed markedly over the last three years. Before 2021, weekly price swings of $20-30 would have been seen as highly volatile. Now it’s not unusual for canola prices to move $40-50 in a week and growers take it in their stride.

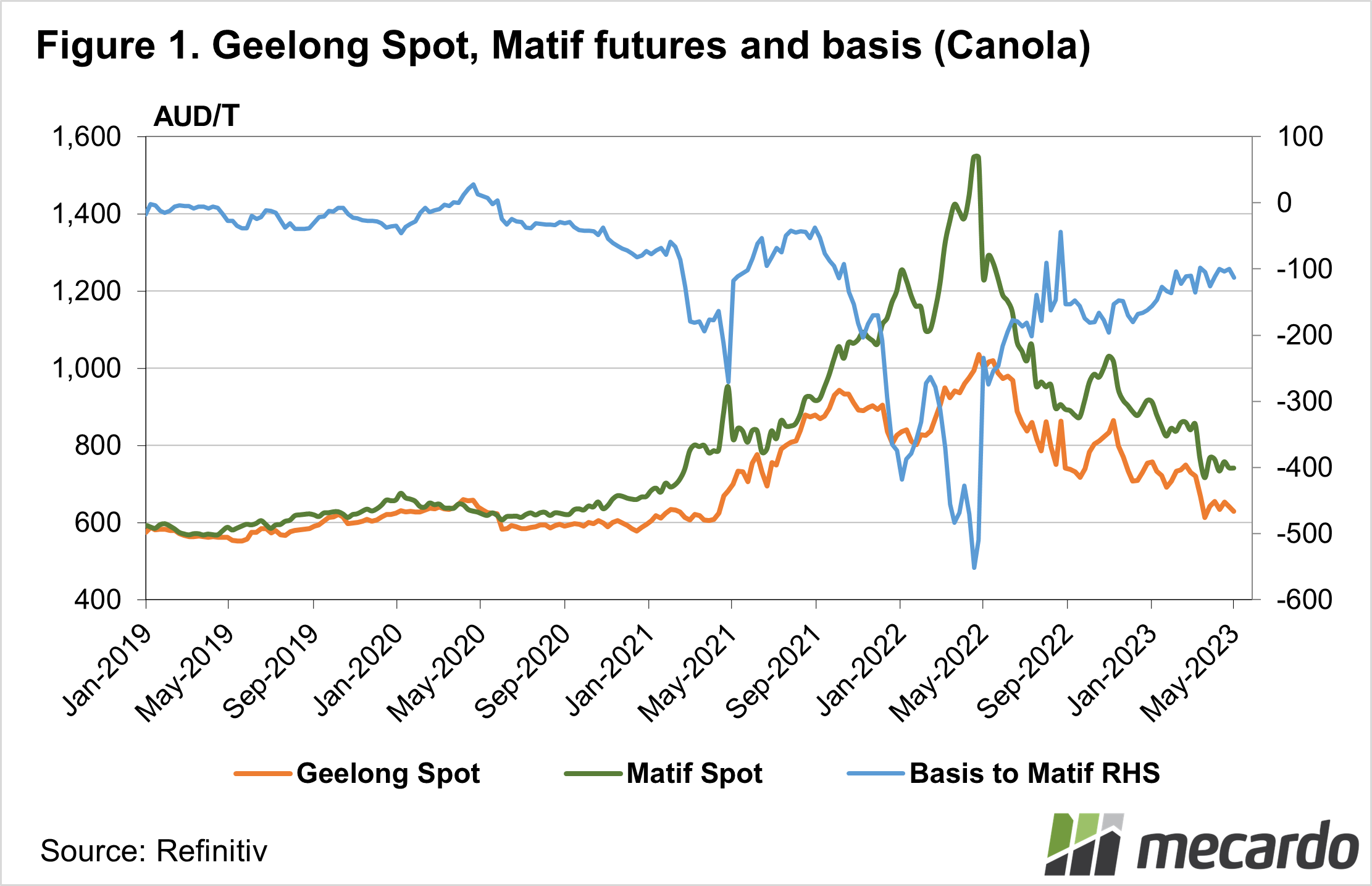

Back in March canola prices lost over $100 in four weeks, but as we can see in Figure 1, prices have steadied since then. Matif (Marché à Terme International de France) rapeseed futures have ranged from $733 to $764 in April, which while historically volatile, is benign these days.

Locally, old crop canola values have continued to follow Matif, with the ‘basis’ or spread remaining in a narrow $100-110/tonne range for much of April.

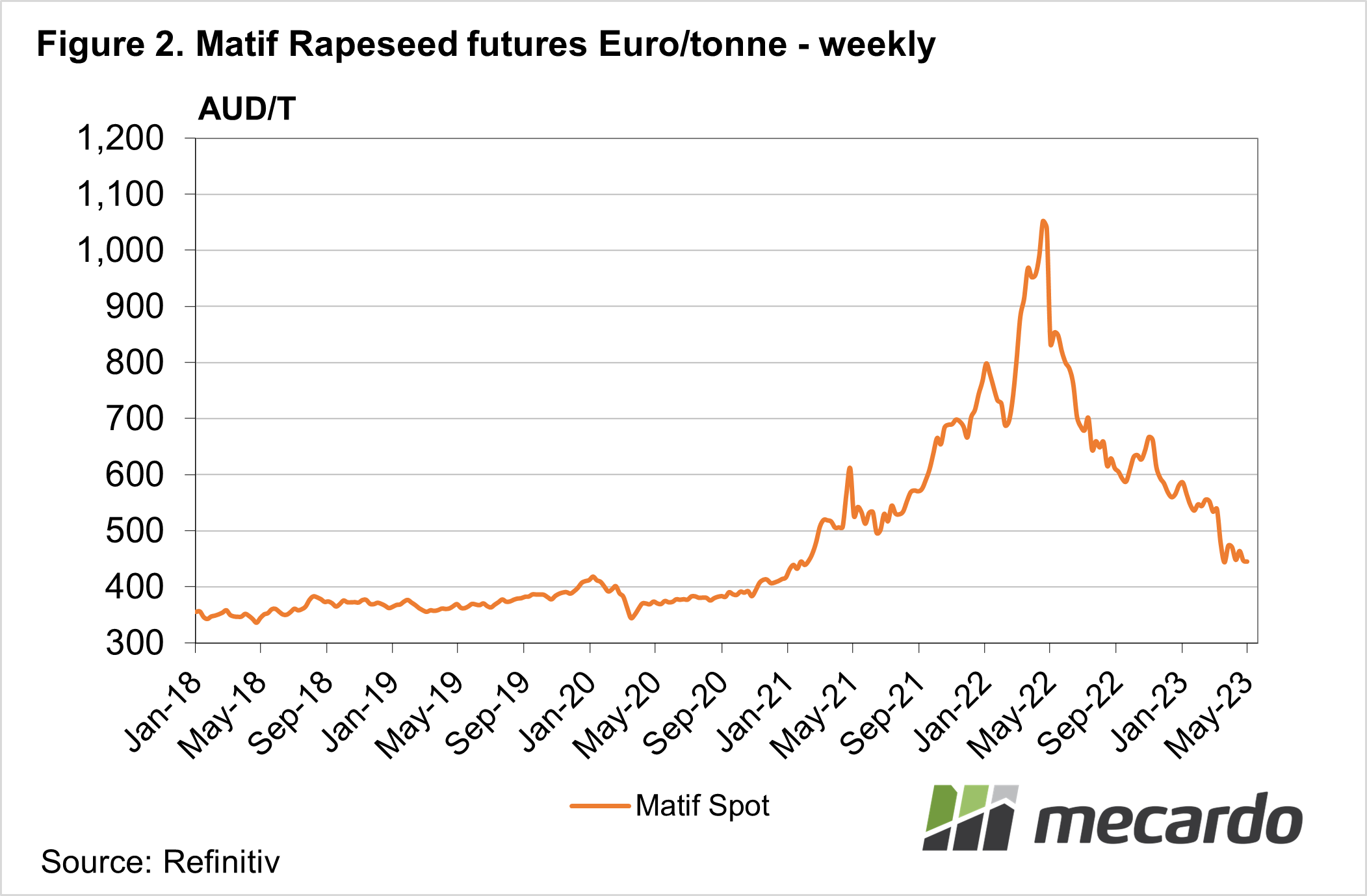

Looking at Matif rapeseed in its native currency, Euro per tonne, there is some concern for further downside. The chart looks symmetrical from the rapid increase in prices in 2021 and 2022 to the fall off the cliff and then the downward trend in the second half of 2022 and into 2023.

The problem is the market is not back at 400 euro/tonne yet, which is where it started in late 2020. It should be remembered that late 2020 prices were still considered strong, with Matif trading in the $300s for much of the five years before 2020.

The argument for a higher floor in international prices is strong. The war in Ukraine continues to add a risk premium to all cropping grains and oilseeds. Energy prices are strong, which is linked to oilseed values, also adding support.

These factors, along with the increased costs of production, which are nowhere near back to pre-2021 levels, suggest we might be nearing the new floor in MATIF canola values, around the 400 Euro/tonne level.

In our terms, we go back to Figure 1 and see we are already sitting around the $600/tonne levels which were prevalent pre-2021. There is some room for upside locally, with the spread to Matif still around $50/t below ‘normal’ season levels.

What does it mean?

There is always downside, especially if a big US soybean, Canadian canola, and European rapeseed crop is produced. The new season World Agricultural Supply and Demand Estimates (WASDE), which will be released this week, might shed a bit more light on this. However, from a charting and profitability perspective, it looks like canola is nearing cyclical lows.

Have any questions or comments?

Key Points

- Canola prices have been relatively steady since the heavy falls back in March.

- Looking at charts, Matif Rapeseed might have a little further to fall.

- There is some upside possible in the local spread, which should support local prices.

Click on figure to expand

Click on figure to expand

Data sources: CME, Refinitiv, Mecardo