Grain markets have been on a steady decline since posting peaks two months ago. Canola is no exception, with new crop prices sliding. Canola has slipped under the $600/t mark, but that doesn’t mean that it isn’t still good selling.

Traditionally the wheat hedging window is well and truly shut by now, with Northern Hemisphere harvest ramping up and sending values lower. The oilseed hedging window supposedly stays open longer, with soybeans, rapeseed and canola not harvested in the northern hemisphere until late summer or autumn.

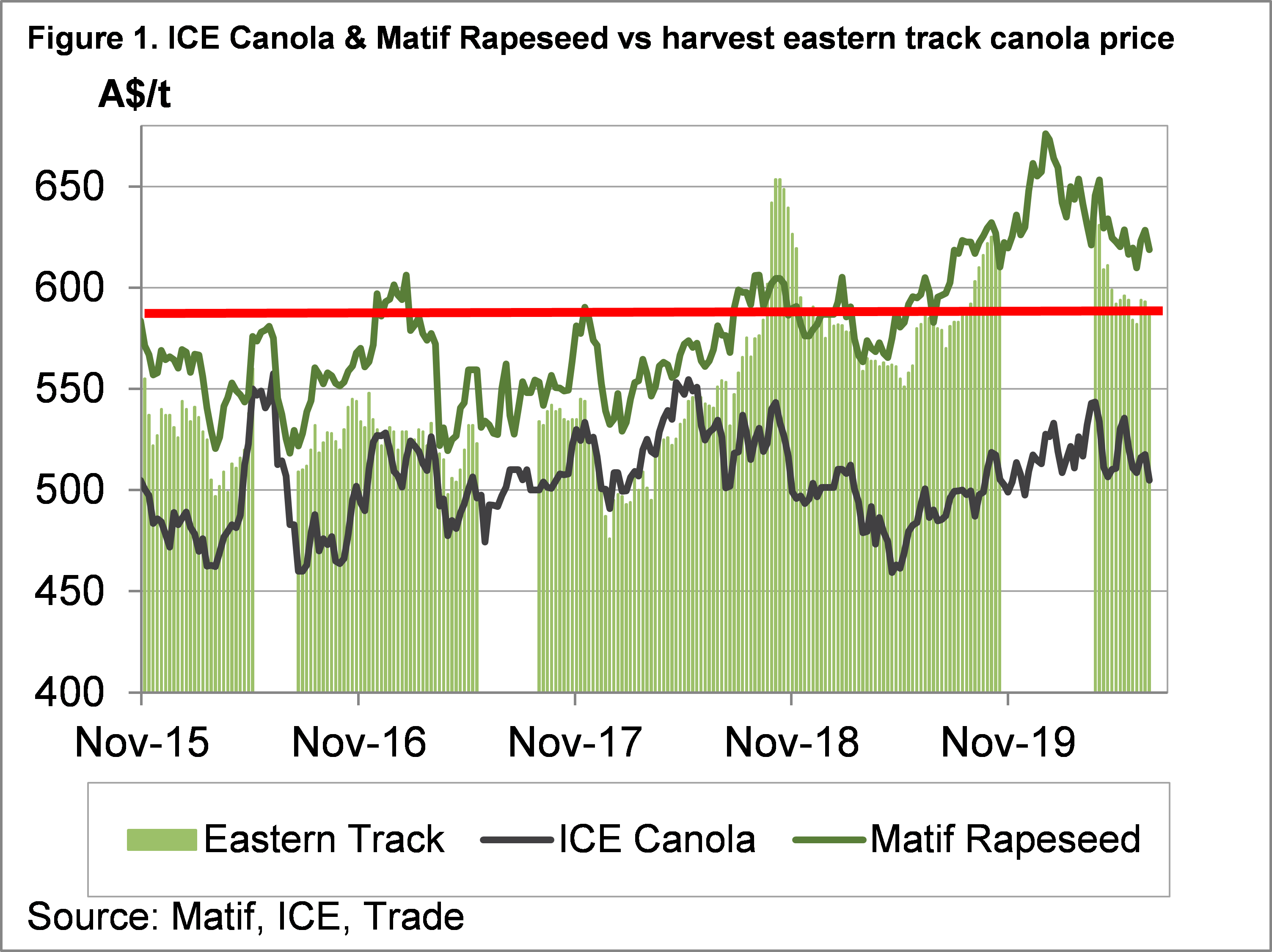

ICE Canola and Matif Rapeseed Futures are the major international contracts we are interested in here. However, figure 1 shows that since mid-2018 Australian track prices have somewhat decoupled from their Canadian counterpart, the ICE contract. Australian canola growers do still have a hedging option, with track prices now following Matif Rapeseed more closely.

The switch in leading prices has much to do with the smaller yields of the last two harvests. The EU is now a major export market for non-GM canola, and as such our prices have been following theirs closely.

Figure 1 shows that since early April, Matif Rapeseed has been on a steady decline, in our terms falling from $650/t to $618/t. Local track canola prices have fallen in a similar fashion, with most of the damage done in April. Coming from $630/t, canola now sits between $580 and $590/t at east coast ports.

Despite receiving well over $600/t last harvest, canola this year can still not be described as cheap. Figure 1 shows there have been few times over the last five years when prices have been better.

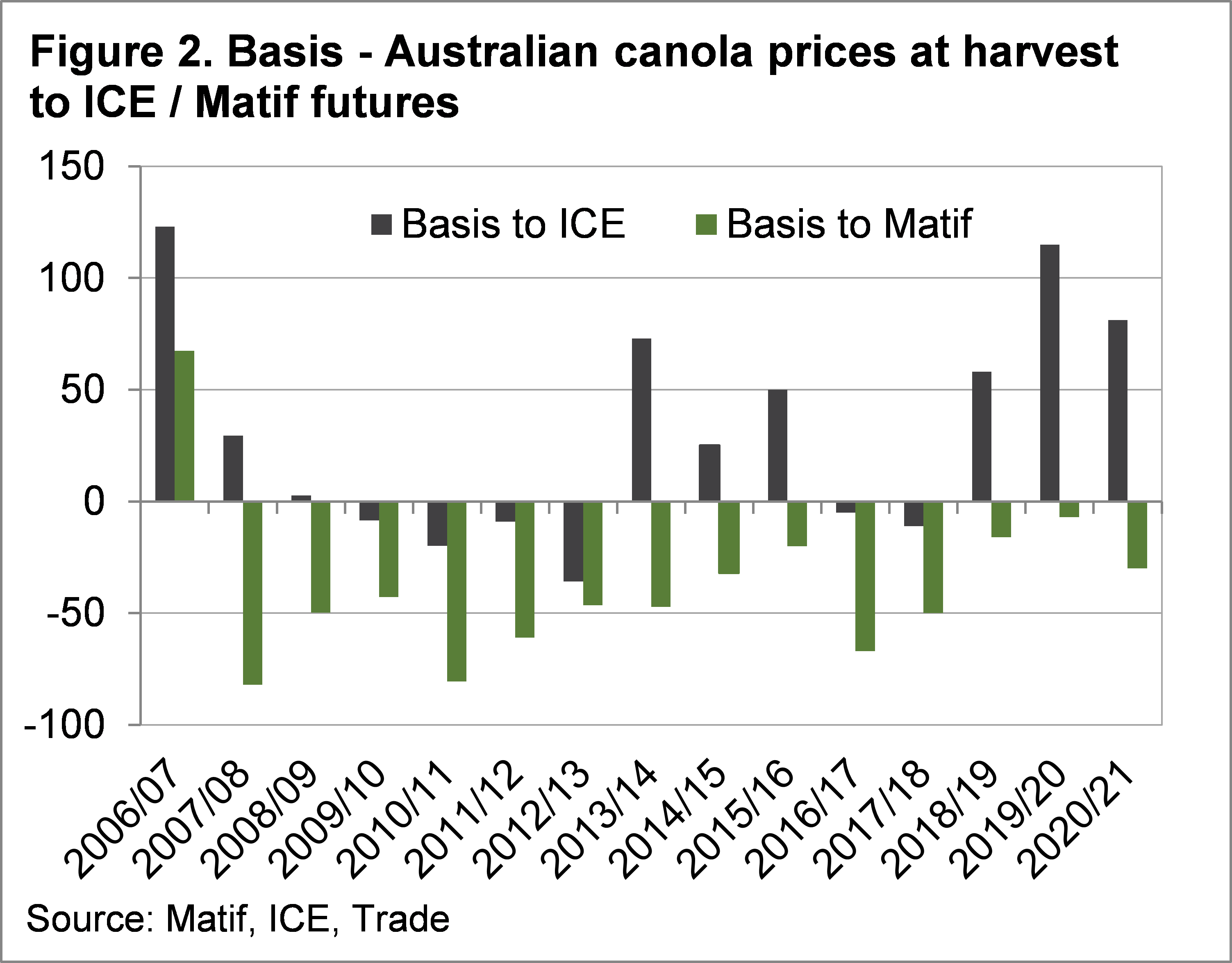

The other measure of value we like to use is basis, or the spread between local prices and futures. Figure 2 shows how harvest basis to ICE and Matif has performed over the last 15 years. Generally, Australian basis to Matif tends to move with production.

The large harvests of 2016/17 and 2017/18 saw basis at negative $50. The last two years have seen local basis only slightly negative. With the canola harvest forecast to rise this year, new crop basis is sitting at negative $30.

What does it mean?

With new crop canola basis currently stronger than most good harvest years, there is little basis risk in selling physical for harvest cash flow. There is always production risk, with the crop a long way from finished, but there could be plenty of harvest pressure if prices remain strong.

With cereal prices falling, canola might be the first to go, so there could be some merit in selling some prior to harvest to ensure a relatively good price can be secured.

Have any questions or comments?

Key Points

- Canola prices have been falling in line with Matif values over the last two months.

- Local canola basis remains relatively good, while absolute values have rarely been higher.

- Selling some physical canola prior to harvest might be a good way to avoid harvest pressure.

Click on graph to expand

Click on graph to expand

Data sources: Matif, ICE, Trade, Mecardo