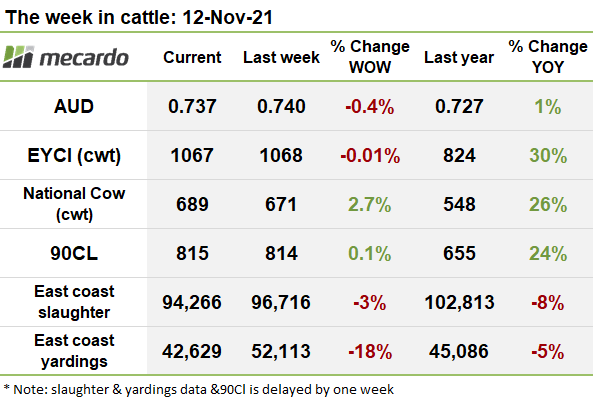

The story of low yardings, tight supply & high prices rolls on in the Aussie cattle market. The rain that has landed in paddocks this week, and the forecast, will keep things that way for the foreseeable future. International demand for Aussie beef also remains very strong.

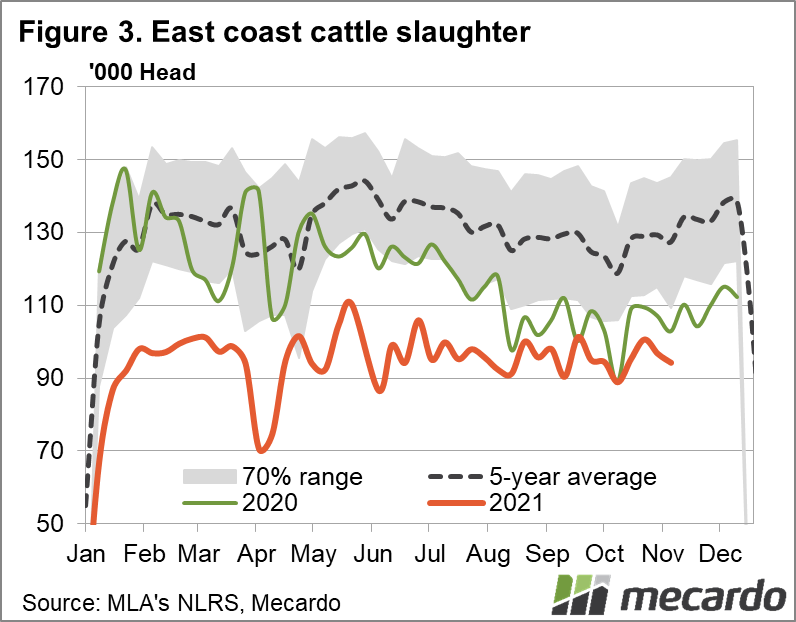

On the East Coast, yardings dropped by around 10,000 head for the week ending 5th November 2021. 42,629 head went to the saleyards last week, 18% lower than the week prior and 5% lower than this time last year. Slaughter levels remain subdued and well below recent historical averages (figure 3). 94,266 head of cattle were slaughtered last week, 3% lower than the week prior and 8% lower than this time last year.

The Eastern states Young Cattle Indicator (EYCI) slipped back just 0.01% on last week, to finish this week at 1067.49¢/kg cwt. The EYCI has averaged 1067¢ for the past four weeks now, which is 30% higher than this time last year.

The top four key EYCI contributor markets all lifted on last week, except Wagga Wagga, which was the largest contributor, at 19%, to the EYCI 7-day rolling average. Dubbo, Roma Store & Dalby were all stronger, with Roma Store average prices coming in at 1137¢/kg cwt, a 6% jump up on last week. 7 day rolling averages at Dalby and Dubbo are sitting at 1078¢/kg cwt & 1112¢/kg cwt respectively.

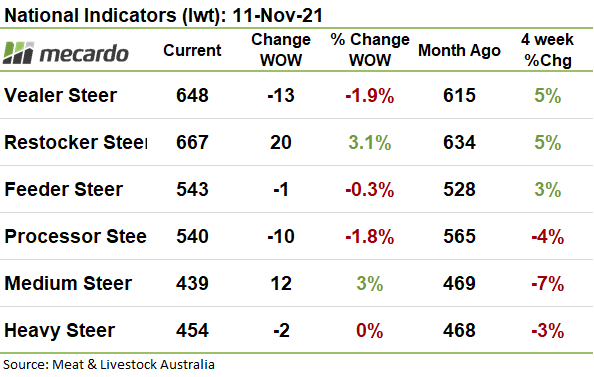

The National Indicators were mixed this week, with the Restocker Yearling Steers leading the charge upward with a new record, up 20¢ on this time last week, at 667¢/kg lwt. The Medium Steers & Medium Cow Indicators also lifted on last week, up 12¢ & 10¢, to finish this week at 489 & 372¢/kg lwt respectively.

Vealer & Processor Yearling Steers recorded the biggest falls week on week. The Vealer Steer Indicator dropped 12.5¢ (<2%) to 648¢/kg lwt, still 183¢ stronger than the same time last year & 5% higher than this time last month. The Processor Yearling Steer Indicator dropped by about the same amount to finish this week at 540¢/kg lwt, still up 112.5¢ on this time last year.

90CL frozen cow prices are still historically very strong, up another 1¢(<1%) on last week to close at 815¢/kg swt. US Steiner reports meat inflation continues to outstrip broader food inflation in the US, with beef prices surging higher than any other proteins there. They also note the imported beef market is ‘somewhat disjointed’, amid tight supply from Australia and supply chain disruptions, making trade ‘especially difficult’.

The week ahead….

The dump of rain across much of the country (despite disrupting harvests and causing flooding in some parts), will continue to fuel the restocker cattle market fire, maintaining pressure on supply and prices.

The BOM recently updated their ENSO outlook this week, predicting a 70% chance of La Niña forming in the coming months. This will no doubt give cattle producers even more confidence to purchase new stock and breed up, further consolidating the tight supply situation.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: MLA, Mecardo, BOM