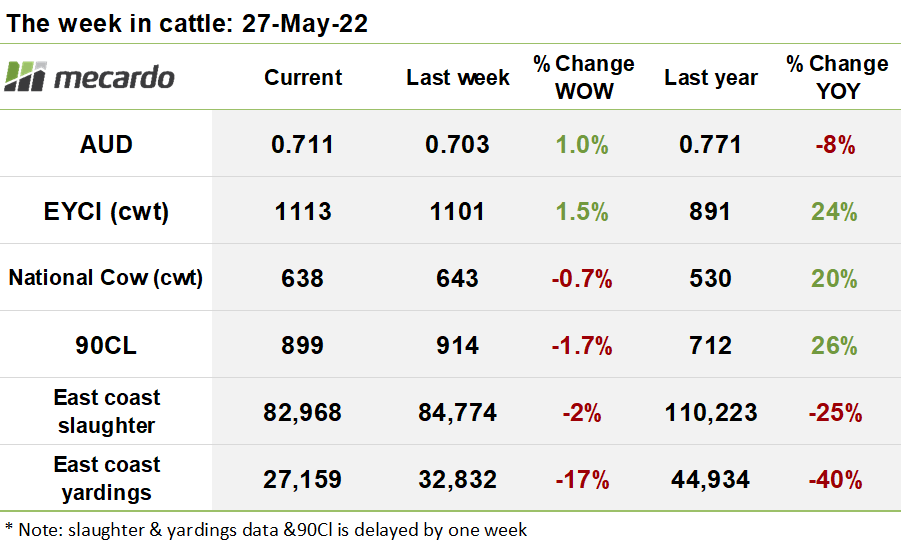

This week contained firm indications that there has been an influx of cattle back to the yards, but despite the higher supply situation, the EYCI was resilient to the downward pressure, improving week on week. Other specifications were not so well supported by demand though with minor falls booked for many of the national indicators.

East Coast slaughter volumes lost ground by 2% on week, falling to 82,968 head for the week ending the 20/05/2022. This was no surprise given the presence of wet weather in QLD that was the cause of logistics problems last week, with numbers stagnant in the big cattle state. Week on week, VIC volumes fell 9%, and SA by 22%. This is the time of year when slaughter typically accelerates, so hopefully the processors will try and operate at full steam to catchup in the coming weeks if the supply situation accommodates it.

Again, because of the QLD wet weather which lead to the cancellation of the Roma Sale on the 17th, among others, the very soft yardings numbers for last week were no surprise. Overall, yardings for the week ending 20/05/2022 slumped 17%, with QLD volumes dropping 24% week on week, and NSW offerings by 23%. Roma returned to operation this week, but reports were that yardings were subdued again this week, at only 2,112 head, with a reduced restocker and processor buying panel in attendance. In contrast, the regular contingent of feed and trade buyers attended the Dalby saleyard this week, with exporters also in attendance.

This week’s supply situation appears to have improved markedly, with EYCI eligible cattle volumes increasing 36% week on week to 9,928 head.

Despite the notionally higher supply this week, indications are that the EYCI was well supported by solid demand, rising another 12¢(2%) to 1,113¢/kg cwt.

Over in the west, the WYCI shed 10¢(1%) to settle the week at 1091¢/kg, with price suffering from a 75% increase in supply, with yardings at 766 head.

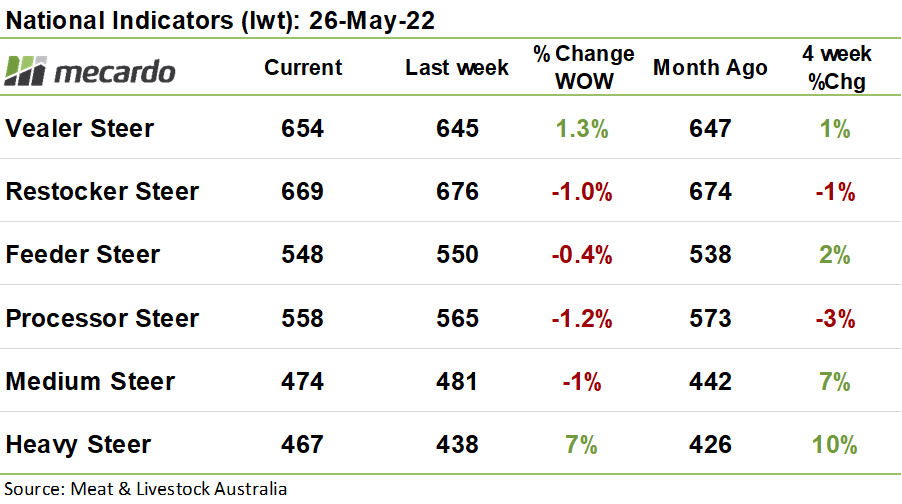

The national cattle indicators were generally downbeat, with most specifications copping minor falls of below 1%. The wooden spoon went to processor steers which lost 7¢(-1%, closing the week at 558¢/kg lwt. The big winner for the week was heavy steers, which bounced 29¢(7%) despite the downward pressure of a 40% larger yarding this week of 169 head.

The US frozen cow 90CL price dipped 2¢(1%) to settle at 285¢US/lb, and lost 15¢(2%) in Aussie dollar terms, closing the week at 899¢/kg swt, with the strengthening in the aussie dollar we saw last week subduing prices. High domestic cow slaughter continues to provide more than adequate lean grinding beef supply in the US, with traders reluctant to bid up imported prices in the near term.

All the action is in pricing is for Q3, where a premium still exists. The good news is that the volume of Brazilian beef coming into the US has slowed down to a trickle since the quotas were imposed, with YTD import figures from the USDA indicating only 4,400 tonnes above quota have entered the US for the year so far.

The week ahead….

Supply seems to have made a solid return this week and given that yardings have been very subdued over the last couple months due to holidays and weather events. We can expect some more of the same in the next few weeks due to accrued backlog. The question is whether demand will remain robust enough to support prices. Softer pricing outcomes next week would be no surprise.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: MLA, Mecardo.