The quarterly Australian Bureau of Statistics (ABS) livestock slaughter and production data dropped late last week. There were a few surprises on the lamb front, with a solid lift in slaughter, at the expense of weights.

A few years ago, the (ABS) gave up supplying monthly livestock slaughter and production data and moved to quarterly. While we can get the slaughter data from Meat and Livestock Australia, the ABS numbers are accompanied by production data. Understanding the weight of lambs that are slaughtered can give us an interesting insight into the attitudes of growers. The now quarterly data come six or seven weeks after the quarter and makes seasonality analysis difficult in three-month blocks. Regardless, we can glean some insights.

While seasonal conditions are now vastly different across major lamb-producing areas, back at the start of the year things were wet, too wet in most cases. The general consensus was that the wet spring and early summer were going to make it difficult to put weight on lambs.

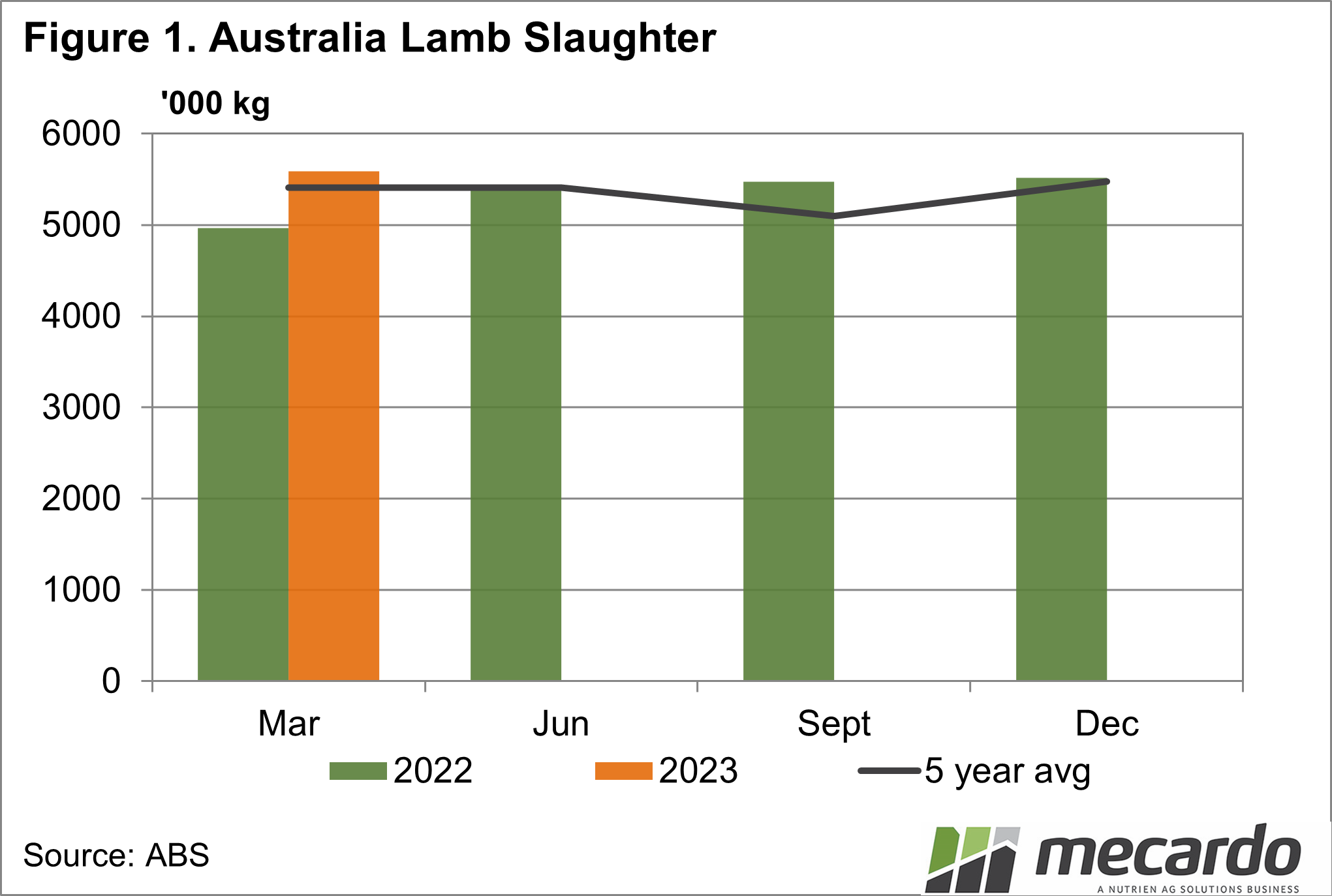

The ABS March quarter data, combined with the December quarter, confirms this. Figure 1 shows lamb slaughter in March was up on December, albeit by just 1.3%, but the first quarter is usually lower than the previous.

The big increase was seen relative to 2022, with lamb slaughter up 12% on the year earlier. March lamb slaughter was 5% off the record seen in 2016, but the strong number is at least some indication that processors are getting back somewhere near full capacity.

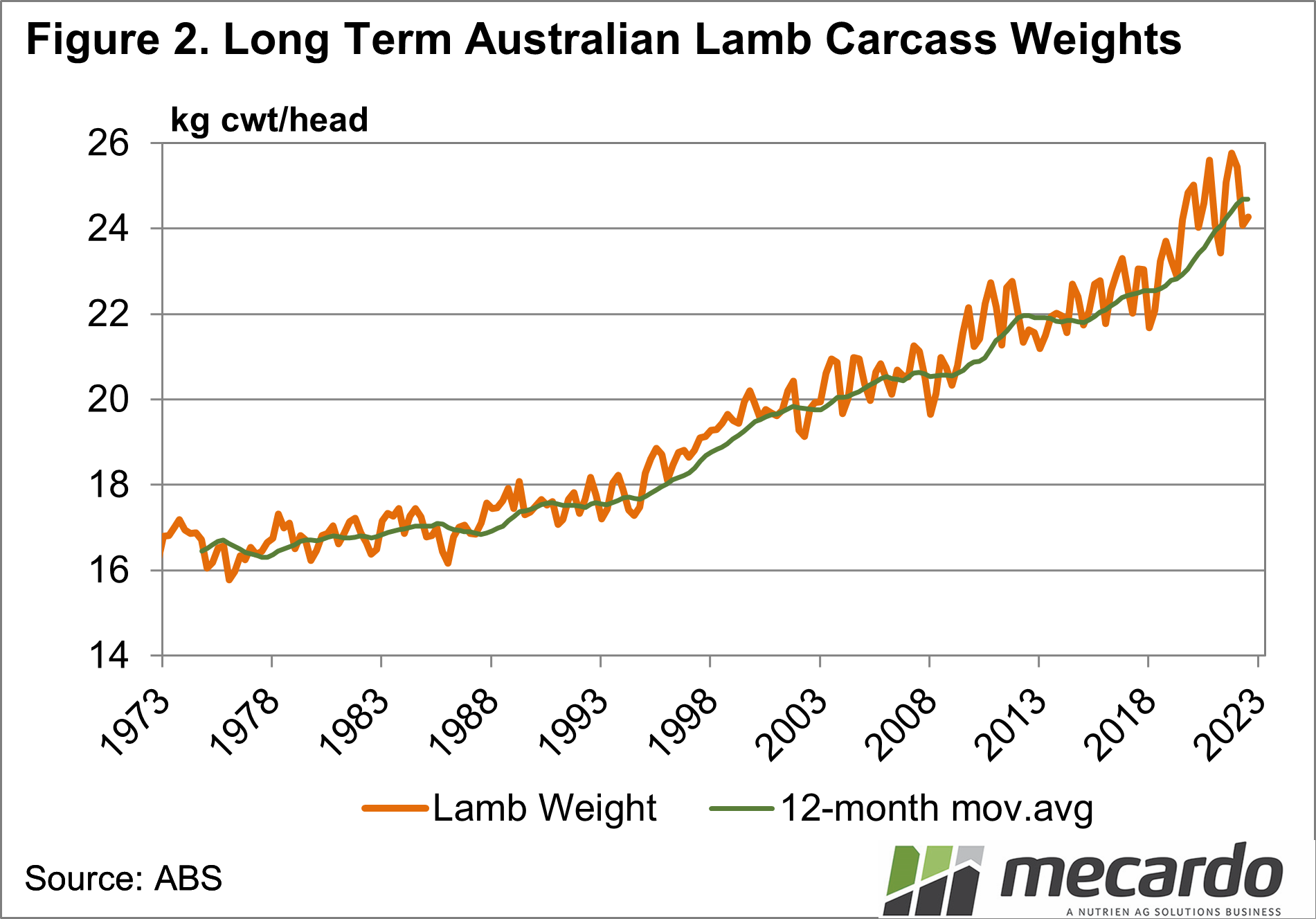

The production of lamb meat was up last year, but the increase was 9%, and as such lamb slaughter weights were down (Figure 2). It should be noted that lamb slaughter weights were at a record 25.1kg/head in March 2022, and the fall to 24.3 kg this year still has weights above the five-year average of 24 kg.

The decrease was 3% and reflects the difficulties in finishing lambs. It is in fact a little surprising that weights were above 24kgs, given the season. With heavy lambs commanding a premium, there was an incentive to get more weight on lambs early in the year.

Despite the strong March quarter, lamb slaughter looking forward is going to have to lift further to meet MLA’s forecasts. To achieve the 22.63 million head forecast, the quarterly slaughter will have to be 5.68 million head, up 1.7% on the March figure.

What does it mean?

Supply and demand are working in the lamb market. Supply was up in the first quarter, and prices were down. With lamb supply still increasing as per the MLA forecast, lamb prices continue to fall in the second quarter.

The September quarter is traditionally the weakest for lamb supply, and we might move back to more normal seasonality this year in time for new-season lambs to enjoy a bit of a price boost.

Have any questions or comments?

Key Points

- Lamb slaughter was up in the March quarter, well ahead of last year as expected.

- Slaughter weights were down on 2022, but still strong compared to historical levels.

- To meet annual forecasts lamb slaughter will have to be higher for the remainder of the year.

Click on figure to expand

Click on figure to expand

Data sources: ABS, Mecardo