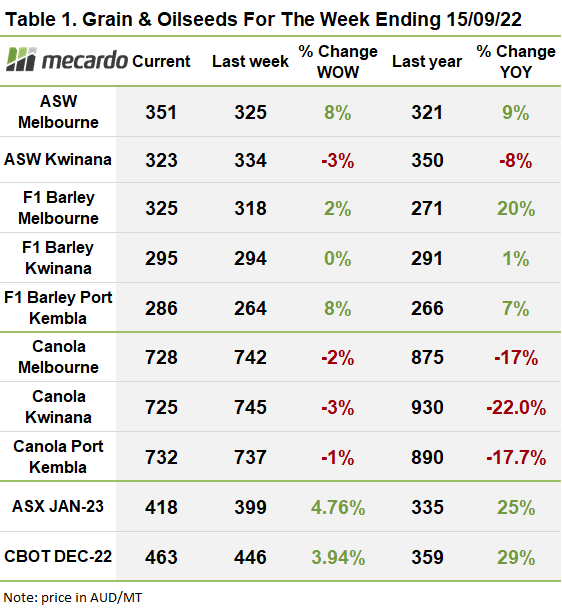

The USDA released their WASDE report earlier this week. Wheat stocks and production numbers were within expectations, if anything a little higher. Russian production has officially been beefed up to 91mmt (+3mmt) which weighed on the market as major exporter inventories are seen as rising slightly.

The report was always going to be significant. Many straw polls were predicting a sizeable cut to corn production so the market was watching not whether it would be cut, but by how much. The USDA didn’t disappoint with US corn yield trimmed from 75.4bu/ac to 72.5bu/ac, which was within trade estimates but still significantly tightens US carryout. Significant too is the year on year drop in global supplies of corn with stocks to use now only 12.5%.

But it was soybeans the major winner, or loser depending on your perspective. Most in the trade were expecting an unchanged or even an increase in US soybean production. So dropping the yield by 1.5bu/ac to 50.5bu/ac caught the market off guard. This tightens US carryout to only 4.5% stock to use and the lowest in 9 years.

Geopolitics remains centre stage in global markets as well. Last week, Putin stirred the pot claiming that Ukraine and NATO had effectively ‘cheated’ the world’s poor by allowing Ukrainian grain exports to go to Europe instead of ‘those who need it’. The comments are a little disingenuous as Europe has for a long time been a major importer of Ukrainian corn and oilseeds. What it has done is throw an element of doubt over the grain corridors on-going success. Consequently, we have seen risk premiums start to build in ag commodities again.

Putin is also fighting a war on multiple fronts, and those are not going well. A Ukrainian counter offensive in the North and South of occupied Ukraine has being hailed a military master stroke and is reportedly sent the Russian forces in to a fully fledged retreat.

Market analysts are split on whether this means a potential end to the war, or an escalation. A cornered bear tends to fight back and with a nuclear arsenal at his disposal, it doesn’t warrant thinking about the repercussions. I can’t help think that we are a long way from this being resolved.

The week ahead….

We are seeing a premium build in the wheat market again. It is going to be a busy week for Russian President Putin who will meet with the UN to discuss the grain corridor and then travels to meet Chinese president Xi. Oh and he survived an apparent assassination attempt. All of these things have the potential to shape the wheat market in the coming weeks and months.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Data sources: USDA, Reuters, Mecardo.