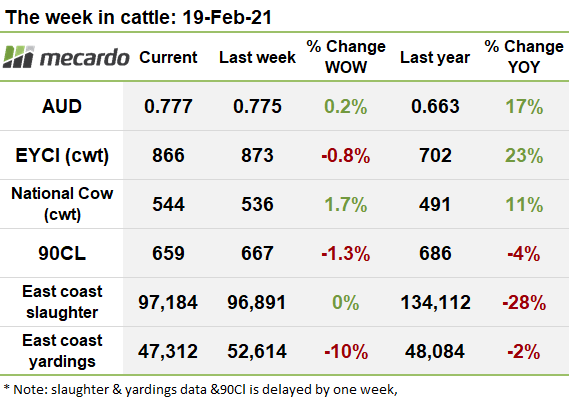

A lacklustre week, where prices have slid marginally across most categories, with the exception of medium cows, which have strengthened to levels not seen for several months. Prices seem well supported by the general lack of supply, indicated by stubbornly low slaughter rates, as producers continue to take advantage of feed on the ground, and retain breeding animals. Yarding’s are still relatively strong, so a preference towards live sales as opposed to over the hooks seems evident.

After seeing a solid lift back to typical average levels recently after a very slow start to the year; yardings slumped 10% last week. The fallback emanated from all states apart from VIC, with NSW dropping 15%, and QLD by 7%. This fall isn’t particularly unusual for the time of the year though, as history tells us that national offerings tend to dip a bit in the second week of February, and we are only 2% down from 2020, and 8% down from the 5-year average.

A total of 47,312 head were yarded on the east coast for the week ending 12th February 2021.

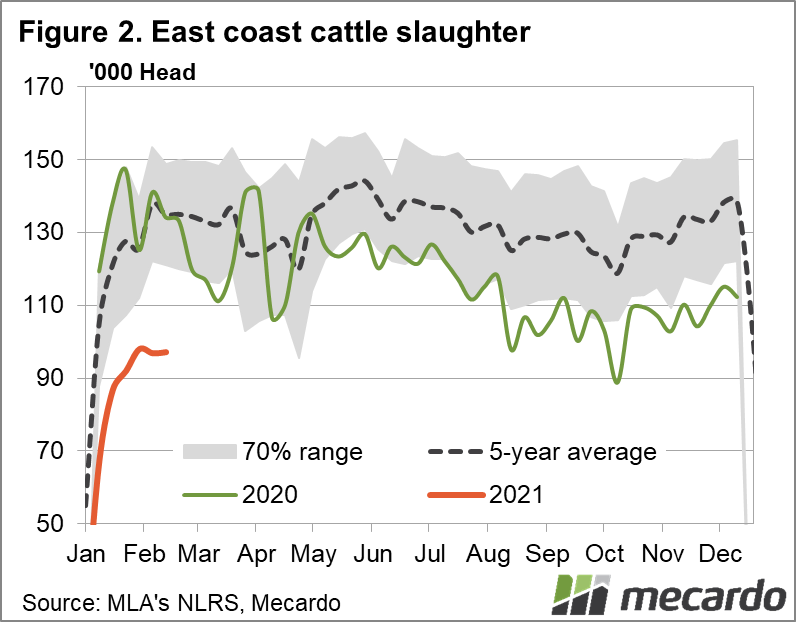

Slaughter was overall on par with the prior week reported, however, the distribution across the states shifted slightly, with VIC seeing a pickup of 16%, however, slaughter is still 28% below last year, and the 5-year average.

For the week ending 12th February, 2021, 97,184 head were slaughtered, which was up a marginal 293 head from the prior reporting week.

The EYCI has continued to slowly slide backwards, losing 7¢ (<1%) this week to settle at 866¢/kg cwt.

The categories universally backed off this week, with heavy steers and restockers backtracking the most, while medium cows bucked the trend and strengthened to levels not seen since November last year.

Restockers fell back 10¢ (-2%) to 525¢/kg lwt, while heavy steers collapsed by 12¢ (3%) to finish the week at 366¢/kg lwt. Feeder, processor and medium steers all stuttered marginally by -1%, to respectively close at 457¢/kg lwt; 437¢/kg lwt, and 399¢/kg lwt.

Medium cows staged a turnaround from falling last week, to rise 9¢ (3%) this week up to 294¢ ¢/kg lwt.

The Aussie dollar strengthened this week by 0.2% to 0.777US. All is not looking well in the US though, with jobless claims accelerating, and housing starts faltering also, so depreciation of the US dollar, and a higher AUD as a result is probably on the not-too-distant horizon. The Aussie banks are mostly tipping an 0.80+ AUD that could persist for years into the future, which will put pressure on our export competitiveness.

90CL fell back 8¢ (1.3%) last week, but this was all stemming from pressure from the rising AUD, as prices in USD were stable. Declines in supply from NZ have resulted in elevated import prices in the US, and buyers are awaiting opportunities to take advantage of lower prices when the seasonal NZ cow slaughter end export volumes pick up.

The week ahead….

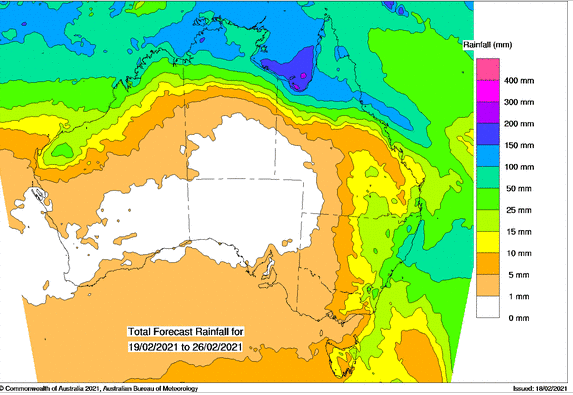

A healthy smattering of rain is forecast for the coming week, with 5-25mm expected to fall across most of the east coast, though further inland is looking to be considerably less generous. As we enter late February, yardings typically tend to pick up around 15-20%. With slaughter and supply still so low, and no end in sight due to restocking activity keeping cattle fattening in the paddock and cows retained longer than normal, good support for prices is likely to remain next week.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: MLA, Mecardo, BOM