Two months is a long time in grain markets, especially when volatility is rampant. Local new crop wheat prices remain very strong, yet at the same time relatively cheap. Compared to two months ago, they are off 20%, but relative to international values they are priced much better now.

The decline in Chicago Soft Red Wheat (SRW) Futures and both ICE and MATIF Canola and Rapeseed futures has been well documented in recent weeks. There is every chance prices could rebound when northern hemisphere harvest pressure comes off, which means the spreads we see now might be as good as they get this harvest.

Figure 1 shows SRW has collapsed under the weight of the US harvest. The 30% fall has been helped by fund money looking for safer investments. Locally, ASX Wheat Futures didn’t fully participate in the rapid price rise, peaking at $495/t, compared to $668/t for SRW. The local price spread was an extraordinary -$173/t. Not that long ago $173 was the price of wheat.

The fall on ASX has been more benign, but still came in at 14%. This week ASX wheat futures are at $420/t, while SRW is back at $500, having bounced $35 in recent days. The ASX discount got in as close at $40, but now is back out to $80, such is the volatility in the market at the moment.

The trends in canola markets has been similar in recent weeks, a heavy fall before a bit of a kick late last week. The local spread for the new crop market has come in from $500 to $200. This is despite canola having lost nearly $200 to sit at ‘just’ $860/t.

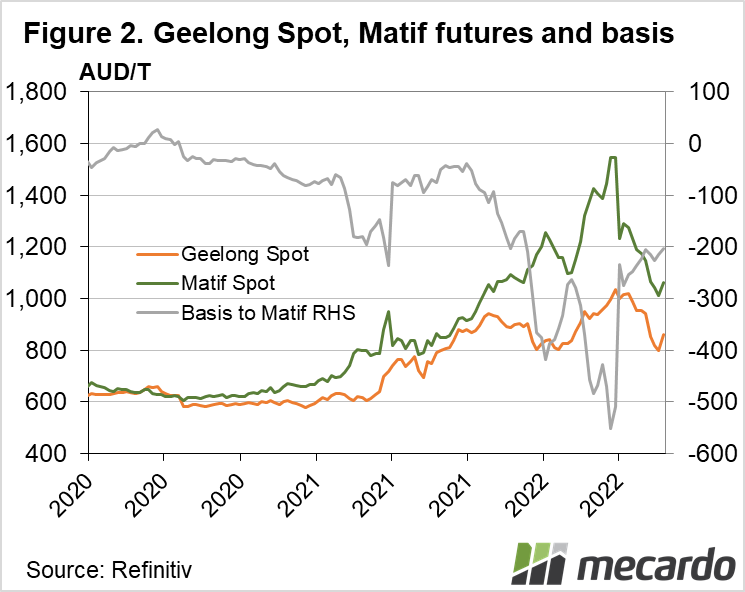

The decline in MATIF Rapeseed prices, at over $500/t, has been extraordinary, and anyone who took out futures or sold swaps in the last six months would be sitting pretty. Figure 2 shows that the local price discount is still very large compared to normal levels of $50-100/t.

What does it mean?

Using swaps in the current environment is riskier than normal, as shown by the massive swings in basis recently. While local prices are very weak compared to international levels, which would normally suggest using futures and leaving the basis open. Those who punted on this happening a couple of months ago can bank some serious profit now.

Most growers will be holding off on prices still, which also makes plenty of sense as prices are still in the highly profitable range.

Have any questions or comments?

Key Points

- Heavy falls in international grain and oilseed futures haven’t been matched in local markets.

- The decrease in the spread makes local futures or physical prices better value.

- Using swaps is risky in such volatile times, but can have big rewards.

Click on figure to expand

Click on figure to expand

Data sources: Refinitiv, CME, ASX