Crossbred wool prices continue to languish at depressed levels although the supply chain is absorbing most of the increased offerings of this type of wool in Australia. Basically crossbred prices followed the general lead of apparel fibres into mid-2020 but since then have not recovered. This article takes a long term look at 28 micron and polyester staple fibre prices.

Before looking at the long term price data in this article there are a couple of points to note. Firstly the markets have changed with time. In the early 1970s the man-made fibres were still early in their development which means volumes were still relatively low, compared to the traditional fibres, and the cost of production was being pushed down at a fast rate relative to the traditional fibres. The second point is the price series are a mix of series, some calculated, which are not always strictly homogenous, cobbled together in order to build a long terms series. As such there will be some errors in the series.

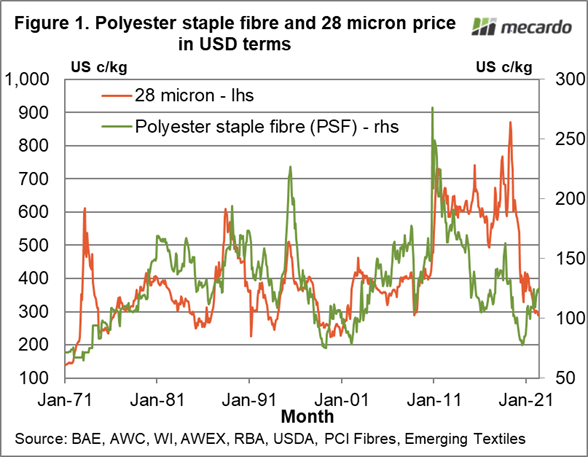

Figure 1 compares price series for a 28 micron crossbred wool category and polyester staple fibre (PSF) in US dollar terms from 1971 to this month. The two series have a variable relationship, generally following similar trends and cycles. In the most recent decade the 28 micron price held at relatively high levels after 2012, while the polyester staple fibre price fell to low levels in 2016 before rising into 2018 and then falling again in 2019.

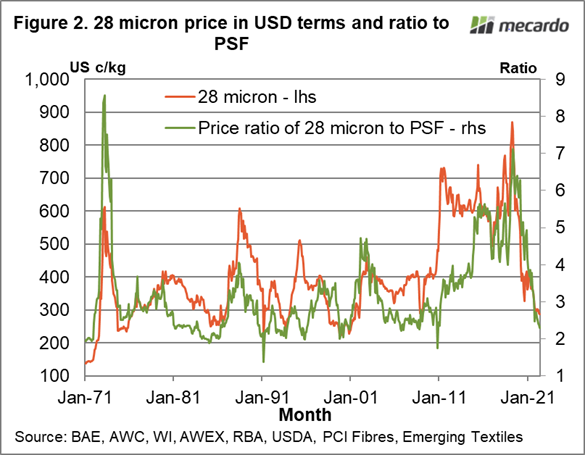

In Figure 2 the price ratio of the 28 micron series to the PSF is shown along with the 28 micron price series. As a rule since the early 1970s a price ratio around 2 has been the low (with exceptions for early 1991 in the aftermath of the collapse of the Reserve Price Scheme and in late 2010). The ratio is now around 2.3, close to the long term support level.

The late 2010 low ratio is interesting as that happened as a rampant cotton market was pulling apparel fibre prices higher and did so through to mid-2011. The cotton market is once again on the rampage, trading at extremely high price levels and rising.

The cotton cycle helped drag the 28 micron price above US700 cents in 2011, and it stayed until 2016 roughly between US600 and 700 cents with strong demand reported for crossbred wool for use in fake fur for teddy bears and fabrics which are used in coats. The price ratio shows that through to 2014 the 28 micron price was not expensive in relation to PSF.

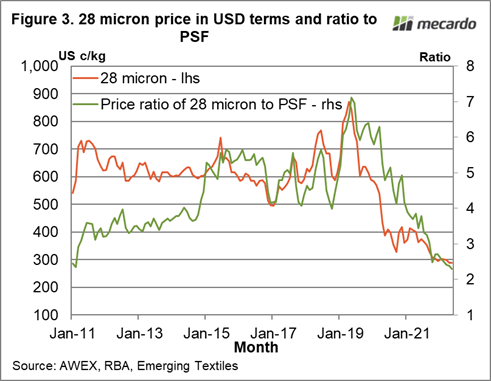

Figure 3 narrows the series shown in Figure 2 down to the 2011-2022 period. It shows the price ratio lifts to the range between 4 and 7 for the period 2015 to 2019 (helped by a very strong merino market in 2017-2019), spending 2019 above 6, and then it collapses. A quick look at fake fur and teddy bear coats on line this week shows that most are 100% polyester with some still with 30% wool. The plausible story about current low crossbred wool prices is that demand destruction took place in the 2015-2019 period for which crossbred wool is now paying.

What does it mean?

While history does not tell us what the future holds, it does improve our understanding of why things happen, such as depressed crossbred prices. In the past decade it appears crossbred prices were dragged higher by the extraordinary cotton market of 2010-11, then held there by a boom in fake fur/teddy bear fabric with the high crossbred price extended by a very strong merino market in 2017-2019. The extended period of high crossbred prices appears to have caused demand to change enough for crossbred prices to fall to their current low (by any measure) levels.

Have any questions or comments?

Key Points

- The 28 MPG is low in relation polyester staple fibre prices.

- It appears likely that high crossbred prices in relation to polyester (and acrylic) prices in the 2015-2019 period caused demand destruction for crossbred wool.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: BAE, AWC, WI, AWEX, RBA, USDA, PCI Fibres, Emerging Textiles, ICS