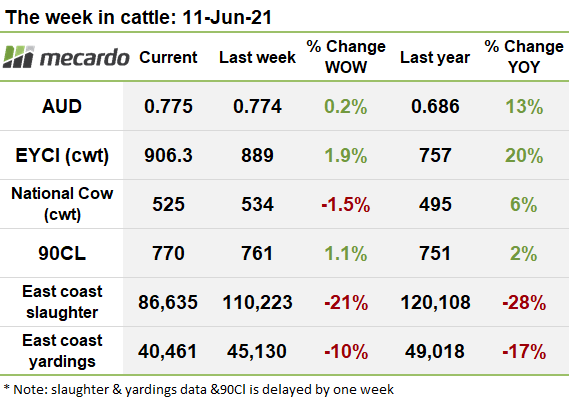

After struggling for many weeks to gain altitude, the EYCI has finally risen to a new all-time record of 913ȼ/kg cwt. The impact of the cyberattack that brought JBS processing to a standstill, before returning earlier this week, had no discernible negative impact upon the market despite slaughter being 21% down, offset by lower supply with yarding’s down 10% as producers held back stock.

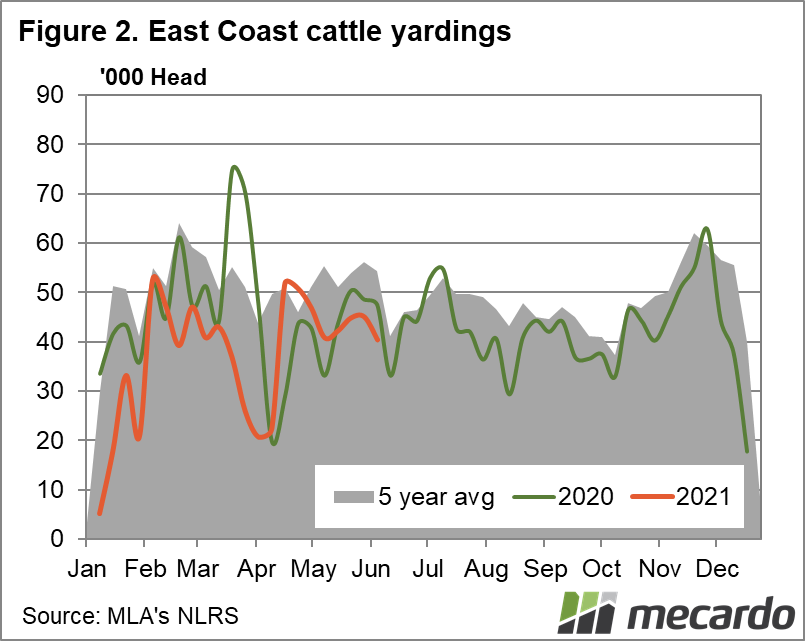

East coast Yardings plunged 10% last week from the week prior, with the largest falls emanating from QLD and VIC, which both fell 14%, while SA numbers fell 30%. NSW throughput, however, was unfazed.

A total of 40,461 head were yarded on the east coast for the week ending 4th Jun; 2021, down 4,669 head from the week prior.

Online, at AuctionsPlus, 18,982 head were yarded, up 9% on the prior week, with clearance rates of 100% for steers and heifers under 200kg, compared to the overall clearance rate of 65%; reflecting high demand for lines of light cattle.

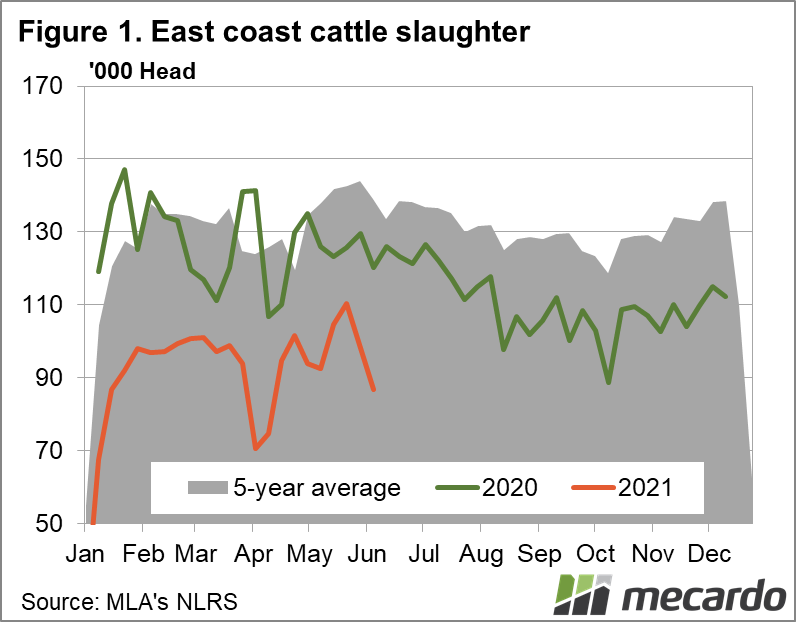

Slaughter last week was severely impacted by the JBS shutdown, clocking in a 21% reduction from the last available figure from the 3rd week of May, with slaughter in QLD and NSW representing the majority of the fall, down 26% and 21% respectively.

Overall, 86,635 head of cattle were slaughtered for the week ending 4th Jun, 2021; which is down 23,588 head from the last recorded week in May.

The EYCI reached a new all time high of 913ȼ/kg cwt this week, finally breaking away into a new range after meandering in a tight 875-900 range for the last six weeks since the last high of 910ȼ/kg cwt in late April.

On the national categories, processor steers saw solid gains of 17ȼ(4%) to reach 474ȼ/kg lwt, and vealers charged skyward by 26ȼ(5.1%) to 537ȼ/kg lwt. In contrast, heavy steers, medium cows and feeders respectively shed 5ȼ(1%), 5ȼ(1%) and 1ȼ(<1%) to settle the week at 399ȼ/kg lwt, 284ȼ/kg lwt and 446ȼ/kg lwt.

The Aussie dollar strengthened 0.2% to reach 0.775US. US CPI, or inflation figures surprised the market again, hitting 5% for May. However, the general view is that the price inflation apparent at present will be transitory, and stimulus policies will not be adjusted in response.

The 90CL frozen cow price continues reaching for the sky, pushing up to 770ȼ/kg swt this week, with clearly no end in sight for the tight supply situation in the US as they struggle to source labour to process domestic beef, and imported beef volumes continue to be limited.

The week ahead….

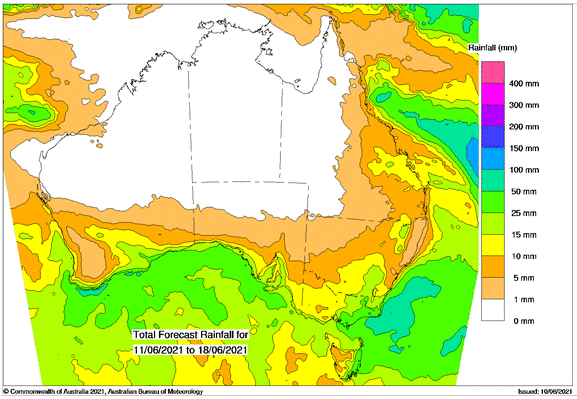

In the coming week, we have a respectable 10-15mm of rainfall due all down most of the east coast, and with JBS back, it can be expected that a few more cattle are likely to come to market than last week, bucking the usual trend for lower yardings as we move through June; though this impact is likely to be temporary. However, it wouldn’t be surprising if post JBS shutdown slaughter numbers also lifted against the typical trend as a focus returns to ensuring that committed beef orders can be serviced; offsetting the potential increase in supply.

Have any questions or comments?

‘last weeks‘ slaughter figures are from the week ending 21.05.21

Click on graph to expand

Click on graph to expand

Data sources: BOM, MLA, Mecardo