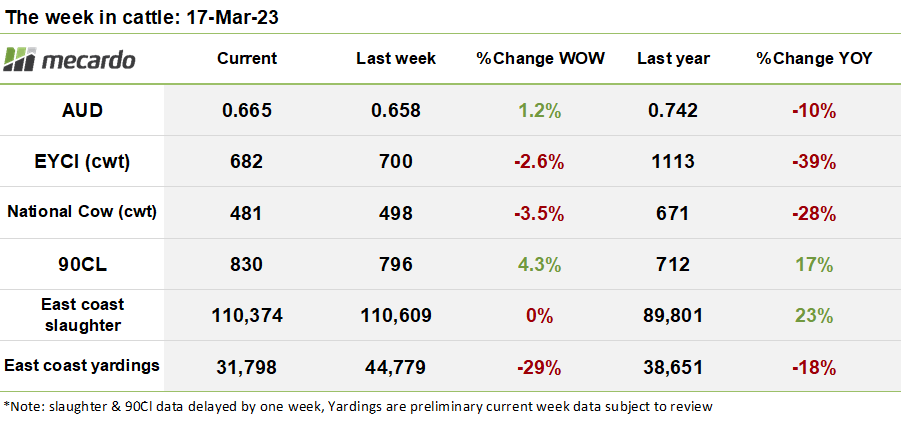

The EYCI has reached its lowest point since February 2020, but part of that can be traced back to the index becoming more southward-biased as yardings in the north fall back due to inclement weather. 90CL in the US continues to sizzle, with forwards for lean imported beef deals clocking in big premiums.

The Eastern Young Cattle Indicator (EYCI) continued its backward slide, losing 18¢ (3%) this week to close at 682¢/kg cwt; the lowest price seen in around three years. The fallback in Queensland (QLD) yardings recently has lessened the state’s influence on the index. This is evident as Gunnedah, NSW, stole the crown from Roma store as the top contributor this week with 11% of the index. To put the importance of this North/south divide into context, Roma Store steers moved at 859¢/kg cwt and Gunnedah steers sold this week at 704¢/kg, (a 155¢/kg (18%) discount to Roma prices).

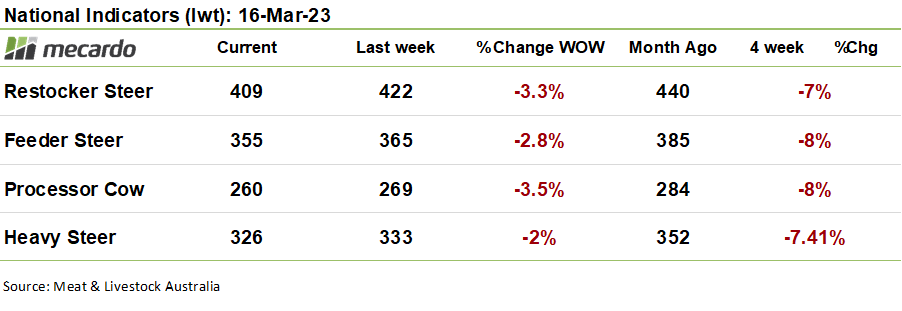

In the north, feeder cattle prices continued to drop, with buyers resolute not to overpay despite the constrained supply situation, while the national indicators were a sea of red, with both restocker, and finished cattle prices falling across the board.

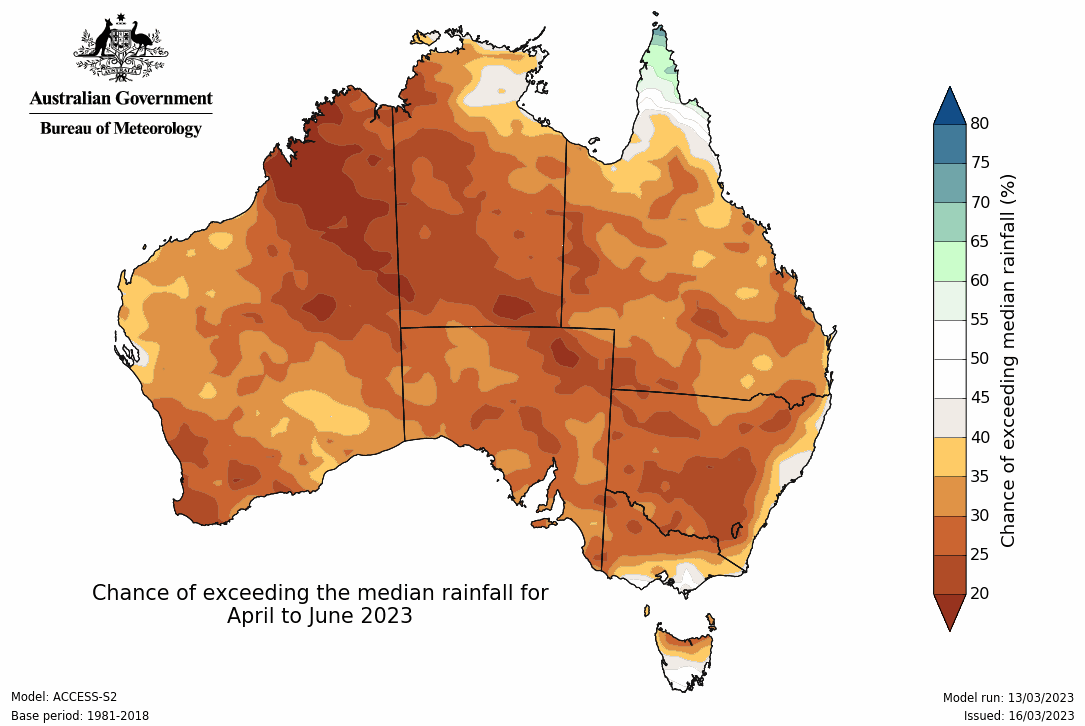

Overall cattle supply on the east coast weakened considerably this week, with preliminary figures indicating that yardings fell 29%, or 13K head down to 31,798 head. Logistical constraints on getting stock to market due to heavy rainfall across QLD cattle country have been a primary driver in this case. The impact is evident this week as QLD only yarded 7K head, 68% below where weekly yardings were a fortnight ago. In contrast, NSW yardings only fell back 2% week on week. The rain in the north was a welcome sight for those looking to hold onto cattle, but this may prove to be temporary if the Bureau of Meteorology’s 3-month forecast of below-median rain eventuates. Slaughter continues to trend around 20% above the prior year’s figures, however, we may see a fall in throughput next week in response to the wet.

US frozen cow 90CL price have continued their sizzling rally last week, jumping 34¢ (4%) to finish up at 830¢/kg swt. Increased domestic demand in the US for lean beef has been driven by US buyers looking to cover their needs for Q2. Sellers have taken advantage of the deteriorating supply situation in the US and bumped up prices to capture premiums in future periods. Steiner reports that there have been forward deals transacted for May/June delivery at a 5-10% premium, which translates into a 260-274¢/lb price, or up to AUD 900¢/kg swt. Steiner cautions, however, that steep premiums like these rarely last long, however, some US forecasters in the trade have made dire predictions of 300¢/lb (~987¢/kg AUD) for US domestic prices by this July. Conditions for US cattle producers have continued to improve, with the percentage of US cattle located in drought falling from 53% to 46% over the last month, driving decreased turnoff, and encouraging rebuild intentions.

Brazil has now reportedly shared all relevant information with China about the Atypical BSE case that occurred on February 23rd, and it is expected that any news about a lift of the ban will probably occur on or prior to when Brazil’s president visits China on the 28th of March. Closer to home, however, Brazil’s agricultural minister Carlos Fávaro held trade talks with the Australian Ambassador to Brazil, Sophie Davis regarding agricultural trade agreements. Of interest to Australian beef producers is the potential of Brazilian pork imports into Australia. Cheaper beef substitutes in an environment of increasing cost-of-living pressures for domestic consumers could result in a dent in domestic beef demand in Australia.

The week ahead….

As ground begins to dry off in QLD, and loading cattle becomes easier, we may see a surge of supply come back into the QLD marketplace again. On the other hand, the dose of rain will also provide an opportunity for some producers to push back their turnoff intentions for a while. In general, the BOM’s drier-than-average rainfall outlook over winter isn’t a strong source of confidence for many and is likely to encourage turnoff over time.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: MLA, Steiner, Bureau of Meteorology, Argus, Mecardo