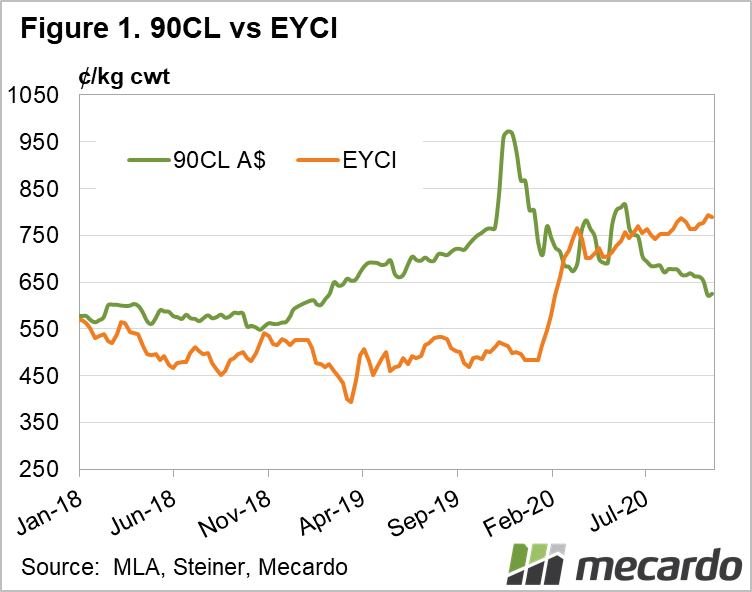

After spending all of 2019 trading at a discount of at least 100¢/kg to the 90CL price, the Eastern States Young Cattle Indicator (EYCI) has spent the majority of this year well above it. The 90CL - a benchmark price for frozen manufacturing beef into the US - has been losing ground this month, while the EYCI - Australia’s go to price point - has been on the rise. Price movements in the two have historically trended together, until last year when global beef demand pushed the 90CL sky high, and Australia’s ongoing drought kept domestic cattle prices in check. This year, widespread rainfall has brought about a complete reversal, and the EYCI currently sits 166¢/kg above the 90CL indicator.

Why the disparity? Let’s look at the EYCI first. Just a fortnight ago it reached another all-time record high of 794.25. This was 310¢/kg above the same time last year, or nearly 60% higher. Up until now this has still been driven predominantly by the change in seasonal fortunes creating strong restocker demand. Meat & Livestock Australia reports that throughout September, restockers operating on EYCI eligible cattle paid 94¢/kg more than processors, and 68¢/kg more than lotfeeders.

In comparison, the 90CL price indicator is 20 per cent lower year-on-year, and at 621.9¢/kg, has dropped nearly 5% in the past week alone (remembering that 90CL figures are one-week delayed). According to Steiner Consulting Group’s latest US update, this price decline is primarily supply driven, with 25% more imported beef landing in the US for the four weeks to October 10, than the previous year. Imports from New Zealand (up 164 per cent on the same period last year), Brazil and Argentina have all increased, and are seen as operating at a more affordable price point for importers, while of course supply from Australia remains tight and prices sky high.

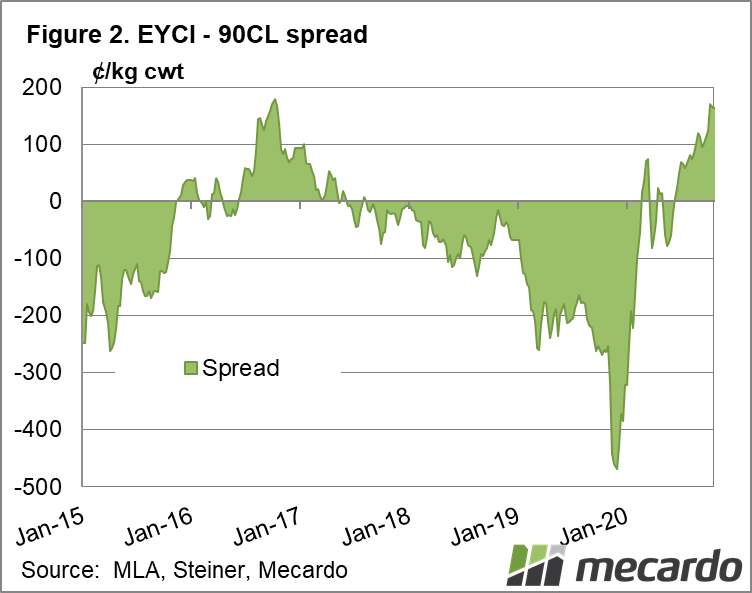

The most recent example of the EYCI operating higher than the 90CL, as pointed out above, was in 2016-17, when cattle prices in Australia were last on a record run, and we all watched it break the previously elusive 700¢/kg barrier. In that case, the EYCI premium lasted for a majority of the 18 month period, and reached a maximum price divide of 180¢/kg. What turned it around last time? Seasonal conditions started to deteriorate, and the herd rebuild had reached a stage of more ample supply. This teamed with record high global demand reversed the premium until the 90CL was close to 470¢/kg above the EYCI.

What does it mean?

If we use the ECYI-90CL spread to predict how long this record run of domestic cattle prices will last, there’s still plenty of positivity to come, especially if seasonal conditions remain favourable. However, last time around demand wasn’t under the cloud of looming global recession due to Covid-19, so regardless of domestic supply, export volumes could change the game.

Have any questions or comments?

Key Points

- EYCI is trading at 166¢/kg above the 90CL price, as restockers push domestic cattle prices higher and ample supply holds US import returns back.

- The last time the EYCI was at a premium the domestic cattle price was also on a record run, in 2016-17, and the price differential peaked at 180¢/kg.

- Within two years, this premium reversed to the 90CL trading at close to 470¢/kg above the EYCI in late 2019.

Click on graph to expand

Click on graph to expand

Data sources: MLA, Steiner consulting, Mecardo