Mecardo last looked at fibre prices in early February, concluding that uncertainty due to COVID-19 had a reasonable chance of leading to lower prices. This has proved to be a genuine understatement, with lockdowns around the world introduced in the second half of March leading to order cancellations along supply chains and plunging prices. We have another look at apparel fibre prices in this article.

The effect of lockdowns in many countries has meant the economic effects of measures to slow the spread of COVID-19 are both wide-ranging and deep. With many retail shops closing for the lockdowns, orders in place along the supply chain have been delayed or cancelled. This is a problem common across apparel supply chains. In the short term, a large proportion of demand has been lost.

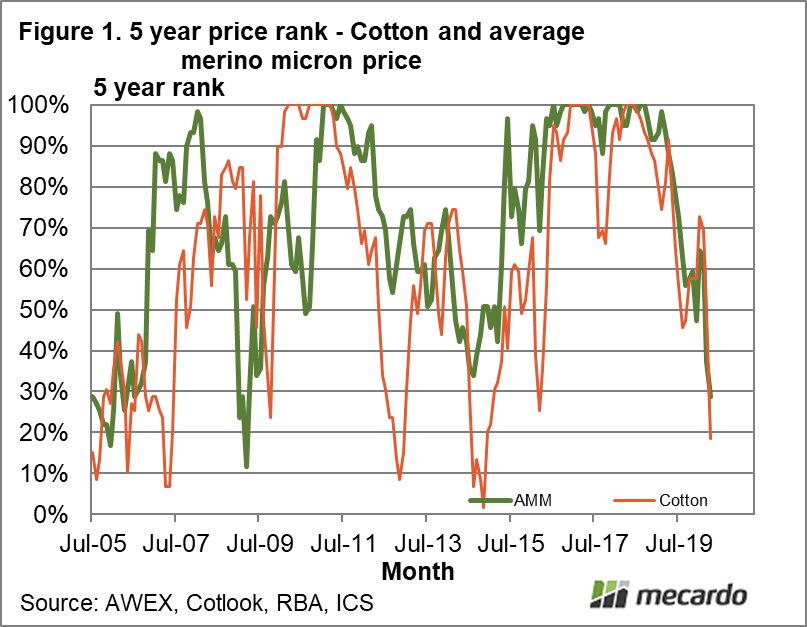

Figure 1 shows the rolling five year price rank for the average Merino micron (currently around 18.5 micron) and a cotton price series (the Cotlook A index is used here) from 2005 to early this month (April 2020). The rolling five year price rank provides an immediate view of the value of each fibre in relation to prices of the previous five years. Note how both cotton and the Merino price have plunged in the past month.

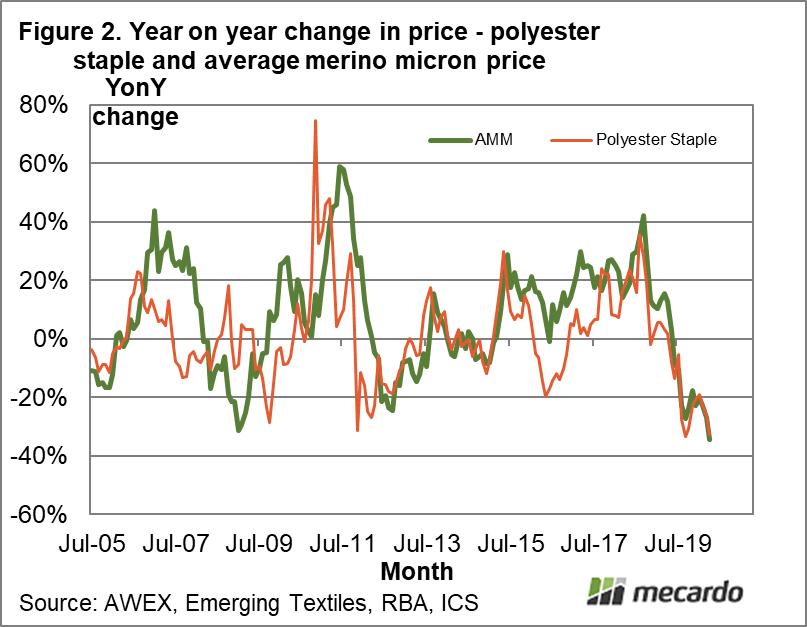

Figure 2 looks at the year on year change in price for the average Merino micron price and a polyester staple price series from 2005 onwards. The underlying prices series are in Australian dollar terms. Since mid-2018 the Merino price has trended lower in a very similar fashion to the polyester staple price. The last leg down has been due to COVID-19 and the economic ramifications of lockdowns.

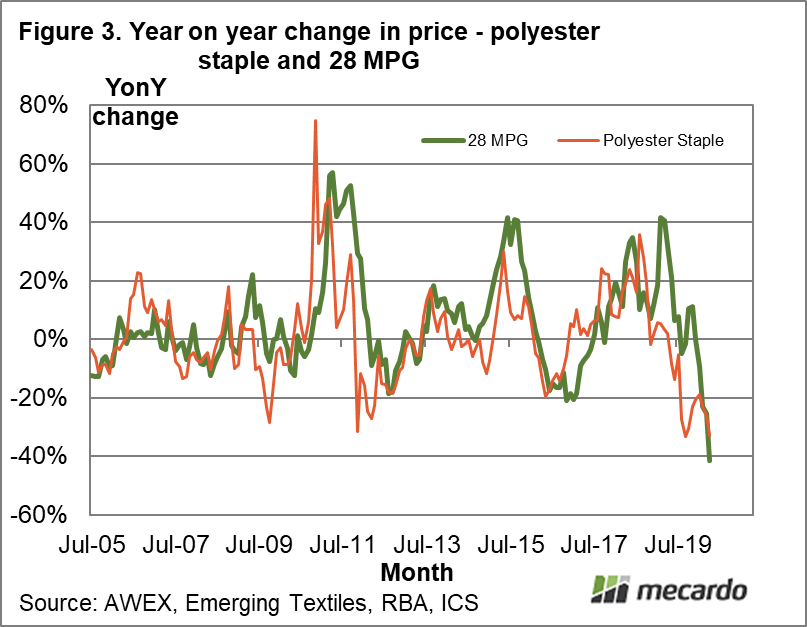

Finally, Figure 3 compares the year on year change in the 28 MPG and a polyester staple price series from 2005. The 28 MPG started its downward trend after the polyester series but has now raced the manmade fibre price down to be 40% below year earlier levels.

Wool prices usually follow the general trends and cycles seen in the greater apparel fibre markets, as they respond to common stimuli. In this case, lockdowns due to COVID-19 have reduced retail sales of apparel and this reduced demand has fed back upstream in the various supply chains to the raw material markets, be it Merino wool, crossbred wool, cotton or manmade fibres. The drop in price has become clear and the effect is widespread across fibres. What is not clear, is the likely duration of the weak demand.

What does it mean?

Wool prices (Merino and crossbred) have been following the same pattern as cotton and polyester staple fibre prices in the past month. Reduced retail demand has resulted in uncertainty along supply chains with lower prices for raw materials as a result. At this stage, the timing of a recovery is most uncertain as it will depend on an easing of lockdown conditions and subsequent recovery in economic activity.

Have any questions or comments?

Key Points

- The drop in Merino and crossbred prices has been matched by drops in cotton and polyester staple prices.

- The apparel fibres are reacting to a common stimulus – the reduction in retails demand due to COVID-19 driven lockdowns.

- What is most unclear at present is the length of time demand will be adversely affected by the lockdowns and the associated economic weakness.

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: AWEX, Cotlook, Emerging Textiles, RBA, ICS