The greasy wool market covers a wide range of constituent wool markets ranging from the rarefied 12 micron wool, which is rarely seen at auction, through to the big 38-39 micron carpet categories of New Zealand. In the current market fine merino wool is outperforming its “wool cousins”. This article takes a look at fine merino premiums.

While apparel fibre prices tend to follow similar cycles and trends, for various reasons various apparel fibres at times out perform or underperform the general movement of apparel fibre prices. The under performer this season has been crossbred wool. In contrast the out performer apparel fibre this season has been cotton (view apparel fibres article) with the average merino micron (currently around 19 micron) price falling back in relation to the cotton price.

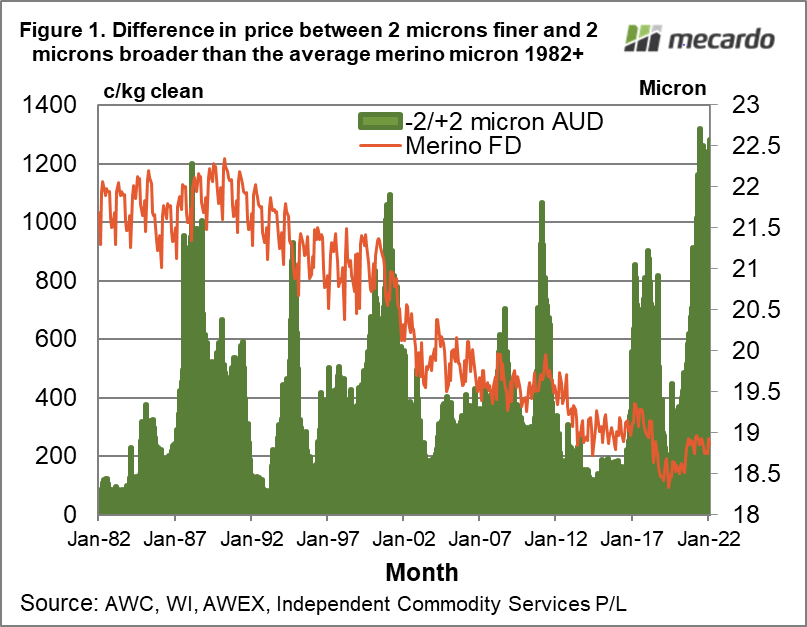

Fine merino wool however is trading at high premiums to medium/broad merino prices. Figure 1 shows the difference in price (effectively a premium) between categories 2 microns finer and 2 microns broader than the average merino fibre diameter from 1982 to last week, in cents per clean kg. In addition the average merino fibre diameter is overlaid, to show how much the quality of the Australian wool clip has changed during the past four decades.

The average merino fibre diameter was 21.5-22 micron during the 1980s, after which it trended lower to around 2013 before stabilising around 19 micron. This means the difference in price shown in Figure 1 refers to different micron categories depending on the average fibre diameter of the time. While this is not a perfect method it helps avoid the effect of changing supply on price. For example in the late 1980s 17 micron (which is currently some 2 microns finer than the average merino fibre diameter) was at least 4 microns finer than the average merino micron (equivalent to 15 micron now).

The current premium for 17 versus 21 micron is around 1300 cents, and has been in the 1150-1320 cents range since mid-2021 (seven months). This is a high premium by historical standards. In 1987-88, 2000-01 and 2017-18 the premium remained at high levels for roughly a year, so the current premium cycle, while high, is not yet “old”. Come mid-2022 the cycle will be a year old, with history pointing to the likelihood of lower premiums.

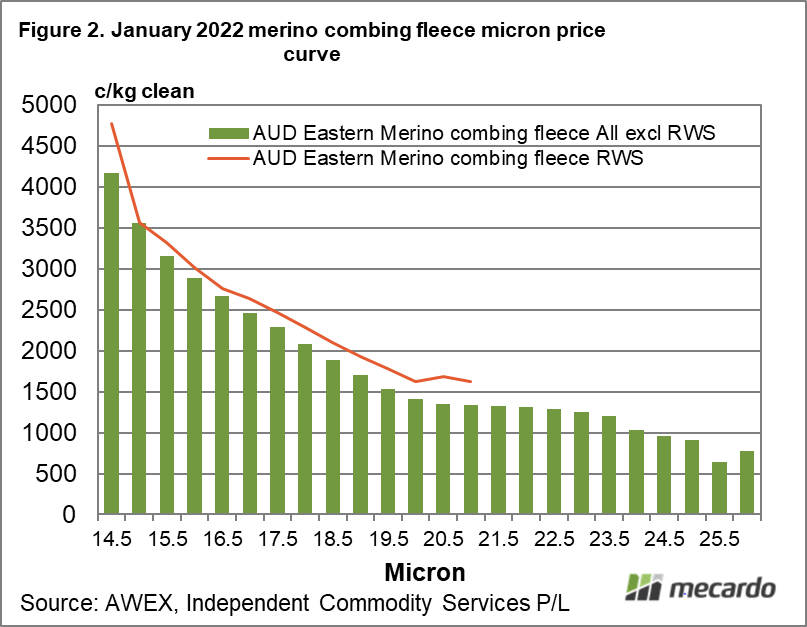

Figure 2 shows the price curve for average merino combing prices by micron for January, split into non-RWS and RWS accredited lots. These two series are separated as RWS prices are significantly higher than non-RWS prices, on average. In Figure 2 the prices for 20.5 through 23 micron are relatively flat, with only 93 cents difference across 2.5 microns. Below 20.5 micron the prices rises steeply, reflecting the high premiums shown in Figure 1. As well prices fall away when the micron becomes broader than 23-23.5 micron.

What does it mean?

Fine merino premiums remain at high levels by historical standards. The question is how long will they remain at these levels. History suggests that after mid-2022 the current cycle of high fine micron premiums will be getting “old” with the implication of the risk of lower premiums.

Have any questions or comments?

Key Points

- Fine merino premiums (as measured by 2 microns either side of the average merino micron – currently 17 versus 21 micron) are close to record levels.

- The premiums have been high since mid-2021. By mid-2022 the cycle will start to be old by historical standards.

- Premiums for merino fleece begin in earnest around 20.5 micron.

- On the broader side the gap between 20.5 and 22 micron is around its long term median but becomes much wider for 22.5 micron and broader.

Click on figure to expand

Click on figure to expand

Data sources:

AWC, WI, AWEX, ICS