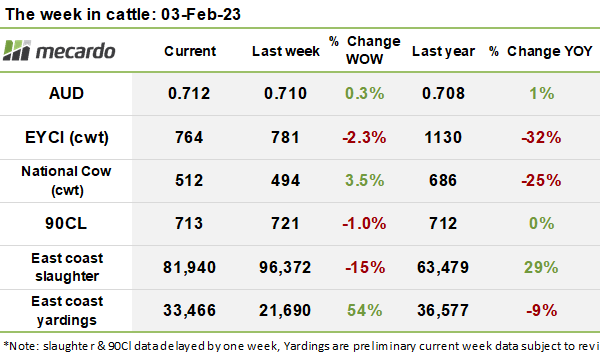

The Eastern Young Cattle Indicator (EYCI) may have fallen slightly this week; but after several weeks of downward momentum, signs of support for finished cattle are emerging from the shadows.

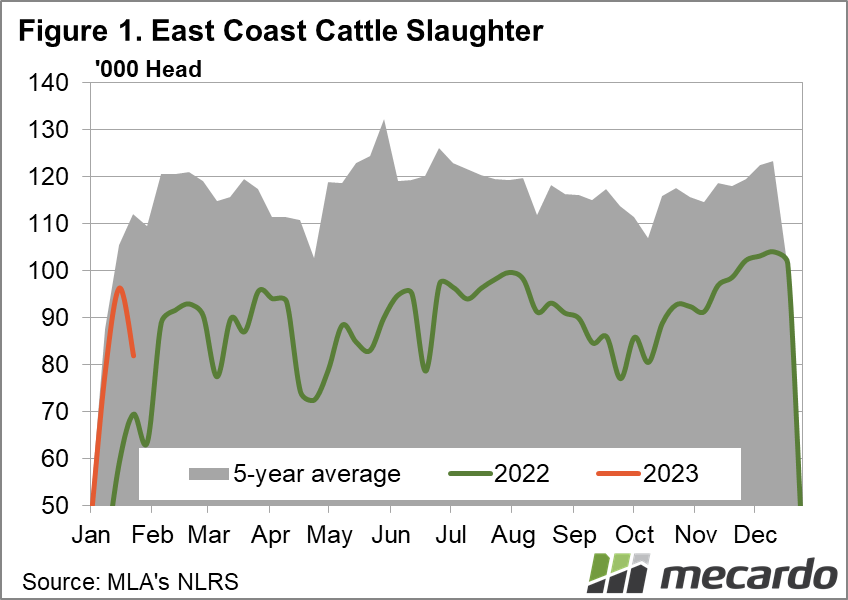

Slaughter is down, so, demand must be down? Not necessarily, a solid clip of meatworkers were having a well-earned BBQ and a beer at home. Last week’s slaughter statistics indicated that processors had to slow up over the Australia day public holiday week with 14 000 (15%) fewer head being processed compared to the prior week. Nothing to worry about though, as this shows up like clockwork this time of the year.

There is still a promising story hidden in the kill rate for this week; 82 000 head is about 29% above where we were last year. Looking at figure 1, for every week this year, we have been averaging 60% above last year’s volumes, so it could be said that processors are on a roll. Word is that the labour problems have abated somewhat (particularly in QLD), but it will be another six months or more until the new hires are fully trained and productive.

The Eastern States young cattle Indicator (EYCI) backpedalled this week, dropping 18¢ (2%) to close at 764¢/kg cwt. Part of the pain can be traced back to stronger supply, with 11,797 head of cattle contributing to the index this week, 15% above last week.

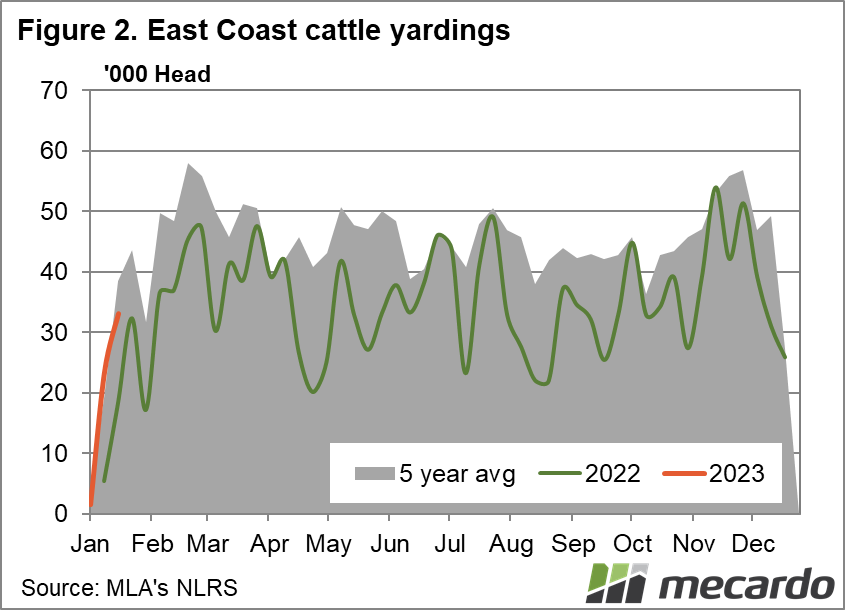

Restocker numbers were on par with last week, however, feeder cattle supply ticked up 3%. Overall, total yardings for this week pushed up 54% to 34,466 head, and the demand for young cattle just wasn’t sufficient to soak up the increase in supply. As usual, Roma, Dubbo, and Dalby were dominant influencers on the index, with steers fetching average prices of 813¢/kg cwt, 804¢/kg cwt, and 766¢/kg cwt respectively. Yearling heifer prices trading at a 10-16% discount to steers at key saleyards are currently a source of weight on the EYCI.

Market reports out of Roma suggest that a crowd of restockers has been attending, but the confidence that drives spirited bidding hasn’t emerged just yet, suggesting buyers are biding their time.

Last week’s AuctionsPlus results suggest that while pass-in rates remain around 43% on the platform, the epicentre of buying activity for weaners and yearlings is located around Wagga. There was also some activity happening in northern NSW and southern QLD. The key observation though is that cattle purchases seem to be geared towards local listings, with buyers having little appetite to transport cattle long distances.

Some northern producers have good grass behind them and are holding off marketing feeders, pushing weights toward the upper end of specifications. Feedlots are starting to respond by adjusting their intake parameters and shifting towards stronger penalties for producers delivering overweight cattle.

The main source of extra supply emanated out of NSW this week, where yardings jumped 72% week on week to reach 13,578 head. Victorian producers were less keen to market cattle, with numbers dropping 2% week on week.

The Western Young cattle indicator (WYCI) pushed up 39¢ (5%) to close at 831¢/kg cwt. Steers traded up 48¢ (7%) at 797¢/kg cwt.

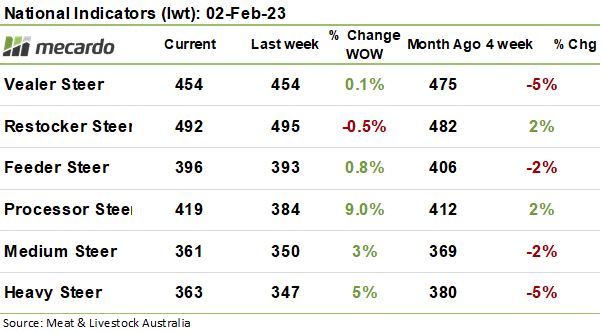

The national indicator board was lit with a healthy green glow. Of note was heavy steer prices lifting 16¢ (5%) to close at 363¢/kg lwt, while medium steers, cows, and feeder indexes all finished firmer.

The US frozen cow 90CL price suffered from the rising Australian dollar, falling back 8¢ (1%), despite actually lifting slightly in US dollar terms over the course of last week.

Concerns in the United States of a sharp fall in cow slaughter in Q2 may have positive consequences for Australian exporters. This is due to potential competition between the Chinese and the United States for imports and other exporters such as New Zealand not seen as sure bets for supply.

The week ahead….

The expected ramp-up in the supply of cattle in the coming month remains an area of concern. However, reports of a solid contingent of restockers attending saleyards in the north suggest that there may be some pent-up demand lurking. Particularly as many areas in the top end still have the benefit of solid pastoral conditions behind them. Pockets of excessive rainfall in some regions are likely to remain an issue, discouraging cattle movements, and dampening marketing intentions. The outlook in the US is also likely to provide solid support to cow prices going forward, in the absence of any huge jump in the value of the Aussie dollar.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: MLA, Steiner, Argus, Mecardo,