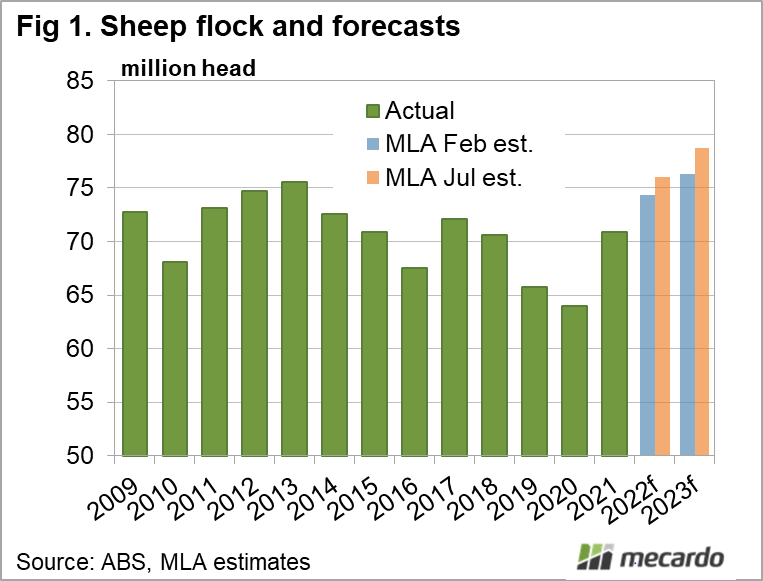

All sheep industry data is on the increase, with the flock size and subsequent slaughter, production and export volumes growing at a faster than first expected rate this year. Australia’s sheep flock reached 100 year lows in 2020, but favourable seasonal conditions and historically high markets have since turned that around. Meat & Livestock Australia’s July sheep industry projection update forecasts the flock to climb to 76 million head as of 30 June 2022, an extra 2% more than its February outlook. (figure 1) And the flock is far from the only figure revised higher, as supply and demand kicks up.

If the flock forecast comes to fruition, it will be a 15% rise year-on-year and MLA predicts the growth will continue in 2023, with sheep numbers expected to be another 3.5% higher at more than 78 million head. Good lamb drops in both 2021 and 2022 are a major contributing factor to this, not just ewe retention, as sheep slaughter hasn’t plummeted and lamb processing is up.

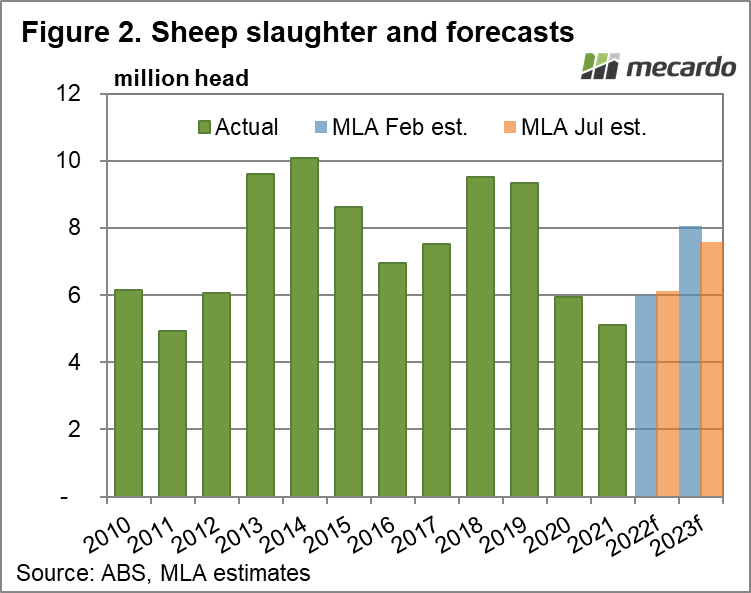

Sheep slaughter is now forecast to be 20% higher in 2022 than it was in 2021, making up the 14% it lost the previous year (2020) and then some. It is then expected to follow the flock higher again in 2023, climbing another 24% to 7.58 million head. (figure 2) Lamb slaughter has been revised 400,000 head higher for 2022 since February, which if accurate will be its highest figure since 2018. (figure 3)

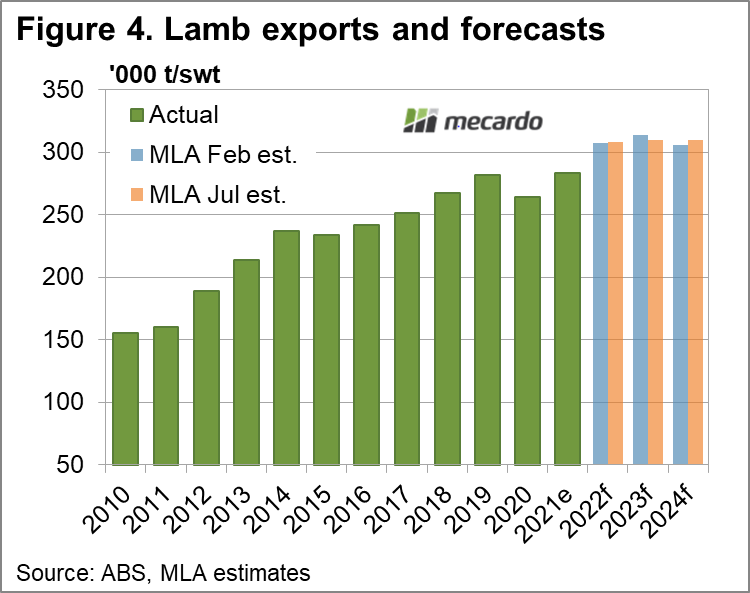

Australian lamb exports are 5% higher year-on-year for the first five months of 2022, and the latest industry projections have raised this year’s total export volume forecast to be 8% higher at 308,000 tonnes shipped weight. This would be on top of the 7% climb between 2020 and 2021, and push lamb exports into record territory, with expectations of further growth into 2023 (310,000 tonnes). (figure 4)

China kept its top spot as our main sheepmeat market by volume, despite having taken less year-on-year from January-May, and swinging their intake away from lamb and towards the lower price point mutton. Mutton exports are forecast to be on-par with 2021 this year, before climbing 18% in 2023. Expectations of live export have dropped significantly with numbers 25% lower year-on-year for January-May, and MLA now forecasting the 2022 total to be 20% lower than it predicted in February.

What does it mean?

The rapid flock growth being experienced means plenty of extra lambs in the system, and comes on top of the processing sector working through a backlog caused by labour shortages and supply chain issues. Producers are already experiencing the repercussions of this as lamb prices have failed to head higher in the mid-winter, a time when lamb supply is traditionally short and returns are at some of their strongest for the year.

However export demand continues to underpin the market as volumes look to hit records, currently supported by a weak Australian dollar making our pricing more competitive. With the exception of live export, the forecast figures all look positive as the flock flourishes from strong seasons, stable markets and positive sentiment.

Have any questions or comments?

Key Points

- Faster flock growth forecast, with sheep numbers to hit 76 million head this year.

- International demand for both lamb and mutton pushes sheepmeat exports into record territory, as live exports plummet.

- Backlog of last year’s lambs still to come through the system will limit traditional winter price hike.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: MLA, ABS, Mecardo