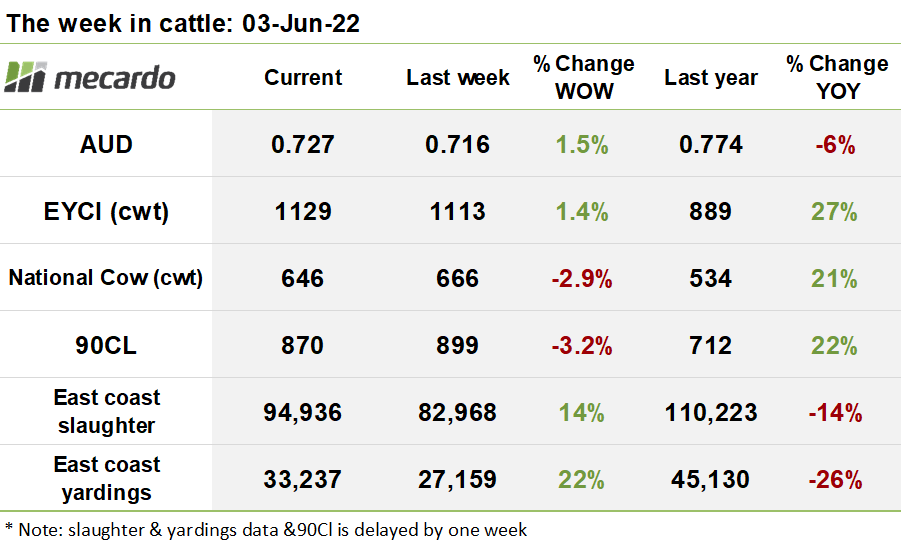

Demand is still outstripping supply for young cattle, and despite increases in yardings recently, price has continued to rise. The same cannot be said for finished cattle though, with medium and heavy cattle prices taking a beating, and cows coming back down to earth in line with a persistently subdued 90CL price environment that may not turn around for some months.

We have finally started seeing some of the typical acceleration in slaughter that occurs in May, albeit coming off a much lower base than usual – east coast slaughter jumped 14% for the week ending 27th May to 94,936 head, with QLD volumes lifting 10K(27%) head, helped along by a 5% increase in VIC volumes.

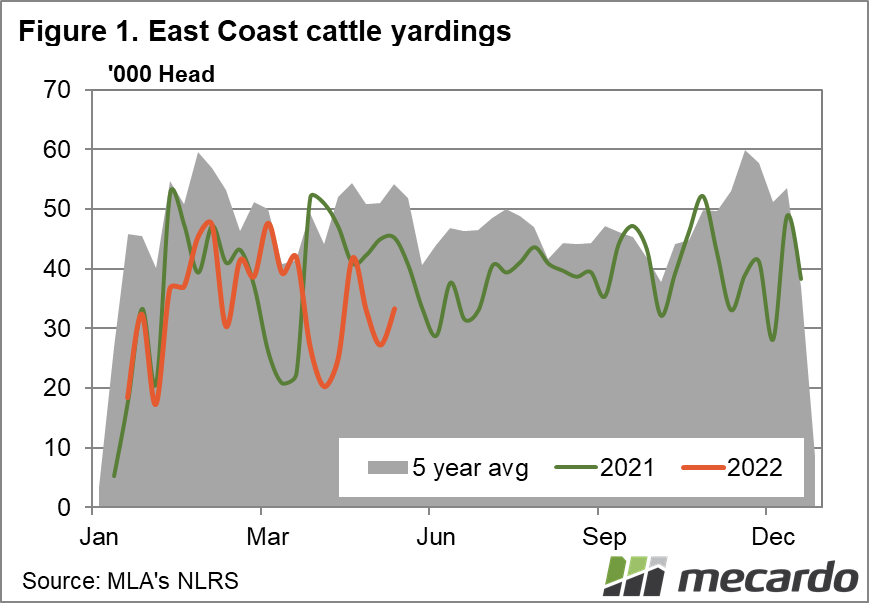

As expected, east coast yardings for the week ending the 27th May 2022 increased 22% week on week to 33,237 head, driven primarily by a huge return to the yards in QLD, where offerings increased 84% week on week, with NSW following the trend, booking a 40% week on week surge also.

This situation this week looks to be one of another period of increased supply, with EYCI eligible yarding’s increasing 22% week on week to 12,129 head.

Similar to last week, despite the significant increase in supply, the EYCI exhibited further evidence of red hot underlying demand, rising another 15¢(2%) to 1,129¢/kg cwt. Keep in mind though, that despite demand easily outstripping supply at the moment, pushing prices higher, supply to the saleyards is still 26% below 2021’s levels. Further increases in supply to more normal levels could easily turn the pricing situation around.

Over in the west, the WYCI advanced 19¢(2%) to finish the week at 1091¢/kg, with price benefiting from a 36% contraction in in supply, with yardings at 488 head, and the vealer proportion of the index increasing 12% to 92% compared to the prior week.

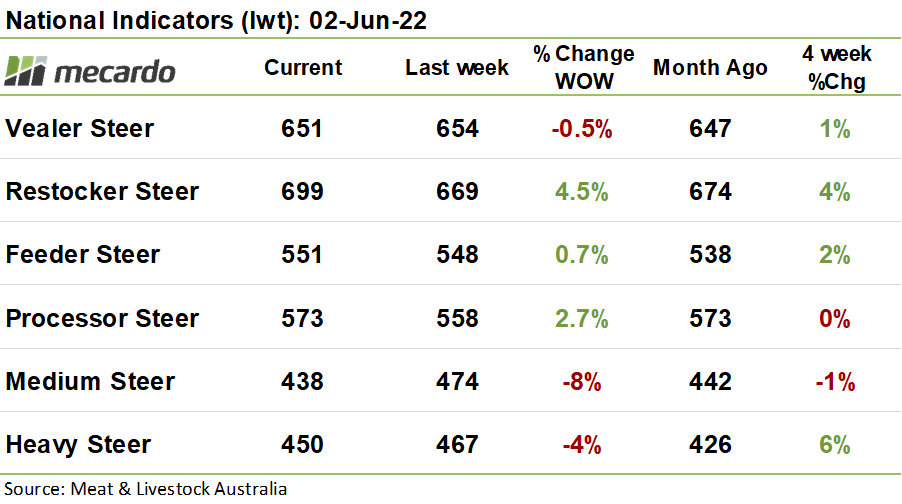

The national cattle indicators presented as quite a mixed bag of results this week. In line with the strong demand for young cattle at the moment, restocker steer prices jumped 30¢(5%) to 699¢/kg lwt, while the wooden spoon was awarded to medium steers, which plummeted 36¢(8%) week on week to settle at 438¢/kg lwt. Heavy cattle and cow prices also fell 4% and 3% respectively.

The US frozen cow 90CL price shed another 5¢(2%) to settle at 280¢US/lb, and lost 29¢(3%) in Aussie dollar terms, closing the week at 870¢/kg swt, with yet another strengthening in the aussie dollar in the week prior exacerbating the fall in price . The sizable fall in 90CL in US terms we have just seen is reflective of the continuing soft demand situation for near term delivered manufacturing beef in the US, with sellers of imported product finally relenting and accepting the lower bids being thrown by the market. Competition from NZ product is also helping the market lower, as NZ slaughter is running at annual highs presently.

On the brighter side though, Steiner comments that US cattle liquidation is running at the highest level seen in 30 years. This may pan out to be a case of destocking activity in 2022 being front loaded, leading to a solid reduction in slaughter rates and supply in the back end of the year, which will be positive for prices, and Australian producers. However, another season of dry conditions in the US caused by a 3rd year of La Niña could keep the slaughter pace up, causing pain in the medium term, but lending substantial support to price in 2023 if US conditions turn around, triggering a herd rebuild.

The week ahead….

Slaughter volumes are showing signs of recovery, and further increases over June would fit well with patterns seen last year, lending support to prices for finished cattle. There are indications that the current level of demand for young cattle is quite strong, and likely to continue, so conditions are looking positive for another week of firm prices coming up.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: MLA, Mecardo.