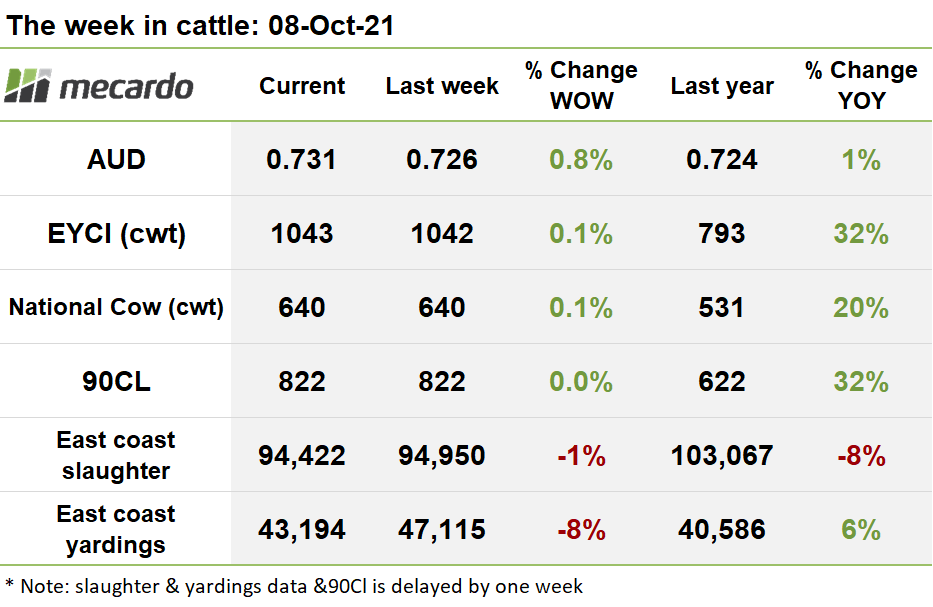

The Eastern Young Cattle Indicator (EYCI) reached a new all-time high this week before running out of steam and falling back to just above where it started, while the market for heavy cattle consolidated, giving back some of the incredible gains last week.

While headline slaughter numbers only dipped 1% last week, there were swings and roundabouts going on in the distribution of the total throughput, with QLD numbers crashing 12%, offset by an 11% lift in NSW, and a 24% increment in VIC.

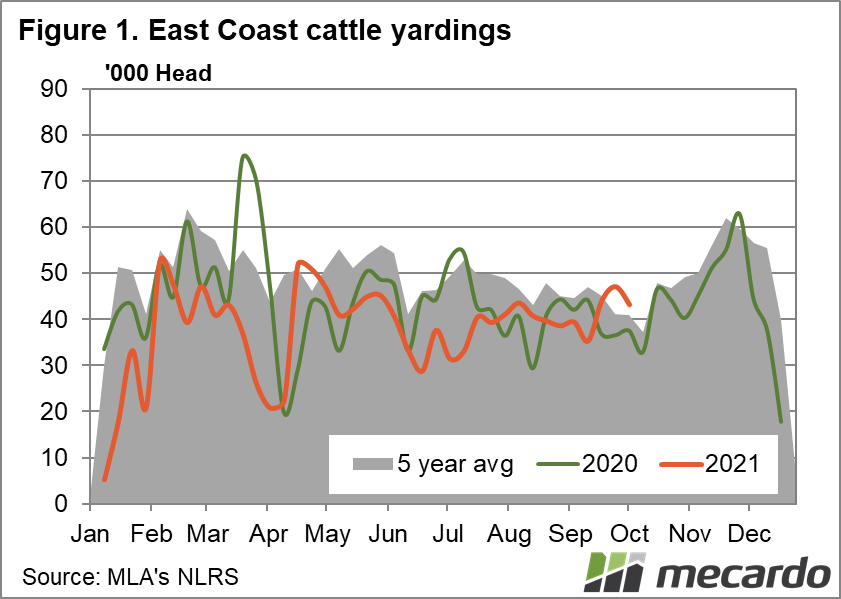

Yardings dropped 8% last week, indicating tightening supply. All states held back cattle, lead by NSW where offerings reduced 16% week-on-week, followed by the big cattle state of QLD, where numbers slipped 5%. Yardings in QLD are still currently 66% above the 5-year average, and 21% above levels seen at the same time last year.

The EYCI continued to show upward momentum, reaching a new record of 1,057¢/k cwt on Wednesday before falling back to close up 1¢ (<1%) from the prior week at 1,043¢/kg cwt. Eligible cattle yardings crashed 31% this week, with supply tightening to 8,492 head.

Roma prices lifted 43¢ (4%) to 1,045¢/kg cwt, on a 29% fall in yardings, while Dalby prices increased 12¢(1%) to 1,035¢/kg cwt. Dubbo went the other way though, with yardings increasing 57% week on week to 1,282 eligible cattle, and average prices fell 64¢(6%) to 1,052¢/kg cwt.

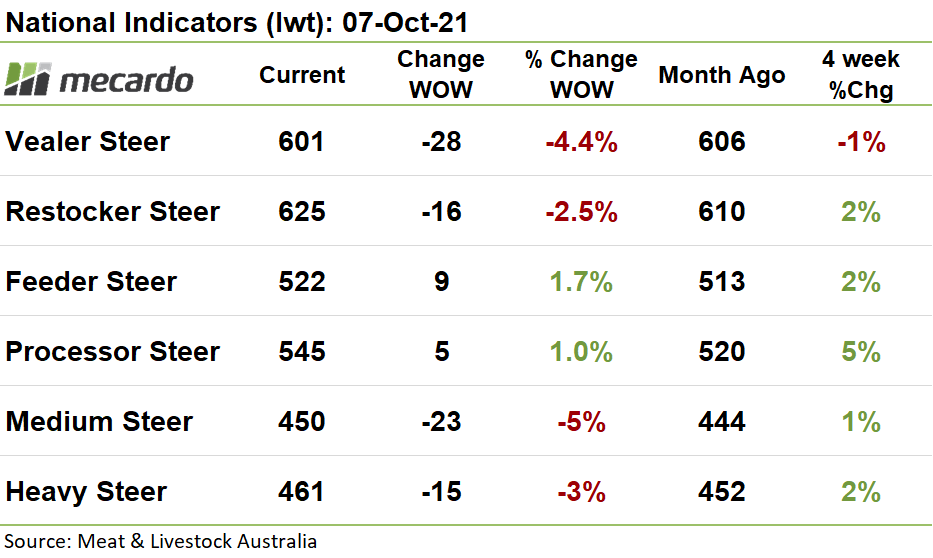

While Vealers, Restockers and Heavy cattle fell back slightly after their meteoric rise last week, Feeder and Processor Steer prices both went higher. After such a big jump last week, heavy cattle coming back to earth as expected was not a huge surprise.

90CL frozen cow prices remained static last week, at 822¢/kg swt, with exchange rates making little impact, as US prices also remained stagnant at 270¢/lb.

Steiner reports that the imported beef trade in the US has taken a leisurely tone recently, with NZ supplies of beef into the US expected to increase over the next couple months, and the opening up of Argentinian exports again forecast to have little impact due to quotas that are in place for the US market.

The Aussie dollar staged a recovery this week, lifting 0.8% against the US greenback to 0.731US, buoyed by improved commodity prices, and risk-on sentiment in equities.

The week ahead….

Overall, the indications are that we are heading for tighter supply again next week, as lower numbers of eligible cattle on the EYCI this week indicate the usual early October downtrend in offerings seems to be taking place. With tighter supply, comes support for prices, so prices holding or grinding higher again next week wouldn’t be a surprise, particularly since a good dose of rain expected in the week ahead though southern QLD and most of eastern NSW will be positive for producer confidence.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: MLA, Stiener, Mecardo