We normally think of managed funds as the “smart money”, but sometimes they do get it wrong. Last week was a prime example. The funds were caught out with sizable short positions on wheat, as the market surged higher on the outbreak of war in Ukraine.

For the last couple of months, managed funds were betting that wheat supply would be plentiful, and the threat of war would fizzle out. They expected to take a profit when Putin sent his troops home from the Ukrainian border, and the war-related risk premium which had infected wheat markets evaporated.

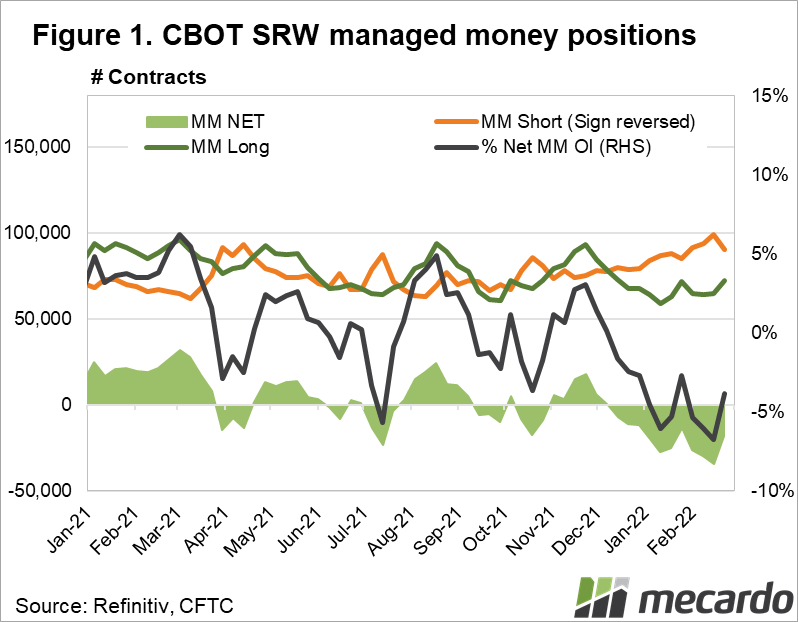

In late November, the funds long positions in CBOT SRW wheat reached a peak of 94K contracts, with their aggregated net long position reaching 3.1% of open interest (Figure 1). From that point onwards, long positions were rapidly closed out until reaching a low of 59K contracts in mid January. In contrast, short positions were steadily being accumulated from 74K contracts, up to a peak of 99K contracts in mid February.

The rationale behind the bearish trade were concerns about global growth and wheat demand that could arise from the spread of the Omicron variant of COVID-19, and expectations of large Australian and Russian wheat crops bolstering global stocks. Late November 2021 also saw the first significant reports of Russian armed forces amassing along the Ukrainian border.

As early as the 11th of February news emerged of supposedly credible intelligence received by the US that Putin would attack Ukraine before the end of the Beijing Olympics. This was a factor that caused the tide of opinion to begin to turn, and the funds began to buy long contracts, and close out short positions.

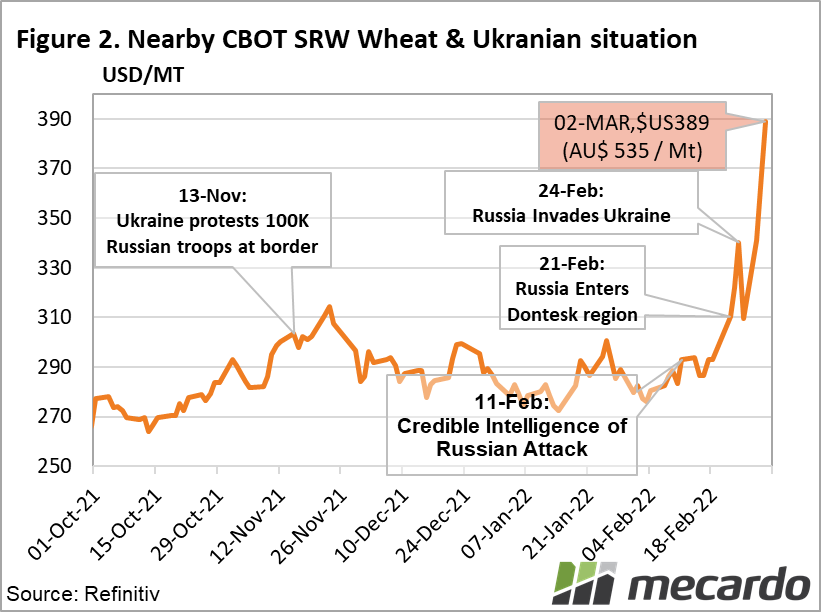

Nearby SRW wheat futures surged in response to Putin announcing “peacekeeping” troops would enter the rebel-held Dontesk region of Ukraine on the 21st, and skyrocketed when the full-scale invasion occured on the 24th of February (Figure 2).

The next CFTC commitments of traders report is scheduled for releases on the 4th March, and considering that there is the distinct possibility that Ukrainian wheat production may be disrupted potentially even into the 2022/23 season if the violence becomes protracted, the expectation is that more short positions will be liquidated.

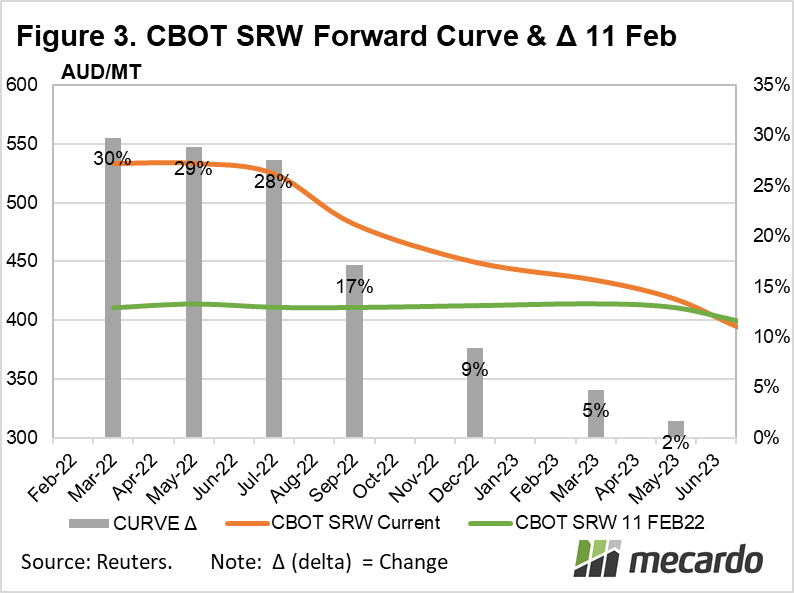

The additional buying activity from managed funds hastily backtracking out of short positions as the market rises, will add to the upward pressure on futures prices in the short term until the funds have extricated themselves from their exposure. Nearby CBOT wheat has added $US 47/mt (14%) in the last few days alone, currently trading at $US 389 /Mt ($AU 535/ mt), and the futures market has rallied some 30% in AUD terms since the 11th February 2022 (figure 3). As such, it is safe to say that many speculators caught short have lost their shirts to Putin recently.

What does it mean?

When funds are caught on the wrong side of the market, they will tend to back out of their positions- and evidence that this process has begun emerged last week. Purchases of long positions by funds to close out what turned out to be ill-conceived short positions accumulated since last year will continue to provide support to the US wheat markets in the short term.

Have any questions or comments?

Key Points

- Managed funds held short wheat positions before war broke out

- Funds are now closing out short positions in wheat

- Long position purchases in the short term by funds will add more heat to the market.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: Refinitiv, CFTC, CBOT, Mecardo