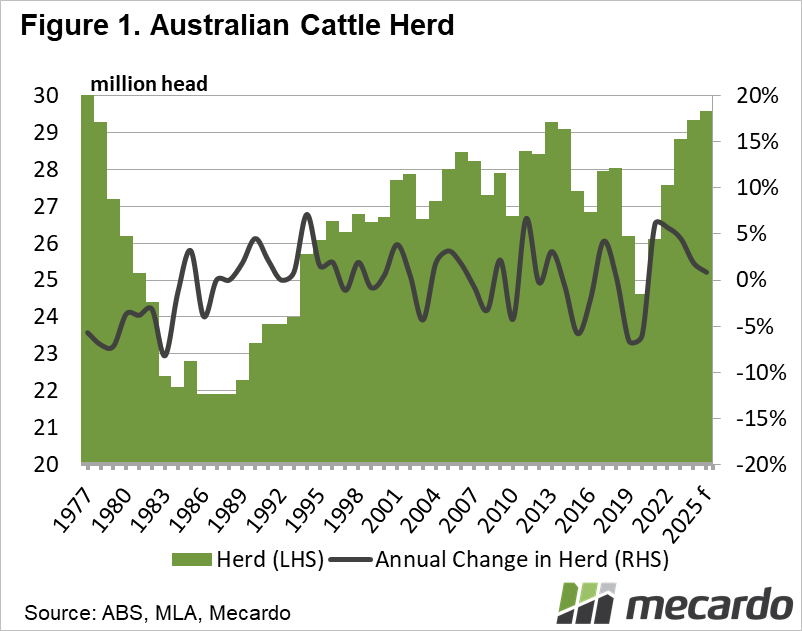

It has been six months since Meat and Livestock Australia (MLA) released cattle industry projections. What has moved since then - as expected - are cattle numbers, which grew by 6% year-on-year in 2022, to just over 27.5 million head, and are forecast to continue to rise this year. This moves the industry past the rebuild phase and into growth territory, mainly due to favourable seasonal conditions and strong prices creating positive sentiment.

Cattle numbers as of June 30 for this year are forecast to be at 28.8 million head, up 4.5% on 2022 figures, with growth continuing – albeit much slower, out to 2025 when they will peak at 29.5 million head. This is set to be the largest herd since 1977 – almost 50 years. Slaughter will therefore also be on the up, projected to lift to about 8 million head by 2025 – a jump of 30%. This will see beef exports follow suit, to back above 1 million tonnes shipped weight in 2023 for the first time since 2020.

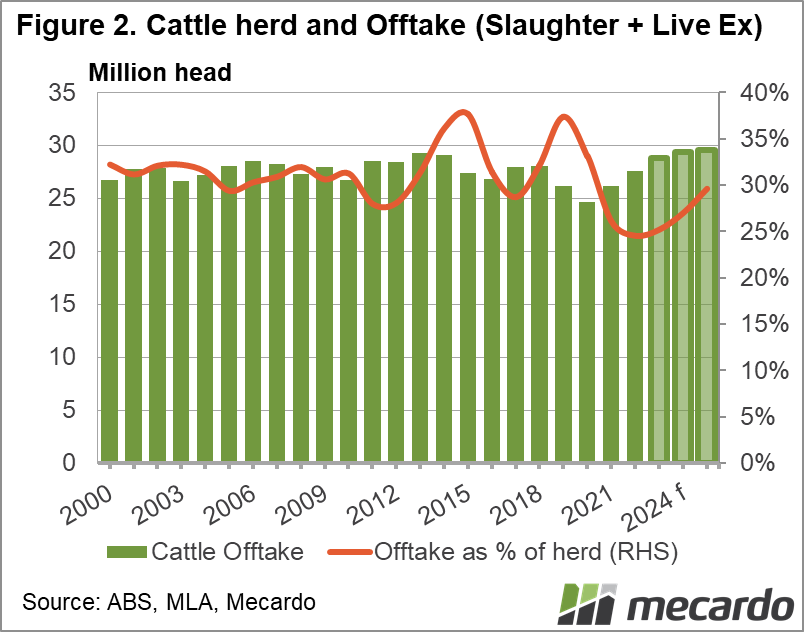

We often look at the female slaughter ratio (FSR) here at Mecardo as a good insight into herd rebuild and retention, and MLA is now also reporting on the stock turn-off ratio (STR). The STR – a measure of the number of cattle processed and exported compared to herd size – is reported to have reached its lowest point on record, 24% in 2022, with the long-term average STR sitting at 31%. Compare this with the rising herd number, and it can only mean one thing – increased supply.

Cattle slaughter forecasts come with a big “only-if” this time around, which makes for an interesting – and significant – variation in numbers. The official projection is for total cattle slaughter (including calves) to climb above 7 million head in 2023, from 6.47 million in 2022, which would be a rise of nearly 8%. The caveat however is the capacity of processors to increase throughput capacity by attracting increased labour. If they can’t – and there is little indication in the current environment that labour issues will resolve themselves wholly in the short term – then slaughter is more likely to remain firm on current figures, closer to 6 million head than 7 million.

MLA has widened the scope of their price outlook, including new indicators in their forecast to which Mecardo is a contributor. Their industry aggregate Eastern Young Cattle Indicator (the collated forecast from industry analysts) is 811c/kg as of June 30 this year, which is 26c/kg above where the EYCI ended last week. They also expect the National Feeder Steer Indicator to reach 419c/kg live weight, between now and the end of June; nearly 7% above where it is currently.

What does it mean?

High rainfall has spread even further across the country this summer, and while that brings its own set of challenges, it’s also continued to support retention and growth, and cattle supply in turn is on the up. We’ve already seen this put downward pressure on prices in recent months.

We haven’t looked at demand in this article, but the global desire for protein hasn’t dissipated and the US cattle turn-off is set to slow, which should support prices at roughly their current levels. The big question for the year is if Australia’s processing sector can turn the extra cattle into beef at the rate required, and how this will impact producers.

Have any questions or comments?

Key Points

- Cattle herd numbers are set to continue rising, overtaking the 10-year-average herd size this year and reaching its largest size in almost half a century by 2025.

- The stock turn-off ratio is 6% points below the long-term average in 2022, its lowest point on record.

- Slaughter figures are highly dependent on processing capacity in 2023.

Click on figure to expand

Click on figure to expand

Data sources: ABS, MLA, Mecardo