Harvest is either going or rapidly approaching in many cropping zones at the moment. With harvest comes selling, or at least much greater interest in prices. Harvest pressure is already appearing in markets, with prices beginning to ease.

Even during a relatively dry year harvest pressure can impact markets. In some cases, harvest pressure is stronger in dry years, as growers are reluctant to forward sell, given the uncertainty in production.

This year it is likely even worse, with geopolitical issues creating another layer of uncertainty, and producers not wanting to get caught having sold cheaply in a rising market.

There is always some impetus to sell off the header, with bills racked up during the growing season needing to be paid, but this year with livestock prices where they are, there might be additional need to generate cash for mixed farmers.

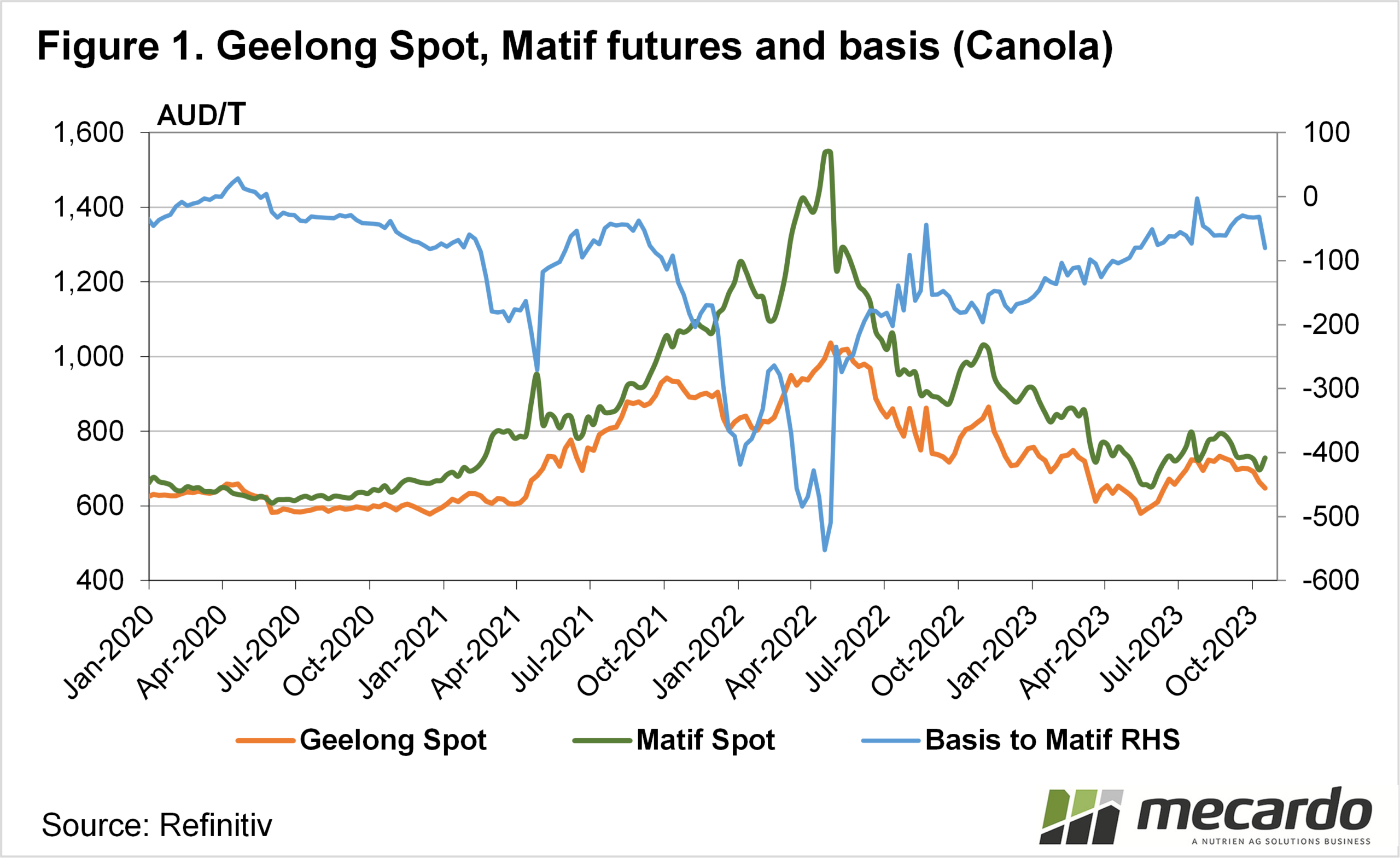

With harvest only just underway, we are already seeing some impact on price. Figure 1 shows canola prices at Geelong, on the MATIF exchange and the ‘basis’ or difference between the two. The last fortnight has seen MATIF prices bouncing around, but Geelong canola has fallen and stayed there.

Geelong canola basis to MATIF has rapidly gone from -$30 to -$80 over the last week, with grower interest in selling increasing, with prices below $600 port fairly recent in memories.

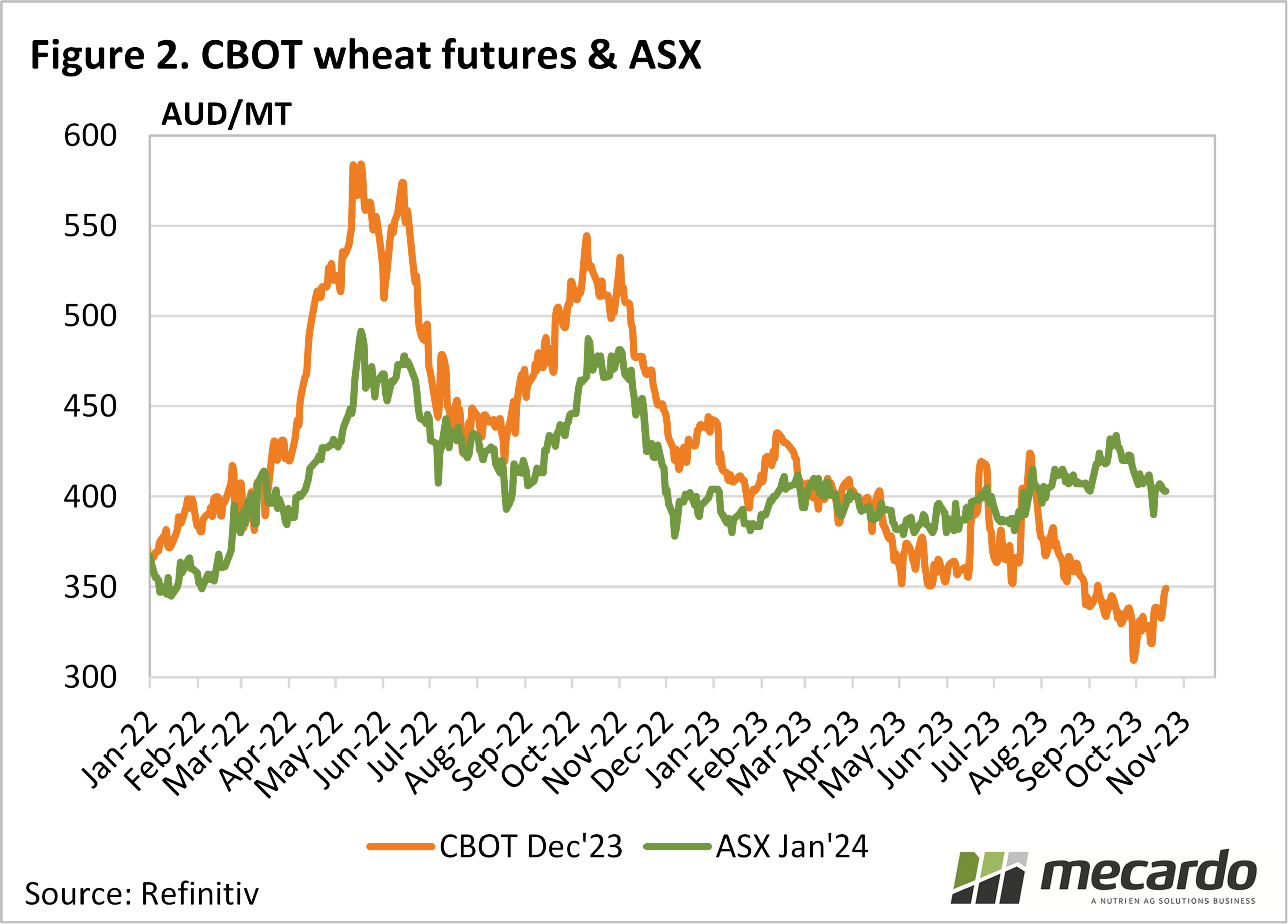

The story is similar in the wheat market. Figure 2 shows Chicago SRW and ASX Wheat Futures. ASX values have eased back towards $400/t, despite SRW staging a rally over the last fortnight. SRW has gained over 10% in our terms from the low, but ASX has shown none of that strength.

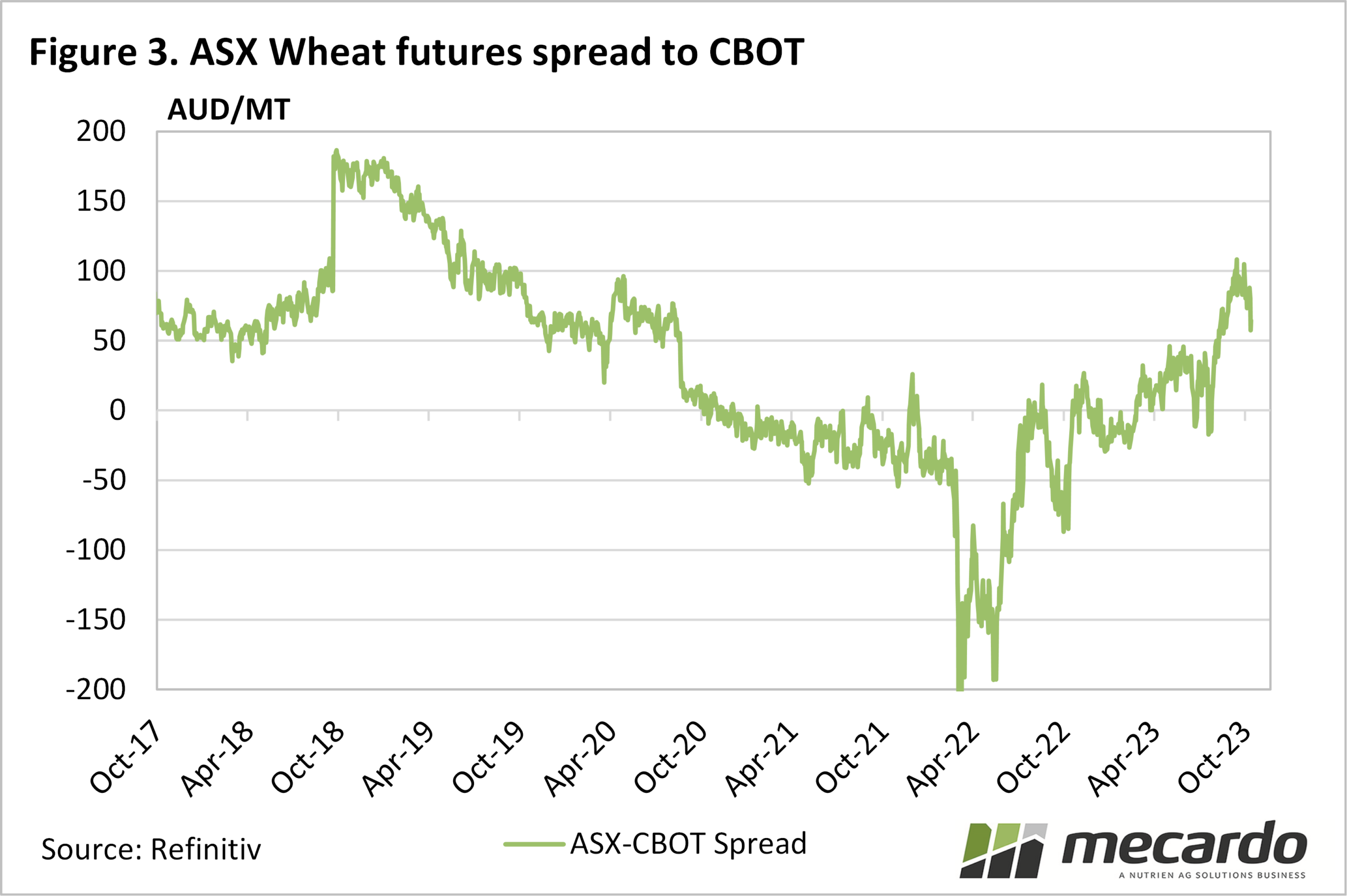

Figure 3 shows the impact on basis, losing $40, from over $100/t back to $60 as wheat supplies gain certainty and selling picks up. Growers will be looking at $400/t and think it looks pretty good in the current environment. It is still only $30 off the highest price seen since last November.

What does it mean?

We’re unlikely to see local prices rise relative to international values now, in the absence of a harvest-disrupting rain or a similar event. There is still room for basis to squeeze further, but both wheat and canola are likely to see some resistance to selling at $400 and $600 respectively.

Having said that it will be some time before basis has the chance to improve, with price increases reliant on international markets now.

Have any questions or comments?

Key Points

- Both wheat and canola prices have fallen relative to international values recently.

- With more certainty surrounding supply, selling appears to be picking up.

- There is little short-term basis upside, with higher prices reliant on international markets.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: MATIF,Refinitiv, CME, Mecardo