Normally the old adage is that the cure for high prices is high prices, and vice versa. The grain trade in the US was banking on the adage holding true, to see the current very good corn and soybean prices translate into stronger plantings. The United States Department of Agriculture (USDA) reckons it hasn’t moved corn.

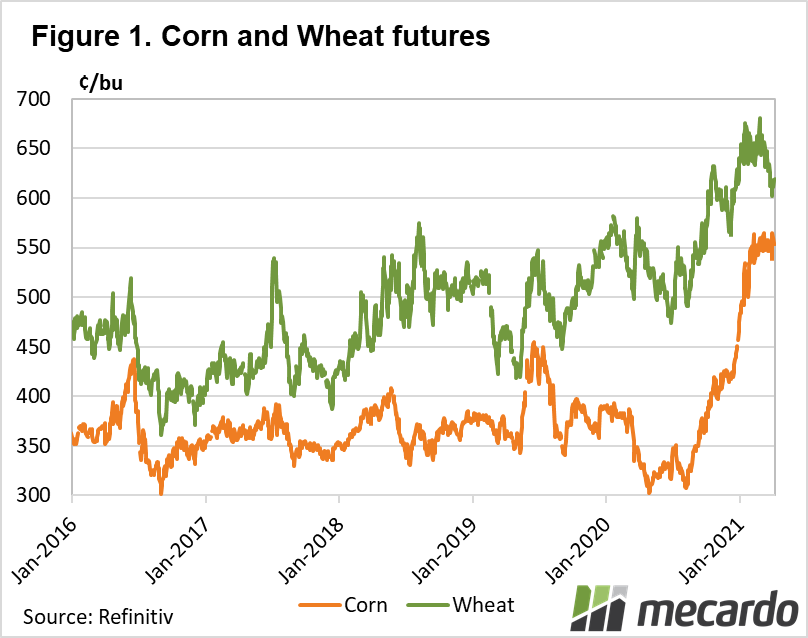

As reported in the weekly comments on Friday, the USDA last week released their acreage report for plantings of winter and summer crops. Corn and Soybean Futures are at very strong levels. Figure 1 shows the rally in corn, which started back in August, has seen prices at levels 62% higher than this time last year.

Compare this to wheat, which is higher than last year, but ‘just’ 19% stronger. We can see in figure 1 that the gap between wheat and corn has narrowed significantly over the last six months.

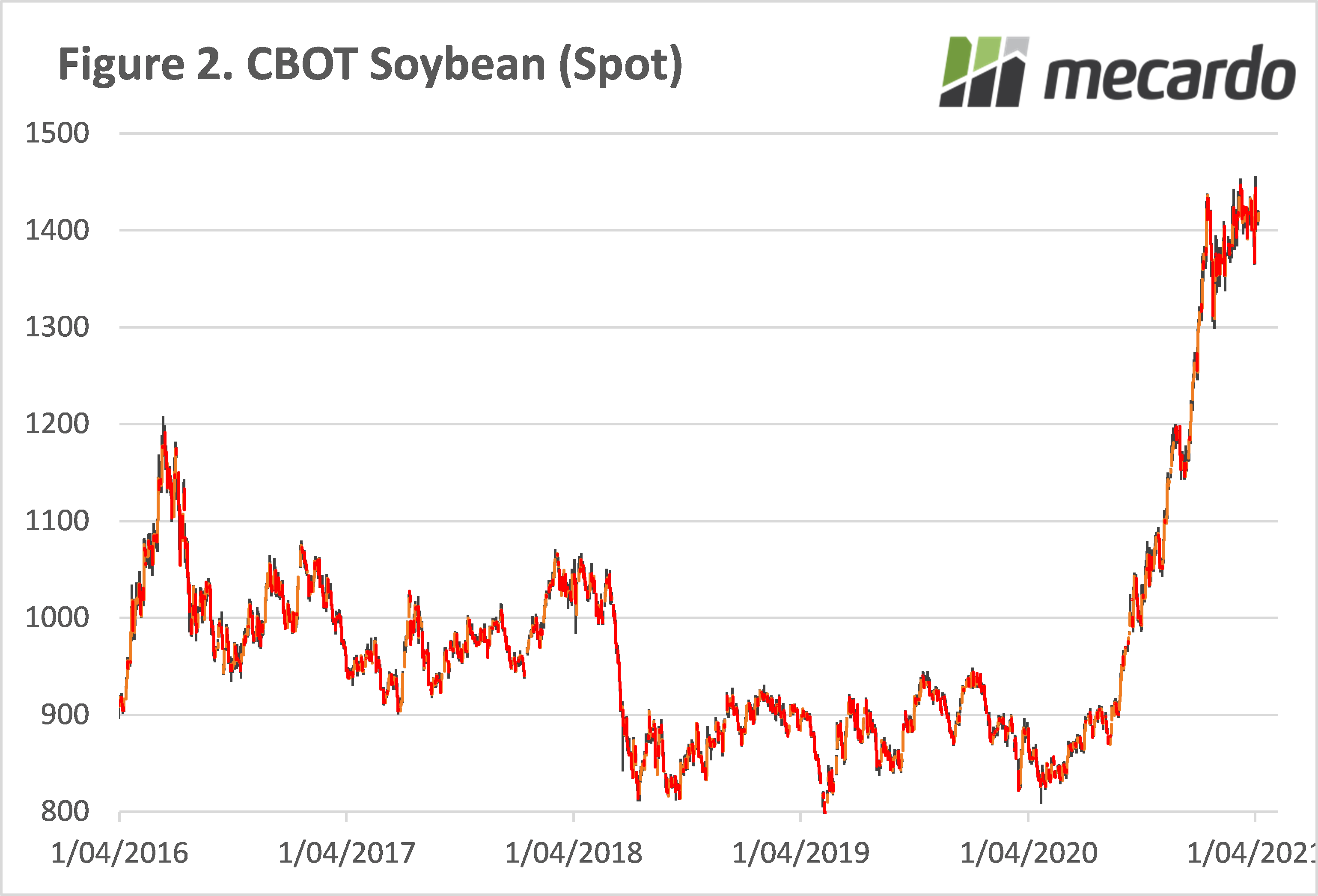

Soybean futures, shown in figure 2, have also seen a very strong rally, with prices sitting 59% above this time last year.

The price rallies in US corn and soybeans over the last 12 months have been partly due to weaker supply, with demand playing a strong part. The global corn stocks-to-use ratio has fallen for five years in a row, while soybeans stocks-to-use has fallen heavily in the last two years, and helped push both soybean and corn prices higher.

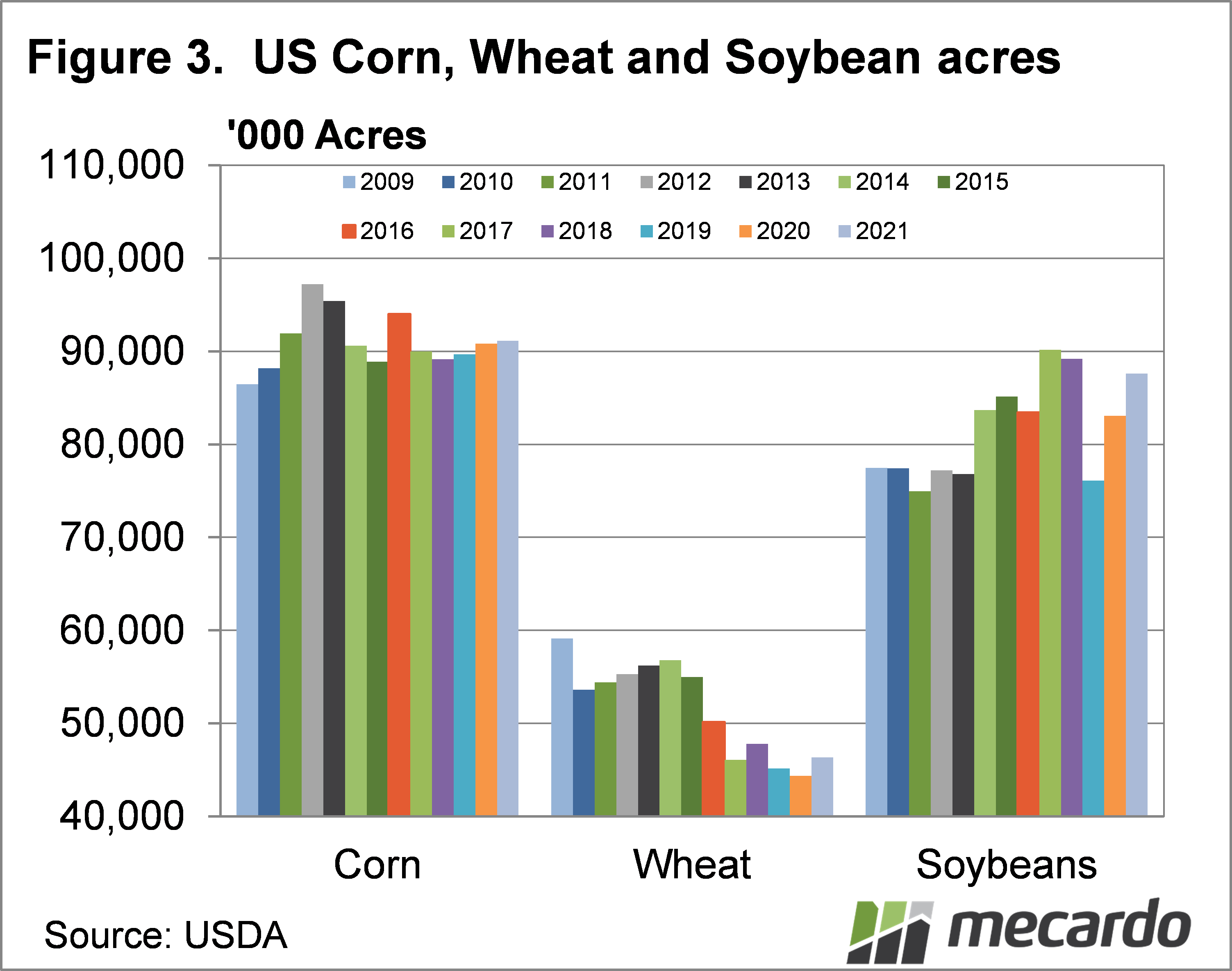

Which such strong increases in corn and soybean prices over the last year, and with values at eight-year highs, surely grain producers in the US are planting more corn and soybeans? The acreage estimates, shown in figure 3, forecast only a marginal lift in corn plantings. Soybeans did see more of a reaction, with plantings growing by 4.5%

Despite price increases being more moderate, total wheat plantings are expected to lift 4.5%. All of the increase in wheat acreage was for winter wheat however, which was planted back in November, before the full price movements had been realized. Spring wheat plantings were down on last year, which makes sense given the current price spreads.

What does it mean?

The market was expecting an increase in corn acreage, and while soybean did rise, it wasn’t as strong as expected. The result was a jump in deferred contract prices. The new crop corn and soybean futures were discounted to the spot market, on the expectation of big crops. Some of this production has been wiped off.

Have any questions or comments?

Key Points

- Corn and soybean prices have rallied over the past year.

- Higher prices were expected to see increases in corn and soybean acreages in 2021.

- Lower than expected corn and soybean acreage is supporting new crop values.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: USDA, Refinitiv, Mecardo