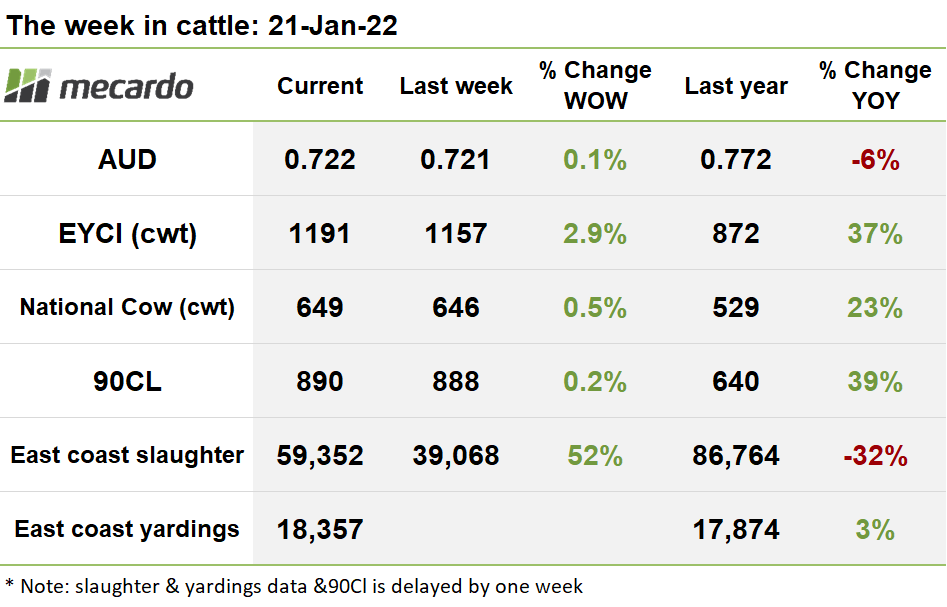

After an initial soft start for cattle markets last week, the pace has suddenly picked up, with the Eastern States Young Cattle Indicator (EYCI) rocketing up 3% into all time record territory again, and most other categories followed suit.

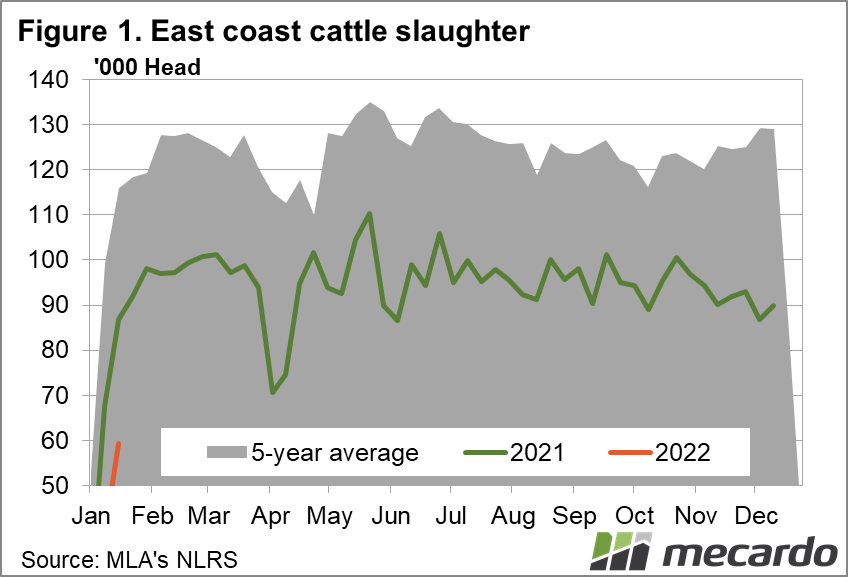

Last week’s slaughter figures showed a marked improvement, lifting 52%, to 59,352 head. Compared to where we were this time last year though, it’s still 32% off the pace, highlighting the issues with processor capacity.

Official yardings figures for last week pegged numbers at a lacklustre 18,357 head, most likely impacted by transport and seller confidence issues stemming from the latest outbreak of the Omicron strain of COVID-19 on the industry.

However, indications are that this week is likely to have experienced a strong influx of supply. The rolling 7-day average number of EYCI eligible cattle , which provides a good early sneak peek indicator for weekly whole of market yardings almost doubled from the prior week to 13K head.

Despite the substantial increase in EYCI eligible cattle on offer, there was clearly no shortage of eager buyers and strong demand for young cattle. The EYCI rose 33¢(3%) to close the week at a scorching new all time record high of 1,191¢/kg cwt – representing a 37% lift on where it was at the same time last year.

Roma store provided the main impetus for the EYCI this week, contributing 28% of total volumes, at a heady price of 1,304¢/kg cwt, closely followed by Dalby, which was responsible for 20% of volume, albeit at lower an average price of 1,178¢/kg cwt in contrast.

Over in the west, the WYCI took an apparent severe beating, plummeting 90¢(8%) down to 1,060¢/kg cwt. The market was impacted by a combination of thin yardings of only 332 cattle (down 84%), and a bias toward cheaper heifers in the week’s mix. WA Vealer steers traded up 60¢(5%) at 1,223¢/kg cwt.

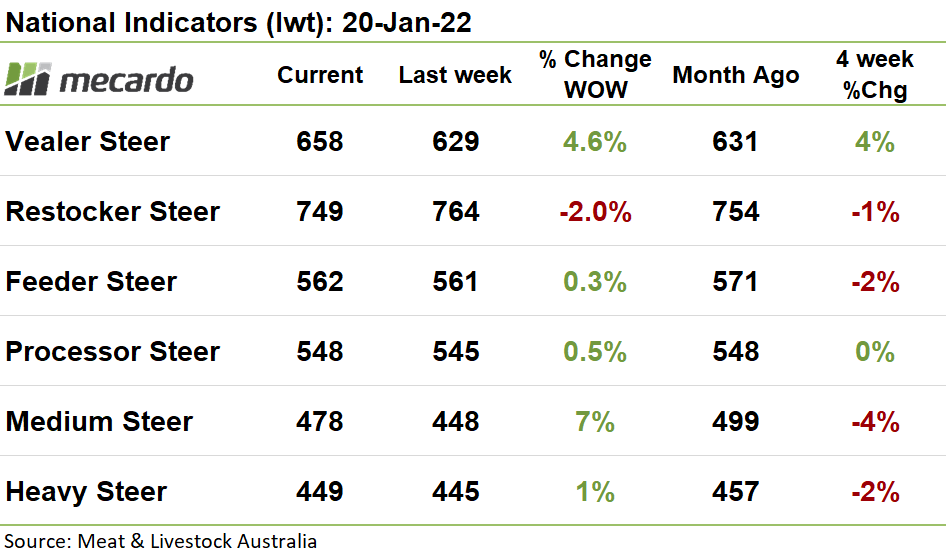

On the national categories, there was more encouraging news across the board, with almost all cattle types notching up gains for the week. The standout performer was the Medium Steer price, which rose 30¢(7%) week on week to close at 478¢/kg lwt. However, the wooden spoon went to Restocker Steers, whose price slipped 16¢(2%) to 749¢/kg lwt.

The all-important US 90CL frozen cow price lifted 2¢ to 890¢/kg. Steiner reports that elevated prices for lean beef can be expected in US from March onwards, as domestic slaughter declines, and seasonal demand picks up, painting a positive picture for 90CL in the near term future. The Aussie dollar strengthened marginally to US0.722

The week ahead….

The strong lift in both the benchmark EYCI, and most other categories this week, combined with initial indications that more supply flowed into the market (which would normally have a dampening effect on prices) signifies that cattle demand is currently red hot. There is no reason not to expect more positivity in the markets, especially further ahead as supply chains recover with more personnel returning to work post COVID exposure.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: MLA, Mecardo