A correspondent asked this week about staple strength in 17 micron wool, and whether there was a significant or critical level with regards to price. Such queries are always welcome, so this article takes a look at staple strength in 17 micron fleece.

Mecardo has looked at trends in premiums and discounts for staple strength and staple length in past articles. In addition to these longer term trends, the greasy wool market is now adding the complexity of non-mulesed certification and over the top of that, various quality systems certification for animal welfare and/or wool quality.

As a start Figure 1 looks at the median price for eastern Australian 17 micron fleece (plus locks and crutchings as a bookend for the lower value wool) with a greasy staple length of 90 mm and a range of staple strengths, for the past five years. The bars show price (right hand scale) and the line is the premium discount (left hand scale) relative to the price for 35-39 N/ktx strength wool. Vegetable fault is limited to a maximum of 2% and no subjective faults (water stain, cott and so on) are allowed.

The median discount for staple strength falls quickly when the strength drops below 30 N/ktx, steadying out around 5-6%. This will vary according to the accompanying point of break in the middle (POM). A high POM makes effective staple strength lower, and the likely discount greater. On the positive side, premiums appear when the staple strength rises to 40 and higher. It is these categories where the presence of NM and or quality scheme accreditations appear in the current market, adding further substantial premiums if all the required specifications are present. The extra premiums are conditional on the lot of wool being “just right”.

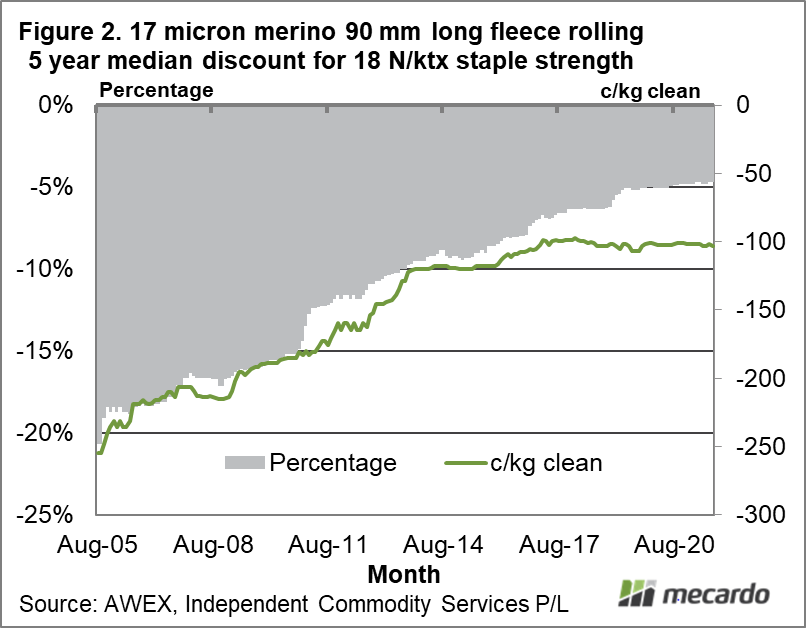

From the perspective of the original question, there is no critical staple strength level, rather a gentle and moderate continuum of discounts to premiums as staple strength rises from very low to high levels. This situation has not always been the case. Figure 2 shows the rolling five year median discount for sub-20 N/ktx strength 17 micron fleece from 2005 through to this month. The rolling five year median discount is used to illustrate how the discounts have shrunk in the past two decades. If this question was asked 16 years ago, the five year median level then would have shown a substantial discount of 20% or 250 cents clean. The discount for low staple strength has shrunk substantially since then. In recent years it has stabilised around 5%, while in cents per kg clean terms it has stabilised around 100-120 cents since 2014.

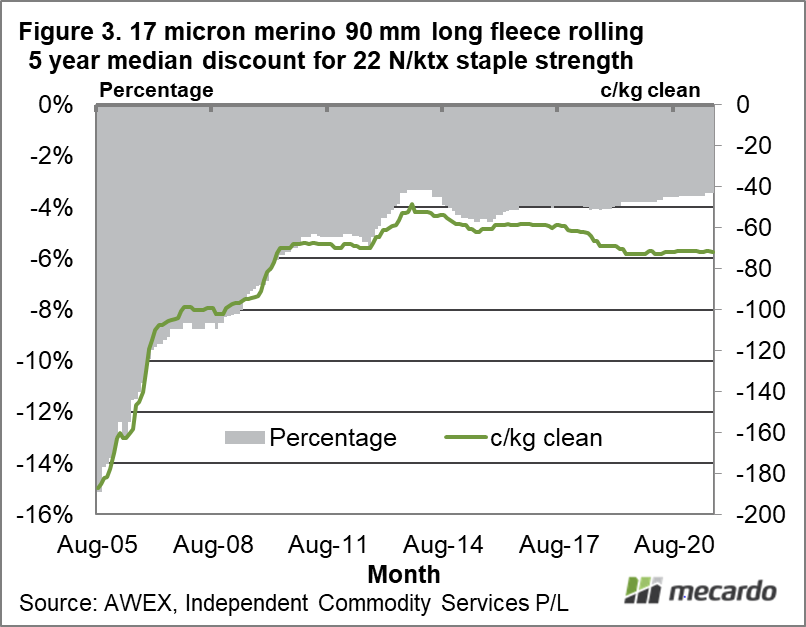

Figure 3 repeats the exercise for Figure 2, for 20-24 N/ktx wool. It shows a similar story with the discount steadying out around 4% or 60-80 cents clean.

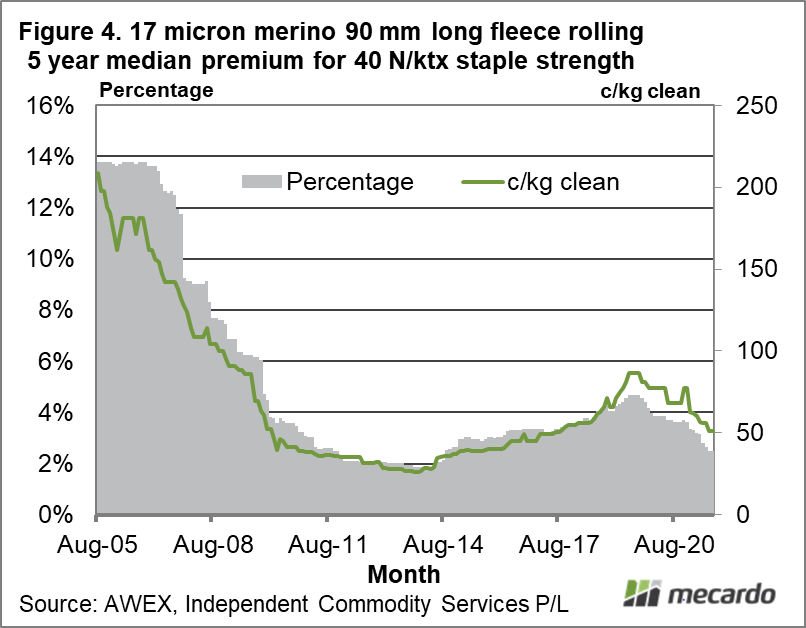

Figure 4 looks at the premium for good style 40 N/ktx strength wool. It shrank from 2006 through to 2012, before steadying. It picked up in the 2018 rising price cycle before falling with the 2019 down cycle and then under the impact of COVID in 2020. As mentioned above, pricing for this category of wool has become more complex with the growth in demand for NM wool and above that quality scheme accredited wool.

What does it mean?

Unlike the 1990s, staple strength is generally not a big issue for pricing fine Merino wool. It will be occasionally when the supply of low strength wool is high, but in structural terms the pricing of staple strength by the supply chain is only one quarter to one third of the levels from 20 years ago. High staple strength is currently a pre-requisite for access to NM/quality accredited premiums, but this market is still in its early stages of development.

Have any questions or comments?

Key Points

- The effect of staple strength on price for 17 micron fleece has shrunk substantially during the past two decades.

- There is no real inflection point in low staple strength at which discounts widen dramatically.

- High staple strength is becoming a condition of eligibility for premiums for NM and or quality schemes.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: AWEX, Ilfracombe, ICS