A couple of weeks ago we had a look at lamb slaughter, while only touching briefly on the sheep side of the market. Sheep sale prices are very important to most sheep and wool operations, so it’s worth a deeper dive into the market.

While the mutton market has shrunk with the flock, and lambs now dominate the sheepmeat market, sheep sales are still important. The forecast this year was for a big jump in sheep numbers coming to the market. This hasn’t eventuated, which begs the question as to whether they are still to come over the summer.

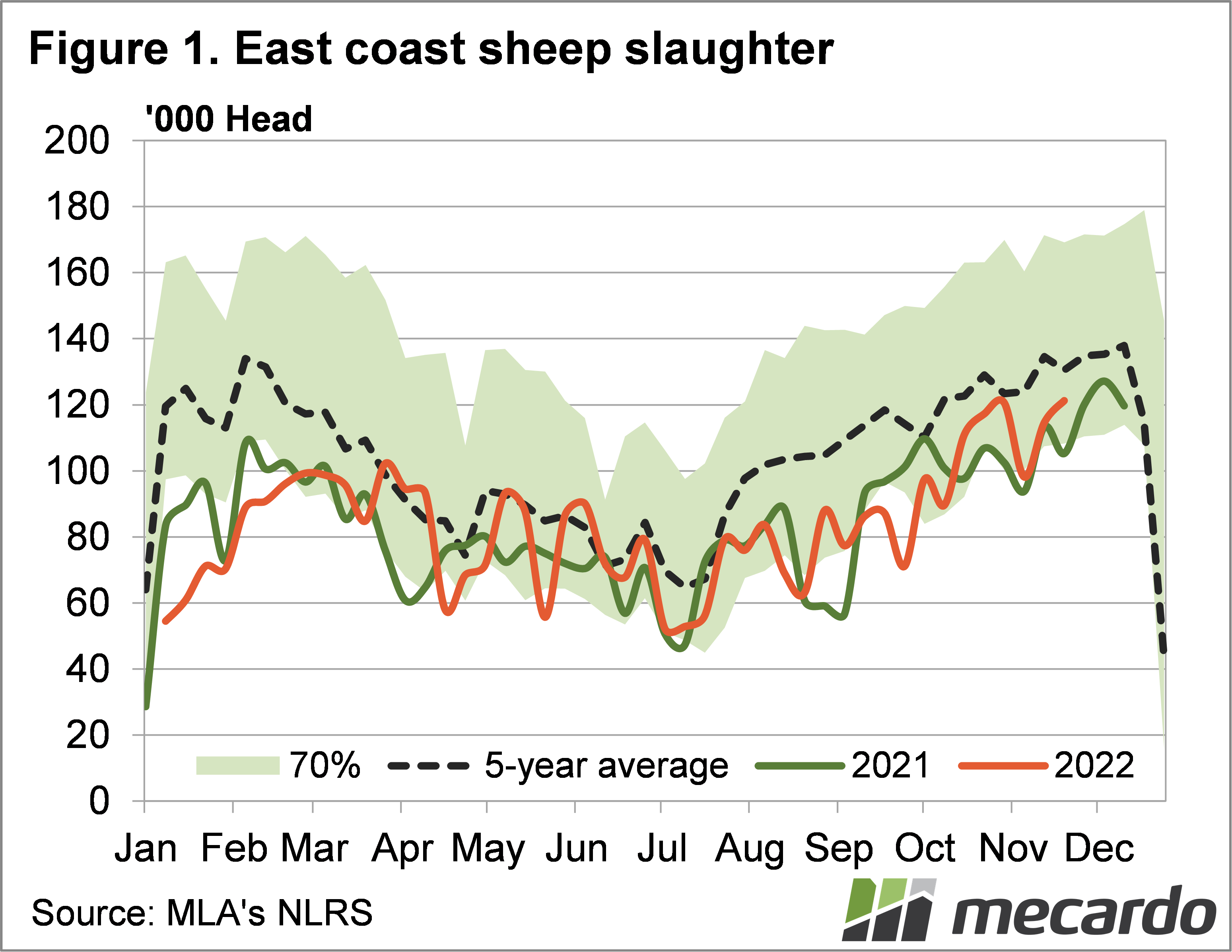

Figure 1 shows east coast sheep slaughter. For the year to date just 12,153 more sheep have been slaughtered than the record low year of 2021. This equates to 0.3%, which is obviously way off the 20% increase MLA were forecasting in their June projections.

We know there are more sheep out there, with the breeding ewe flock growing according to survey data. Over 2 million head have been added in the last two years. It seems that for 2022 at least, ewes are being kept on farm for further breeding, rather than selling for slaughter. Additionally, lower lamb slaughter rates in recent years suggest plenty of young ewes are being kept to add to the breeding flock. The flush of sheep might be delayed, compared to lamb.

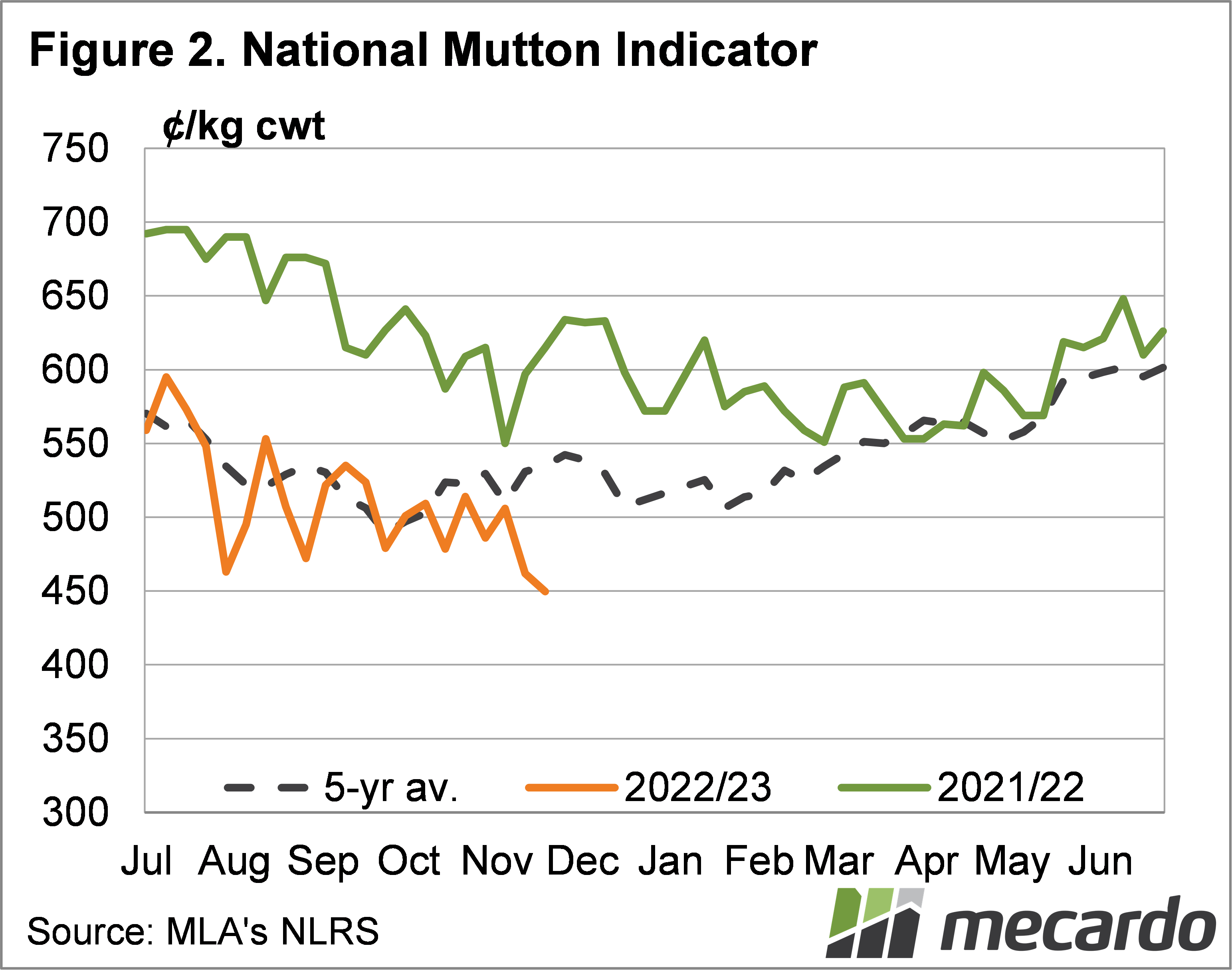

Despite sheep supply being similar to last year, prices have tracked much lower this year. Figure 2 shows the National Mutton Indicator (NMI) last week hit a three and a half year low of 449¢/kg cwt, 26% lower than the same time last year.

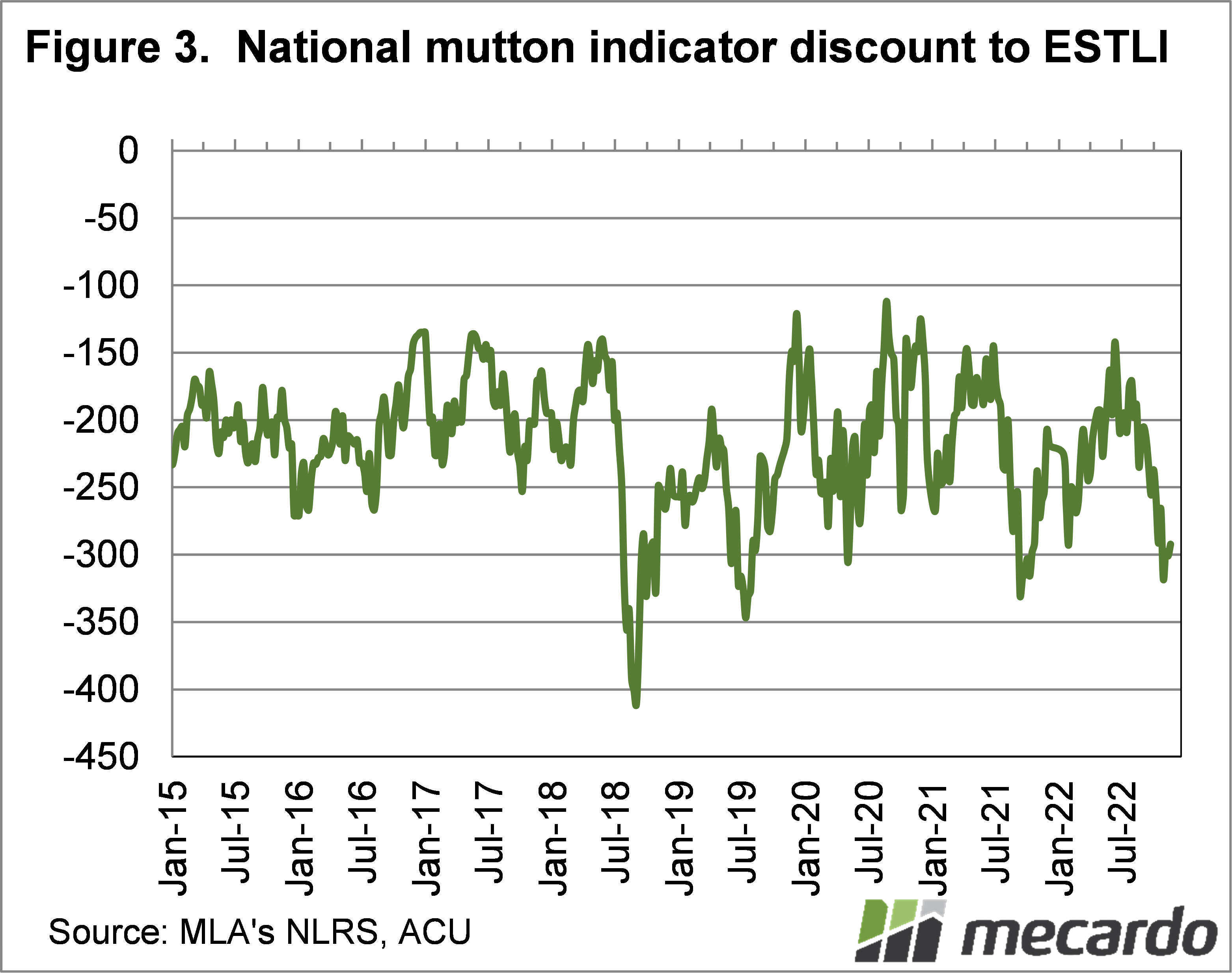

Mutton is also cheap relative to lamb. Figure 3 shows the NMI sitting at close to a 300¢, or 39% discount to the Eastern States Trade Lamb Indicator (ESTLI). There appears to be little additional downside for the NMI, if lamb prices can hold, as the discount is close to historical lows.

What does it mean?

The supply of sheep doesn’t seem to be overwhelming the market, but like the store lamb market, it is likely the lack of restocker demand which is depressing prices. The export market for mutton is steady at best, and without restockers competing for stock prices are low.

When crops come off we might see some improved restocker demand in areas where stubbles are grazable, and this could see up to 100¢ upside in the mutton price. At $20-30 per head it might be worth waiting for.

Have any questions or comments?

Key Points

- Sheep supply has been tracking similar to last year, but prices are much lower.

- Demand issues are likely the cause of weak absolute and relative mutton prices.

- There is some upside in mutton prices when crops come off and demand improves.

Click on figure to expand

Data sources: ABS, MLA