It’s been four months since we had a look at the much-talked-about Middle Eastern lamb export market. With the export data for the first two months of the year, along with slaughter weights for the December quarter, it’s time to again assess how many lambs have exited the market early.

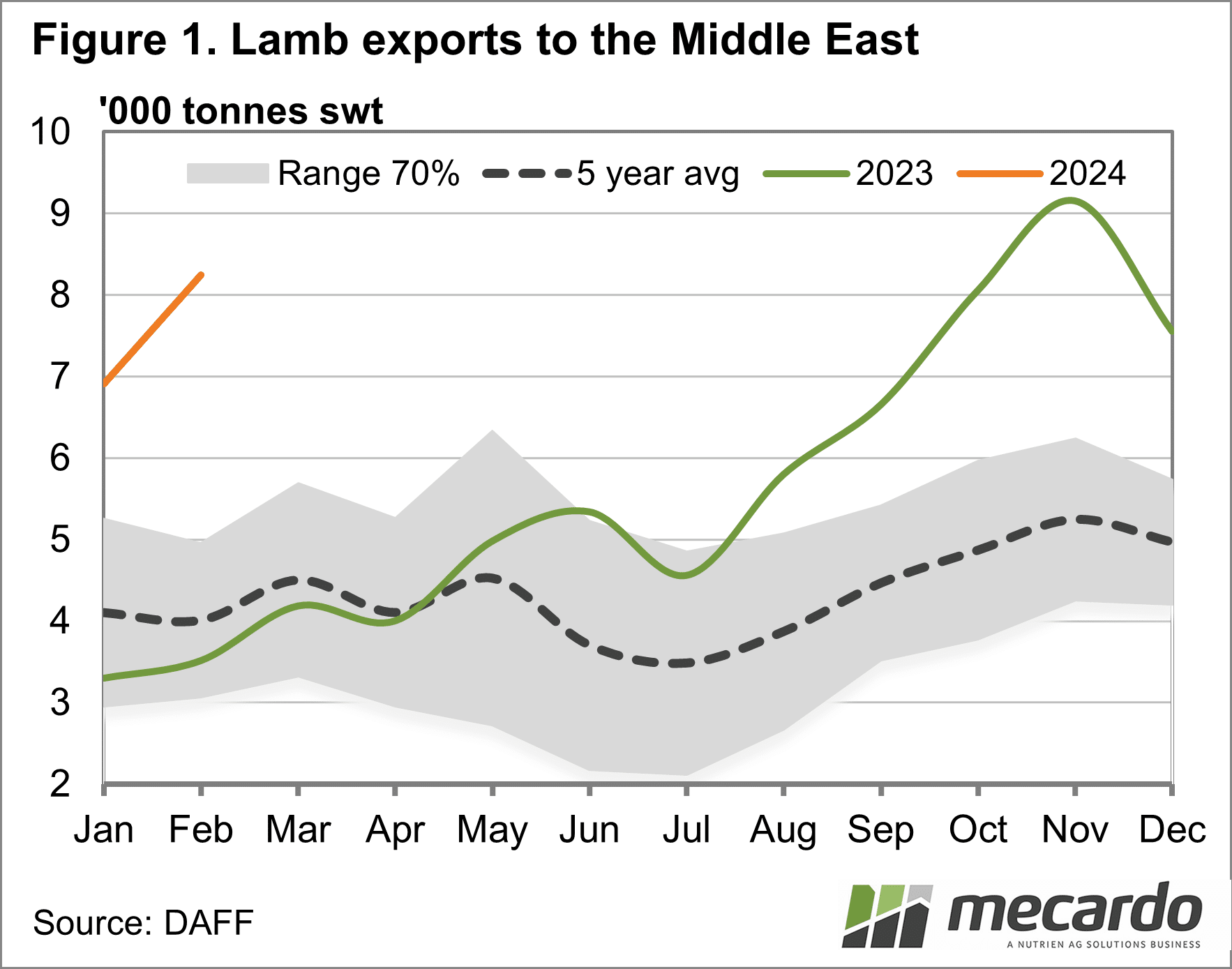

Figure 1

shows lamb exports to the Middle East have continued their strong form early in

2024. While not quite up to the highs of

November, we have sent 122% more lamb in January and February than at the same

time last year.

For the 2023

crop of lambs, by which we have a rough measure of sales starting in July, lamb

exports to the Middle East have been up 116%.

In terms of tonnage, Australia has exported 30,618 tonnes more lamb to

the Middle East since July.

Since 2022

the Middle Eastern market share has grown from 13% to 20.6% in 2023, and 27%

for the first two months of 2024.

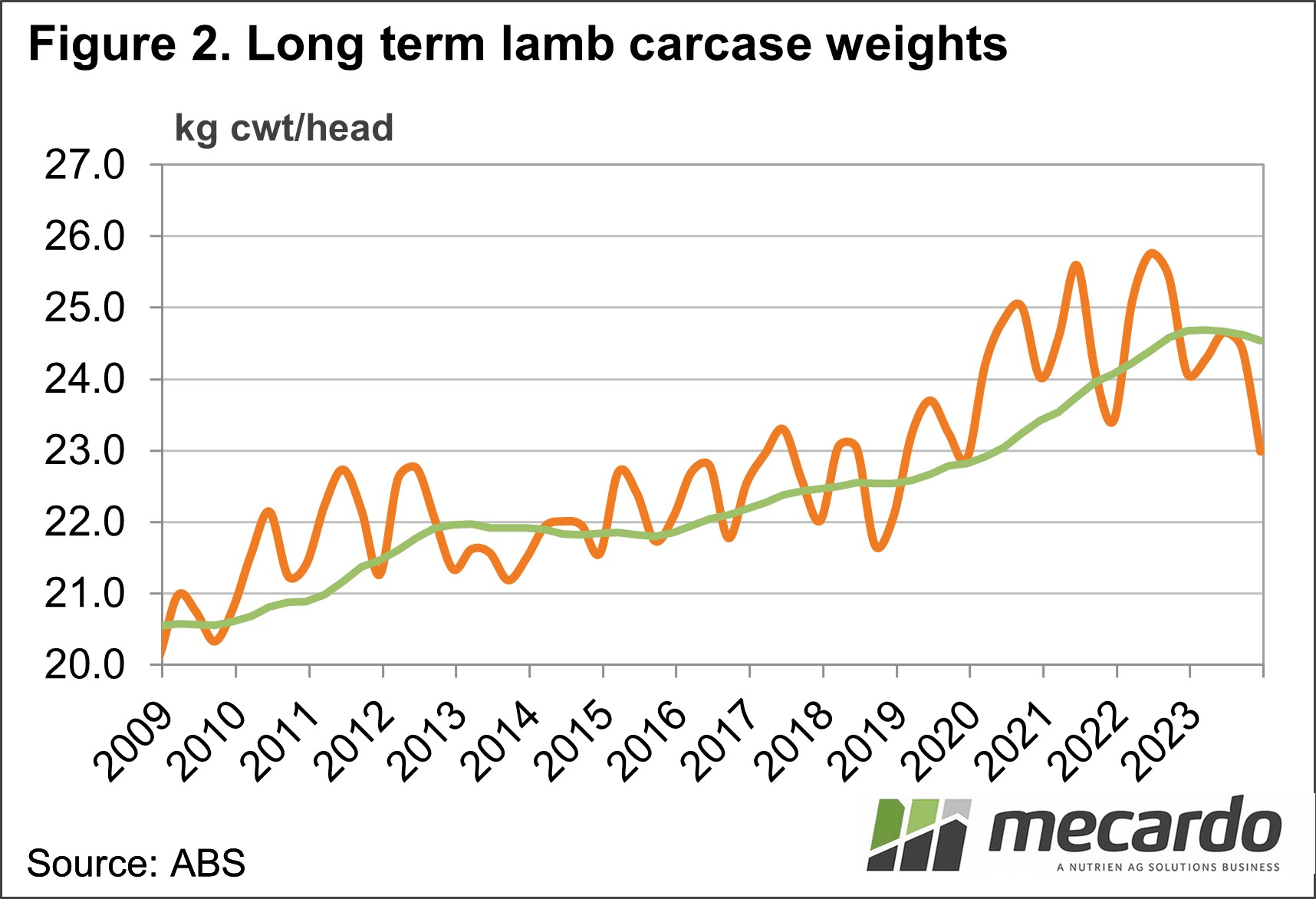

To work out

how many extra lambs this was, we need to take a look at lamb slaughter

weights. Figure 2 shows lamb slaughter

weights hit a two-and-a-half-year low in 2023.

The December average slaughter weight was 23kgs cwt, which is well down

on most of the 2020-2023 quarters, but it is strong compared to pre-2020

levels.

While we

can’t know the average weight of lambs going to the Middle East, we know that

they are among the lightest lambs marketed.

If we work on 19kgs cwt, the extra lambs exported to the Middle East

equates to 1.61 million. To put this in

context Meat and Livestock Australia are forecasting lamb slaughter this year

to hit 26 million head.

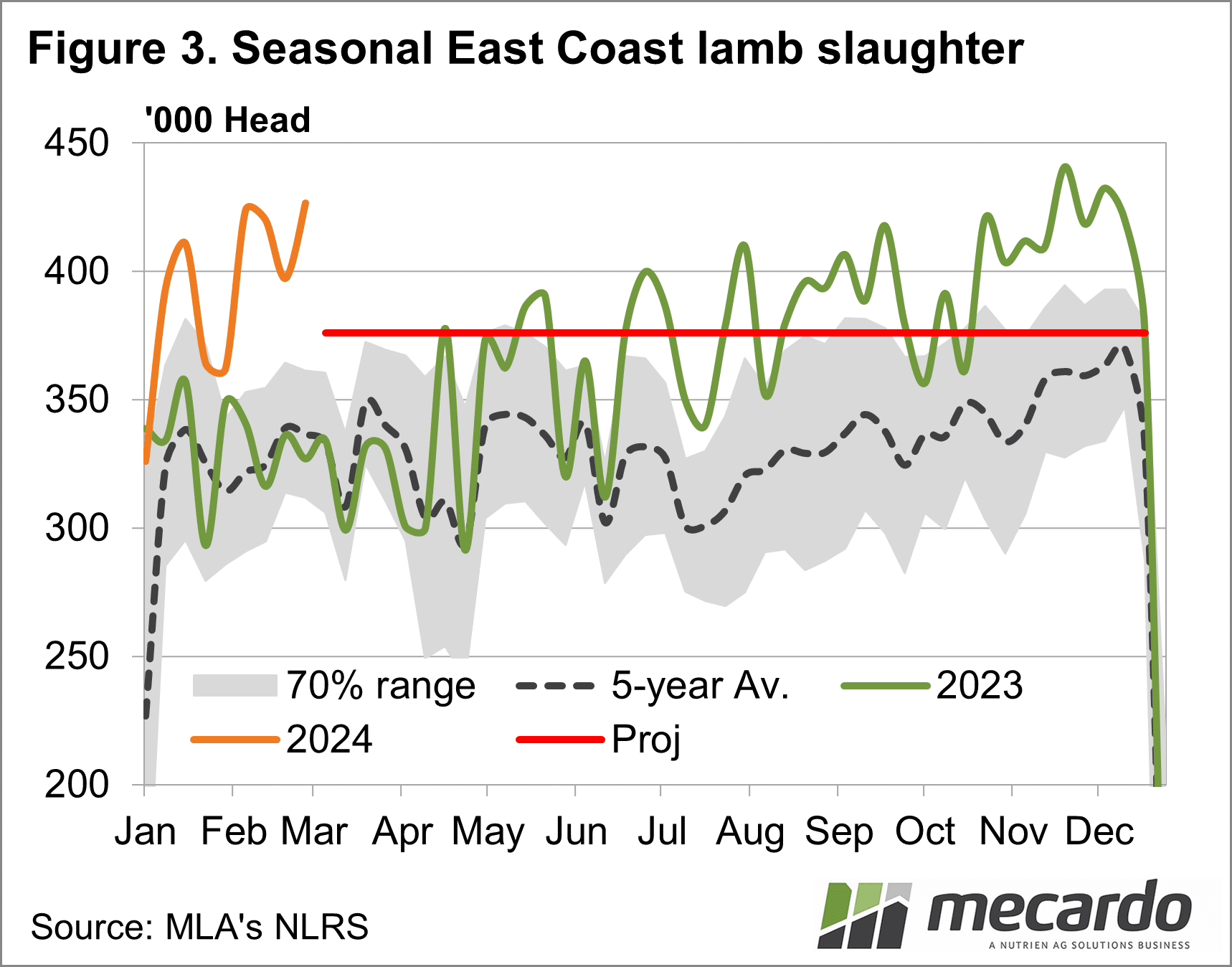

Figure 3 shows

that lamb slaughter hasn’t slowed down early in 2024, with the slaughter space

opened up in November and December, remaining in place this year. It is interesting to see that lamb supply

hasn’t slowed with the big numbers exiting early.

In fact, lamb

slaughter has been up 18% on last year, or 532,000 head, based on MLA’s weekly

data. MLA is forecasting a 5% increase

in total lamb slaughter this year, which equates to 1.2 million head. We can run some extremely basic calculations

on this.

With nearly

half the forecast yearly increase in lamb slaughter having been achieved

already, it means that slaughter will have to slow at some stage. The red line on Figure 3 shows where average

weekly lamb slaughter would have to sit to meet the 26 million head

forecast.

What does it mean?

It’s hard to think lamb slaughter can keep up this pace unless the lamb crop in 2023 was up 15-20% on 2022. This is possible but seems unlikely given what we know from survey data. What’s more likely is slowing lamb slaughter, and this fits with seasonal trends. The question is what sort of impact this has on prices?

Have any questions or comments?

Key Points

- Lamb exports to the Middle East continue to run hot.

- Slaughter weights were down in December, due to increased sales of lighter lambs.

- Strong lamb slaughter early this year should result in slower supply at some stage.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: ABS, MLA, Mecardo