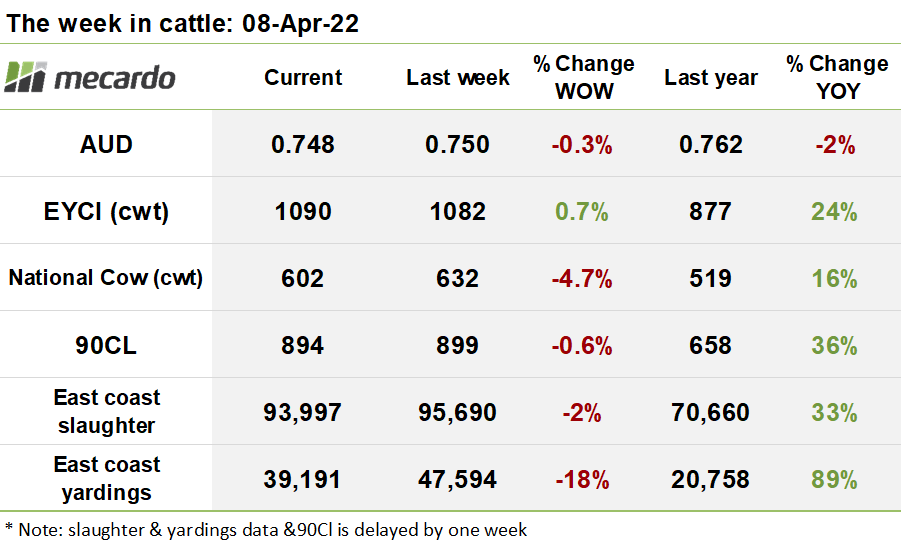

There has been evidence of a bit of a late surge of cattle to the yards this week, as producers try to get ahead of the extended slowdown and shut saleyards across the string of Easter and ANZAC four-day weeks in the month ahead. Heavy steer prices jumped up, but cow prices have continued to decline, while the US cow liquidation spree sets up support for future prices in 2023/24.

East Coast slaughter dipped 2% last week to 93,997 head. Most states were relatively stable on last week, although NSW volumes took a 7% week on week decline. Slaughter normally always takes a sizable dip in April due to Easter holiday period, so we can expect numbers to drop for the coming few weeks as the number of processing days reduces for some plants. Traditionally, the industry will operate at 75% due to staffing shortages and avoidance of paying public holiday wage penalties rates.

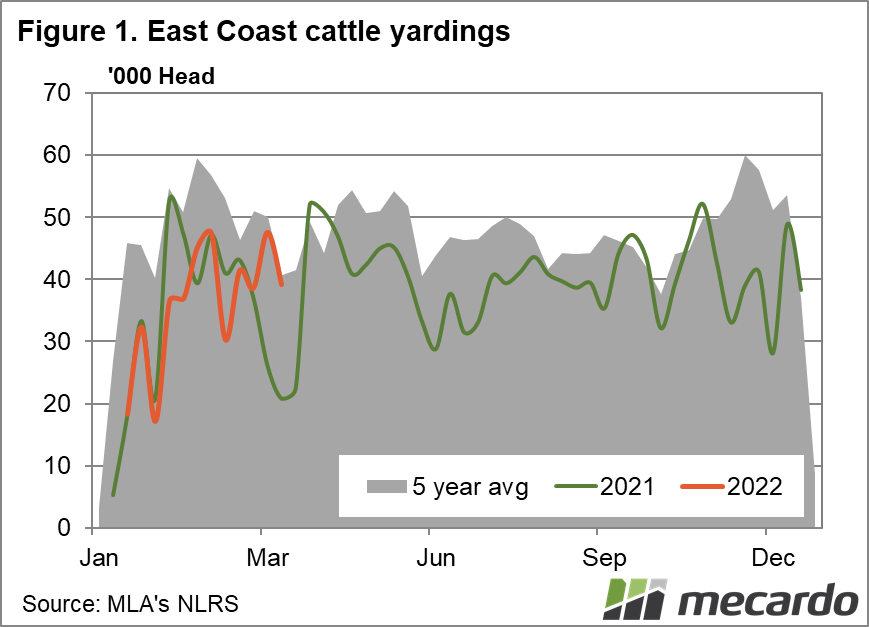

East coast yardings dropped back 18% last week to 39,191 head, with the majority of the pullback in offerings emanating from NSW & QLD, where numbers were down 26% & 18% on the week prior. Similar to the story for slaughter, the easter holiday period and ANZAC day will weigh heavily on yardings in the next few weeks, with three four-day weeks in a row coming up.

EYCI eligible yardings this week rose 37% to 11,322 head this week, possibly related to late rush to the market before the extended slowdown that will occur over the Easter period. MLA’s Jenny Lim reports that sales that will be skipped over the coming weeks include Dubbo, Tamworth and Wagga, and the Griffith feeder sale wont be going ahead.

Despite the higher, but not extraordinary numbers yarded this week, the EYCI inched up 8¢(<1%) to close the week at 1,090¢/kg cwt. The usual saleyards provided the key influence on the index, with Roma at 21% at 1,097¢/kg cwt, and Wagga 14% at 1125¢/kg.

Over in the west, the WYCI strengthened again, 65¢(6%) to 1,192¢/kg cwt, on a smaller yarding of 605 eligible head, partially influenced by a 5% uptick in the higher priced vealer proportion of the index to 90%.

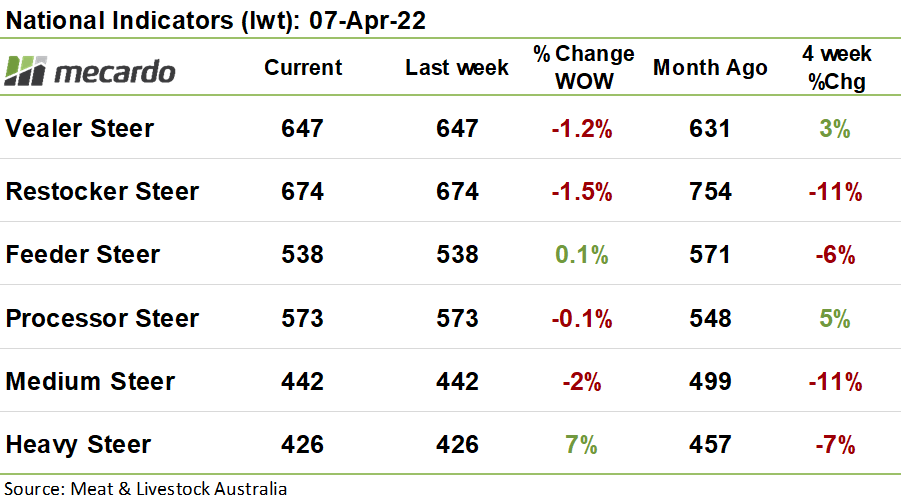

The national categories were all swings and roundabouts this week, with the heavy steer indicator lifting a whopping 30¢(7%) to close at 457¢/kg lwt. In contrast, the wooden spoon was awarded to medium cows, which shed 16¢(5%) to settle at 325¢/kg lwt, and the rest all posted moderate losses.

The US frozen cow 90CL dipped 1¢ to 304¢US/lb and lost 5¢(<1%) in Aussie dollar terms, closing the week at 894¢/kg swt. The US continues to post record high cow slaughter, with the high cost of feed forcing the hand of producers into liquidation. The potentially deep liquidation cycle that is shaping up is set to create a substantial hole in US beef supply in 2023 and 2024 as the calf crop reduces, and any rebuild leads to higher retention, and higher prices. In the medium term though, all eyes are on the volumes of beef coming out of Brazil to assess the impact of the 26% MFN out of quota tariff which kicked in this month.

The week ahead….

Next week is a shorter four-day week for the saleyards, and lower processing activity due to easter holidays, so with many market participants absent, or in holiday mode, cattle market activity will be subdued. A softer week would not be a surprise.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: MLA, Mecardo