Quality schemes continue to be a topic of conversation in the greasy wool markets, with some large premiums appearing this season for RWS accredited wool in particular, but not exclusively. This article takes a look at RWS premiums for the season and during June, as well as volumes for combing merino fleece.

When developing an estimate of price effect (premium or discount) it is necessary to calculate a base price to enable a comparison. In a season where micron premiums and discounts have been at extreme levels, a difference of 0.1 micron can mean a sizeable difference in price and potential error when calculating premiums and discounts. Added to that has been the effect of vegetable fault (VM) both early in the season (view article from 2021) and since January, where big steps in price can result from relatively small changes in VM. As the market has moved through the autumn the level of cott and water stain has increased (water stain is running at 4-6 times normal levels in the Australian wool clip). All of these factors have complicated the price structure of greasy wool market this season.

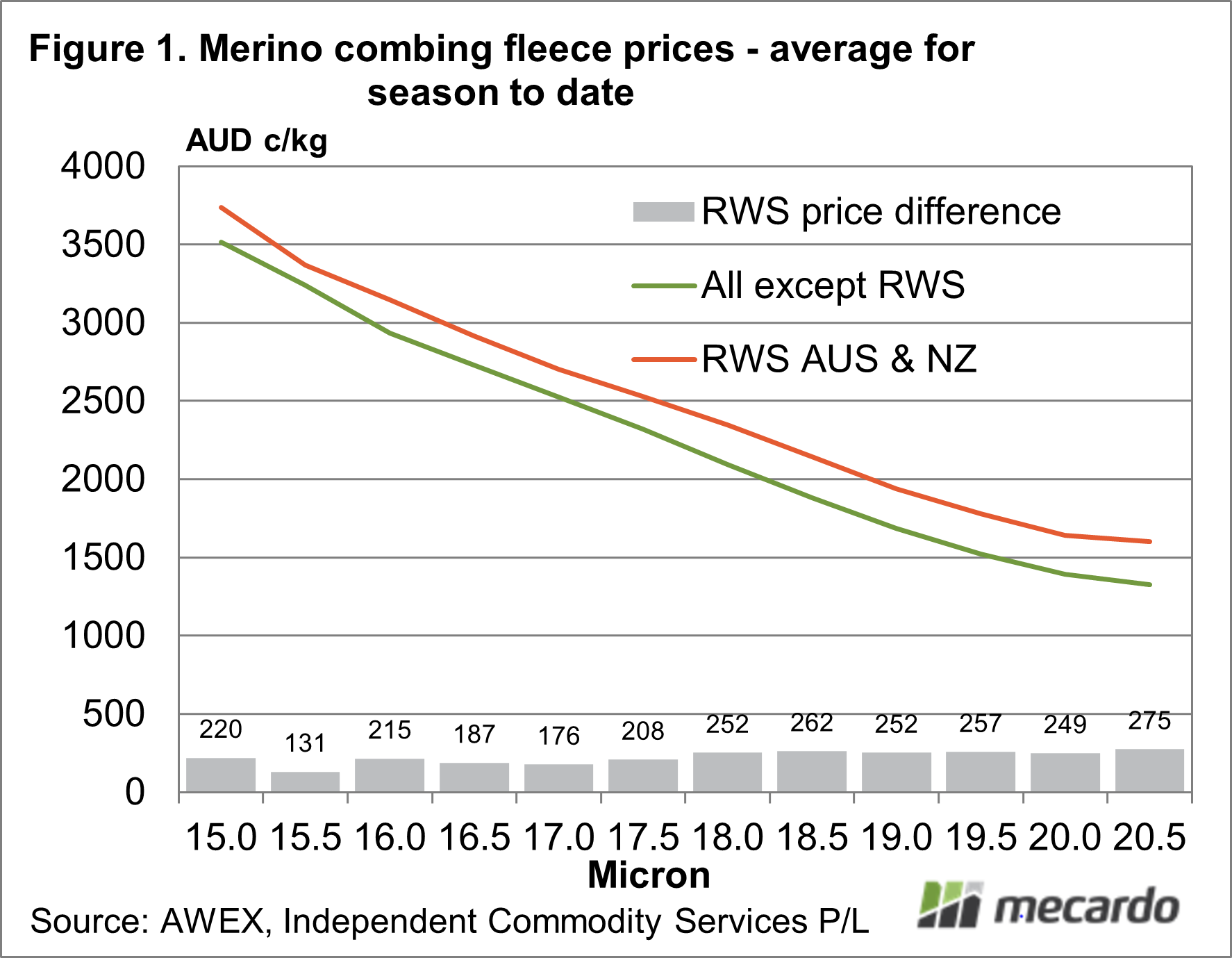

With the above in mind a wide view of prices for RWS accredited merino fleece and non-RWS as shown in Figure 1 has been used. The base wool category used in Figure 1 is combing merino fleece sold in the eastern selling centres, which is 50 mm and longer, has a vegetable fault 2% and lower, a staple strength of 30 N/ktx or more and no subjective fault thereby excluding wool with cott, water stain and other subjectively assessed faults. An average price for the season, by half micron, for RWS accredited fleece varies between 131 and 275 cents above non-RWS merino fleece.

The premium is fairly consistent in cents per kg terms between micron categories, although they are smaller for the finer micron categories. This matches premiums published by Cape Wools for the South African market (17 through 22 micron) which also tends to be consistent between micron categories (view earlier article from this year).

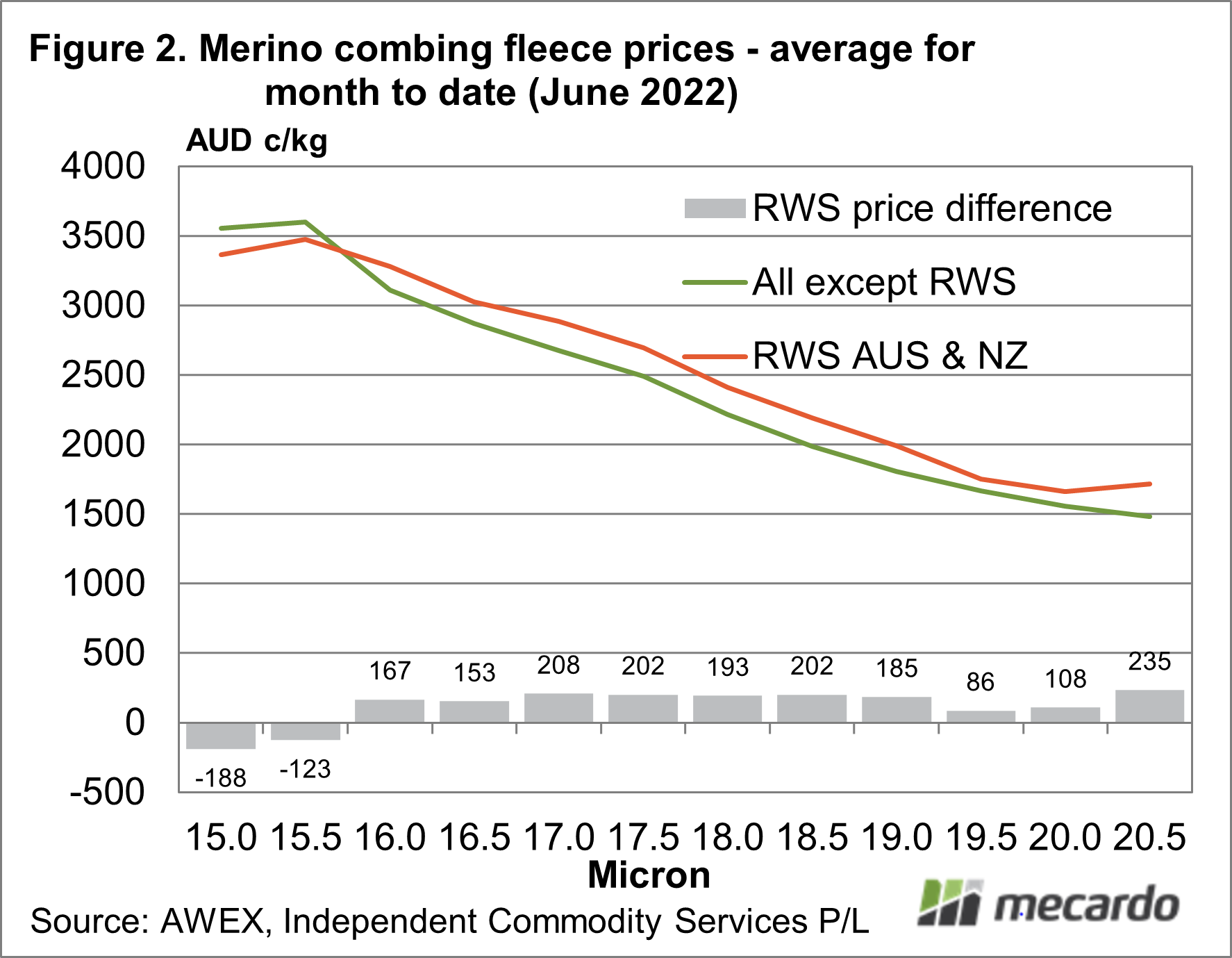

Figure 2 narrows the timeframe to June 2022 (to last week) while using the same series as in Figure 1. The price difference is more varied, dipping to a negative for 15 and 15.5 micron. This is not necessarily a discount but a function of limited volumes, varied timing of sales and extreme micron premiums and discounts. It is a reminder that the price effect of RWS does vary at the sale lot level. Exporters work on mill consignment averages, while famers sell wool in individual sale lots.

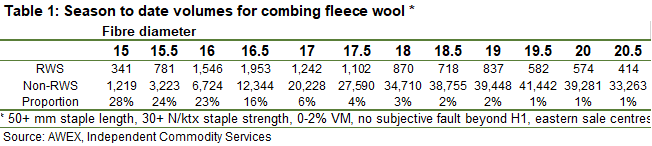

On average the premium for good merino fleece wool accredited to RWS has been extraordinary this season. Table 1 shows the volume, in farm bales, for the prices shown in Figure 1. The proportion of volume of good fleece wool sold this season accredited to RWS ranges from around one quarter for 15 to 16 micron down to 1% for 19.5 to 20.5 micron. Volumes of RWS accredited wool remain low in Australia, for 17 micron and broader merino wool.

What does it mean?

Premiums for RWS wool were first published by Cape Wools in October 2021 which seemed to spark premiums in the Australian greasy wool market. This was only nine months ago, so it is early days in terms of Australian farmers, their adoption of quality schemes and the response of the supply chain to increased premiums and presumably growing supply.

Have any questions or comments?

Key Points

- On average RWS accredited good merino fleece wool has sold for substantial premiums this season.

- The premium is fairly consistent between micron categories in c/kg terms, although it does shrink for the finer micron categories.

- Volumes of RWS accredited good merino fleece wool remain low, accounting for about one quarter for 15-16 micron, down to 1% for 19.5-20.5 micron.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources:

AWEX, Cape Wools, ICS