As previous Mecardo articles have noted, greasy wool prices tend to follow the same general cycles and patterns of the bigger apparel fibre markets, responding to common economic factors. What does vary are the relative prices for different categories of greasy wool, often from a change in supply and occasionally from a change in demand. This article is an update on apparel fibre prices.

While price levels for the major apparel fibres do not necessarily tell us what price level a given category of wool should be trading at, they do provide context for wool prices helping round out the greater apparel fibre story within which the various categories of wool operate.

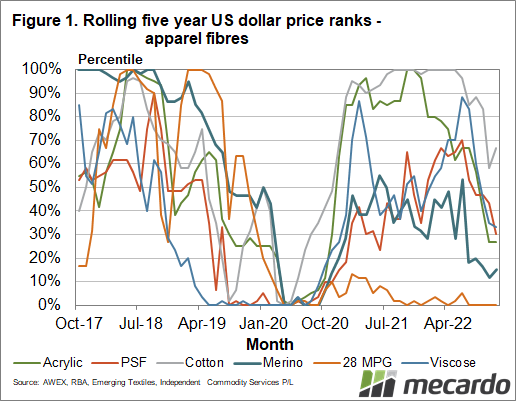

Figure 1 shows the rolling five-year price ranks for a range of apparel fibres, including merino (effectively around 19 micron) and the 28 MPG, in US dollar terms. At first appearance, it resembles something Jackson Pollack may have painted but there are some interesting pieces of information in it. Firstly it shows the overwhelming effect of the pandemic in 2020, pushing all prices down to five-year lows, which is a classic case of a major world event (the economic repercussion in this case) affecting all apparel fibres. The 2008-9 financial crisis was a similar event.

Since mid-2022 the rolling price ranks of all apparel fibres have fallen. Even the 28 MPG managed to lose some ranking, which is not easy when prices are already depressed. The easing trend in price seen in recent months has been a common feature of apparel fibre prices. It looks to be a response to the deterioration in economic conditions in the major northern hemisphere economies.

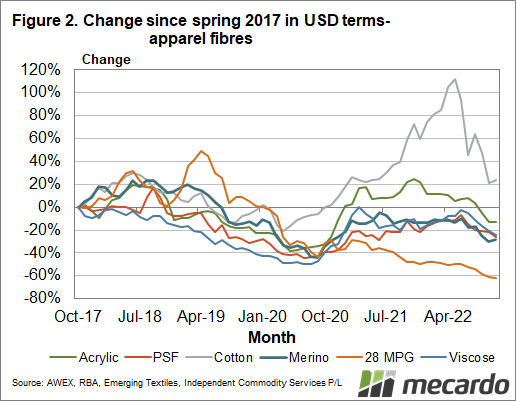

Figure 2 takes a look at the changes in price from the spring of 2017 for the same apparel fibres as shown in Figure 1, also in US dollar terms. The down cycle in 2019 dragged all prices lower, which was then extended by the pandemic in 2020. Excepting crossbred wool, all fibres then made a recovery from mid-2020 into mid-2022 before rolling over. It is a similar story to Figure 1, but less messy to look at. In this cotton remains the outperformer on the upside, crossbred remains the outperformer on the downside and the rest of the fibres are bunched together in the middle.

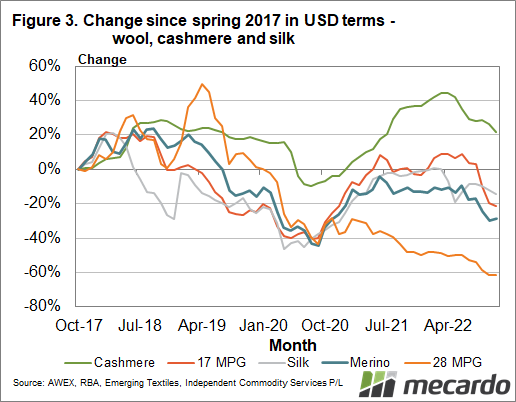

Figure 3 takes the same format as Figure 2 but focuses on categories of wool plus silk and cashmere. The same story is told of a down cycle, reaching a low in 2020 before prices rebound, with the exception of the 28 MPG which departed from the general trend of fibres in late 2020, continuing to fall in 2021 and 2022. Cashmere has been the outperformer of the natural fibres.

What does it mean?

Apparel fibres are looking for an improvement in the economic situation in the major northern economies to underpin a switch to a rising trend. This is unlikely to occur until well into 2023, at this stage. Hopefully, crossbred prices can hitch a ride on the next rising price cycle.

Have any questions or comments?

Key Points

- Apparel fibre prices have generally fallen since mid-2022, so wool continues to follow the lead of the larger apparel fibre complex.

- In terms of price movement since the spring of 2017, merino prices are in the main pack of fibre prices with cotton outperforming on the upside and crossbred underperforming on the downside.

Click on figure to expand

Click on figure to expand

Data sources: AWEX, RBA, Emerging Textiles, ICS