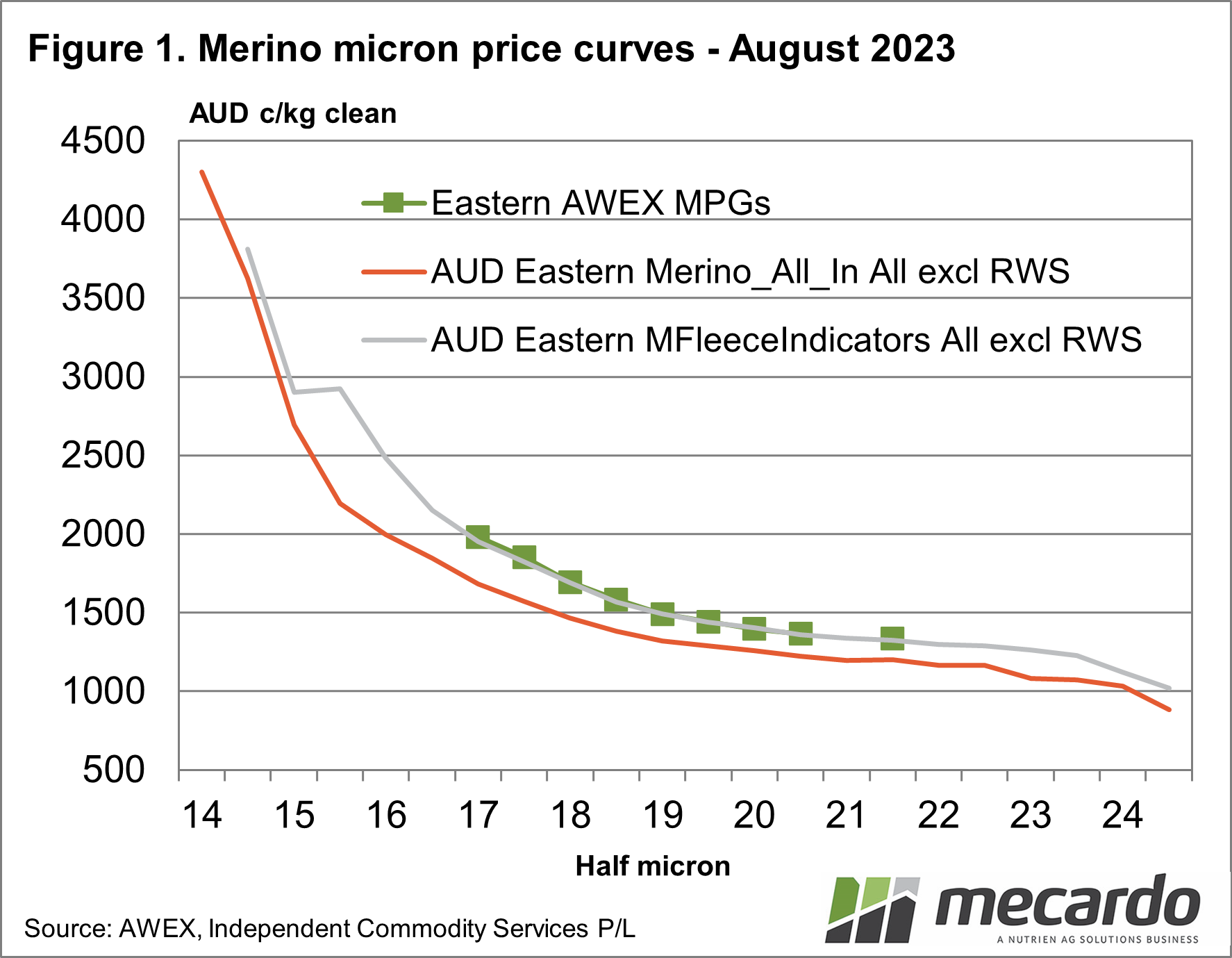

The range of AWEX indicators is restricted by the volume of suitable wool types for generating reliable quotes that are used internationally within the wool supply chain. As such merino MPGs are effectively limited to the range of 16.5 to 21 micron. In this article we use a wider basket of “indicator wool types”, without the responsibility which AWEX operates under, to generate price series both finer and broader than the MPG range.

In Figure 1 current (August 2023 averages to last week) price curves are shown for Eastern Merino “indicator” type fleeces (67-95 mm staple length, 35+ n/ktx staple strength, 0-1.8% VM, Team3 CVH less than 56%, yield of 60% or more and no subjective faults) excluding RWS accredited lots from 14 to 24 micron (grey line). For reference, the August average Eastern AWEX MPGS are overlaid. In addition, a second merino price series (orange line) is shown which includes all merino lots sold for each half-micron increment, regardless of quality or category. The data for this schematic is shown in Table 1.

The “indicator” fleece types do a reasonable job of mimicking the AWEX MPGs, at least for the bigger picture, which gives some confidence for using them to look at the finer and broader micron categories. The “All-In” series is lower as would be expected, including cardings and lower-value lots.

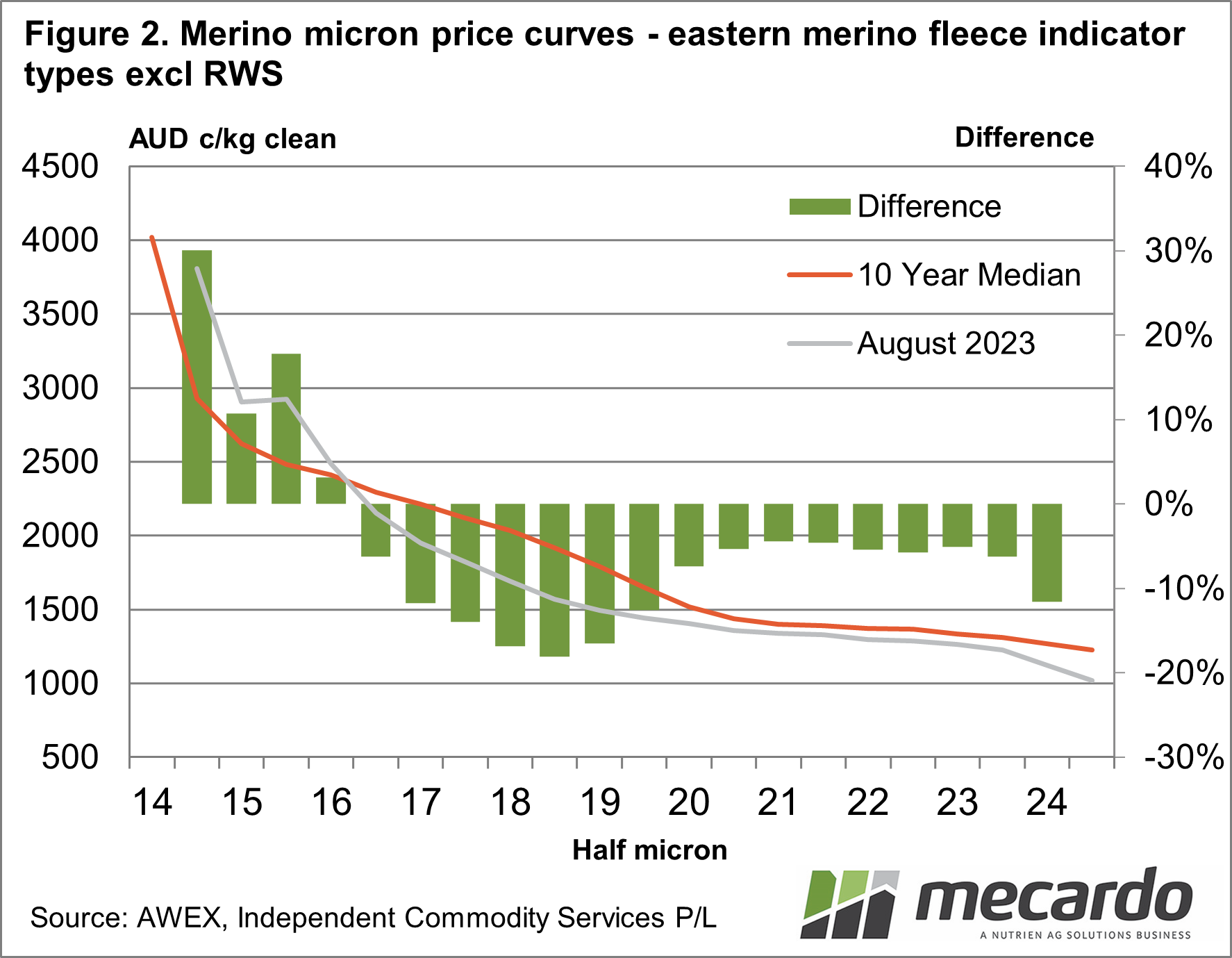

To put the current price series into some context, in Figure 2 the 10-year median (nominal) is compared to the current “indicator type” price series, with the bars showing the difference between the two. Interestingly the 15.5 micron and finer current price season remains above its 10-year median level. The 18-18.5 micron categories are the lowest in relation to the past decade, some 17-18% below the 10-year median. On the broader side of the distribution, the 20-23 micron categories are generally 5-6% below their respective 10-year median levels. The broader merino MPGs have been trading close to rolling 10-year medians for the past two years.

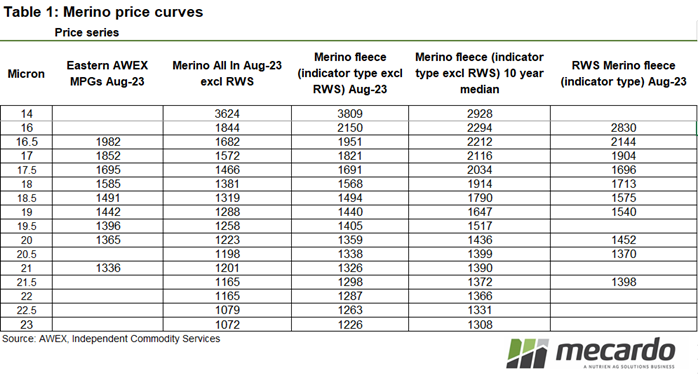

Table 1 has one extra series added, which is the “indicator type” series which were RWS accredited and sold in August to last week. This is a rough way to demonstrate RWS to non-RWS wool (as the timing of sales will have some big effects) but the message given is consistent with other analyses. The message is that while RWS-accredited “good” wool generally sells for a premium there are plenty that do not. The calculated average premiums incorporate lots which sold in a range from big premiums to small discounts. Calculated premiums also shrink as the quality of the wool declines.

What does it mean?

While fine wool prices have been under downward pressure it is not all bad news there with the very fine end doing relatively well at present. The broader merino categories are down 41% on their peak 2018 levels, which is a big fall (albeit from extremely high price levels) but they have been tracking their respective 10-year rolling median levels for the past two years. From this perspective, the market is not flagging itself as being at a low point.

Have any questions or comments?

Key Points

- 15.5 micron and finer merino fleece prices are still tracking above 10-year (nominal) median levels.

- The 18-micron category is performing the worst in relation to 10-year median levels, down some 18%.

- Broader merino fleece prices are currently 5-6% below 10-year median levels.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: AEX, ICS, Mecardo