Change in supply is a big driver in the change in relative price within the greasy wool market. Change in demand certainly plays a role in terms of the cycles of economic growth but these tend to be longer, multiyear cycles. Wool supply is sensitive to seasonal conditions which can change year to year. With this in mind this article takes a look at changes in the merino micron category volumes for last season.

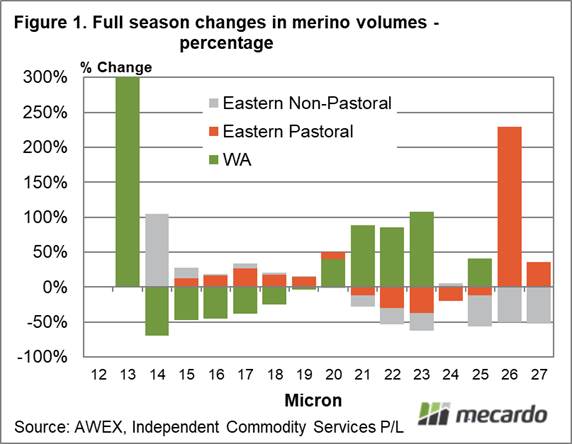

The 2021-22 season was interesting in due to the marked change in supply going on in Western Australia which was opposite to the mild changes in micron volumes seen in the eastern regions. Figure 1 shows the change in sales volume by micron (12 through 27 micron) for merino wool only last season. The changes shown are the changes between the full 2021-22 and 2020-21 season for the micron category of the specified region. The regions are broken up into Western Australia, pastoral production zones in eastern Australia and the rest (non-pastoral zones).

While the increase in 13 micron volumes in Western Australia was the largest proportion change, it only involved two farm bales. Note how sub-19 micron volumes fell in the west and rose in the east. For the broader side of the merino micron range Western Australian increases were large (50-100%) while in the east they fell 50% for 22 to 25 micron. The broadening trend in Western Australia ran counter to the fining trend in eastern Australia.

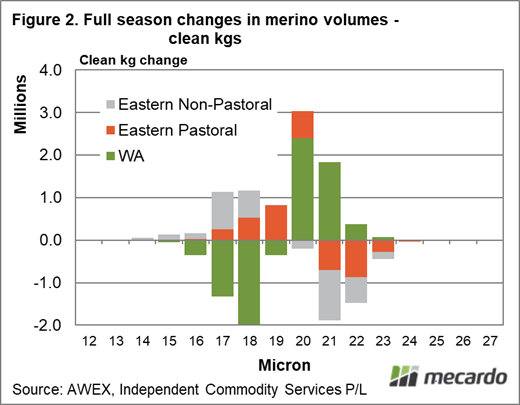

Figure 2 repeats the method of the first schematic but shows the changes in clean kg rather than proportional terms. This allows a direct comparison of changes by micron between regions and also puts the changes in some perspective of size. The counter trends of eastern and Western Australia are even more interesting in this graphic as it shows the change in Western Australian volumes out weighing the changes in the eastern clip despite the disparity in size (Western Australia accounts for about 16% of the Australian merino clip in clean terms).

In 2021-22 Western Australia pulled the supply of fine merino wool lower, increased the supply of 20 micron merino wool and held up the supply of 21 micron merino wool. That is an outsized influence on the national wool clip for Western Australia.

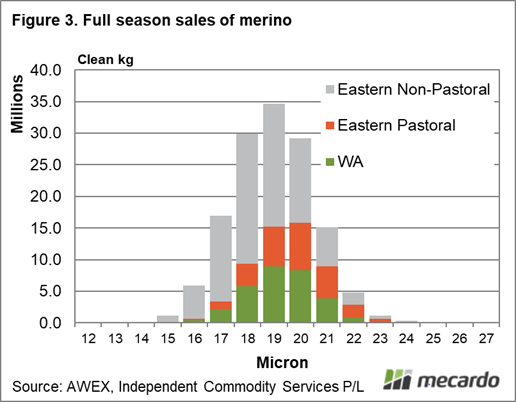

To provide a final supply perspective Figure 3 shows the full season breakup of merino sales by micron by region, in clean kg. The average merino fibre diameter for the season was 18.83 micron (19.2 micron in Western Australia, 19.6 micron in the eastern pastoral zones and 18.4 in the eastern non-pastoral zones). 98% of Australian merino sales in 20221-22 were between 16 and 22 micron with the eastern non-pastoral regions dominating the 18 micron and finer supply. For 19 micron and broader the supply more evenly spread between the three zones.

What does it mean?

Supply is not expected to be a factor in pushing the relative price of different micron categories around this season. Demand might wane and result in lower premiums (and discounts) for micron but supply will not be there to accelerate or retard this process.

Have any questions or comments?

Key Points

- Changes in micron trends in Western and eastern Australia ran in opposite directions in 2021-22.

- Falls in the western sales of fine wool pulled overall sales slightly lower, while increases in western broad merino sales held volumes up.

- The swing broader in the western clip is running out of steam and the eastern clip fibre diameter is not changing much at present so there are not big swings in supply of broad or fine merinos on the horizon from micron changes.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: AWEX, ICS, Mecardo, Agsurf