The rainfall flooding NSW this week is causing all sorts of problems in coastal areas, but on the other side of the divide, it is likely most welcome. In cropping country, the moisture will be banked, and couldn’t provide a better start to the cropping year. With new crop prospects as good as they can be at this time of year, we take a look at whether it’s time to start pricing.

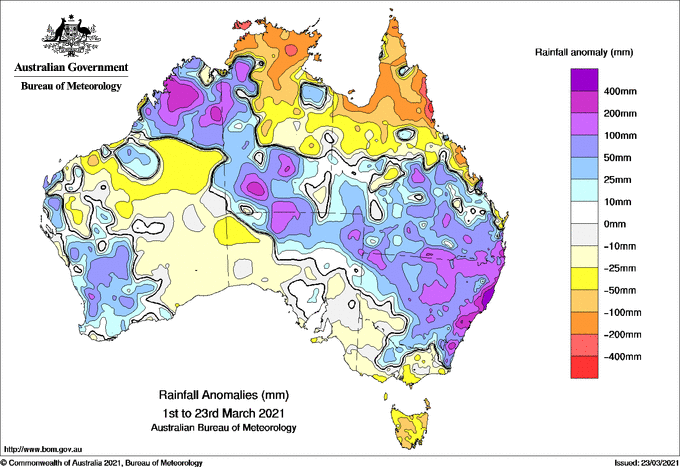

Figure 1 shows just how much rain has fallen in NSW for this March, but mostly this week. Most of NSW cropping country has received 50-100mm more rain than the monthly average, and it will give croppers a great start to the season.

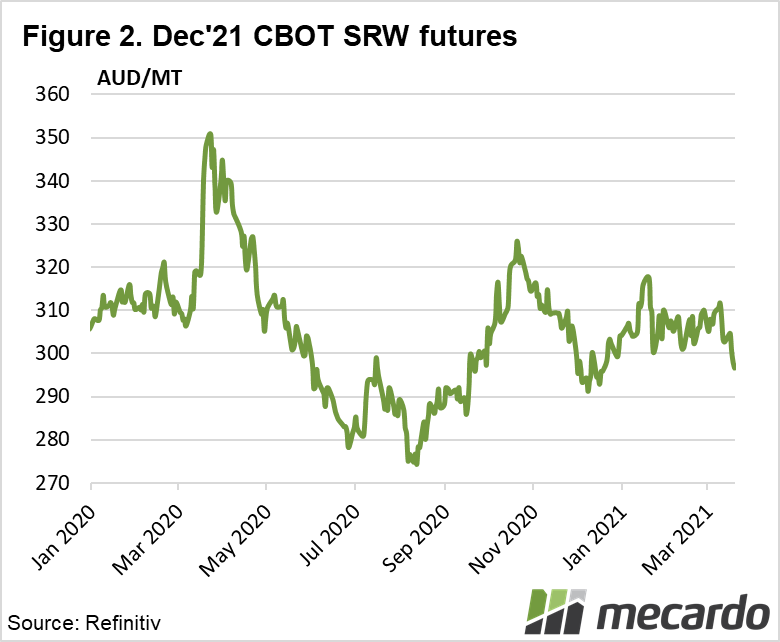

While US wheat futures have fallen in the last month, the hedging window is still open. Chicago Soft Red Wheat Futures (SRW) have fallen on the back of easing production concerns, but remain relatively strong.

Figure 2 shows the fall has taken Dec-21 futures from $308/t to $296/t, before rallying back to $300 on Wednesday, with some help from a lower Aussie dollar. It’s not unusual for futures to fall at this time of year. Northern Hemisphere crops are coming out of dormancy, and uncertainty around condition is dwindling. As such, more sellers come to the market, looking to lock in historically good prices for harvest.

Traditionally, Australian croppers miss out on the height of uncertainty, and strong international prices, as they wait for an autumn break and sowing before looking to do any pricing. Historically the best time to sell futures is in the first quarter of the year, unless of course, there are serious issues with northern hemisphere crops.

There doesn’t seem to have been any increase in new crop selling with the rain. The forward price basis for new crop multigrade wheat contracts to SRW remains steady, albeit at the relatively low levels of parity to minus $5. The bumper crop we’ve just seen saw the weakest basis levels at minus $10-15 for APW, so locking in physical prices would just be eliminating basis upside, with little downside to protect.

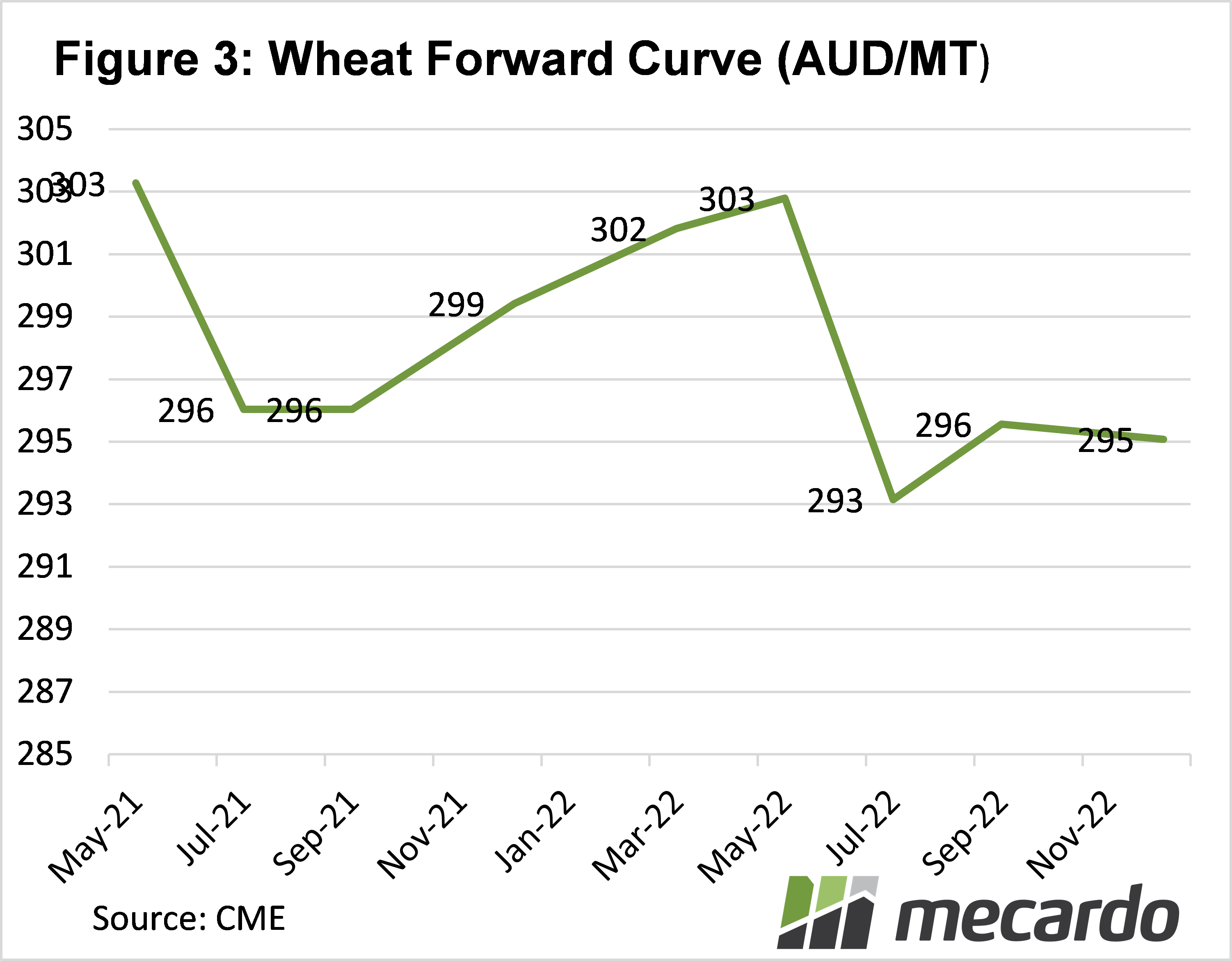

Figure 3 shows the forward curve for the SRW Futures contract in our terms. The uptick this week sees swaps available for Dec-21 at, or very close to $300/t.

What does it mean?

Hedging before the crop is even in the ground is usually a stumbling block for many producers. However, with the moisture profile building, it is a good time to have a look at that first sale, if nothing has been done yet.

It is worth remembering that if the price rises, most of the crop will appreciate with it, but if the market follows the seasonal pattern downwards to June and July, there has been something priced close to $300/t.

Have any questions or comments?

Key Points

- With rain falling across much of the east coast, cropping country production prospects are good.

- Chicago SRW swaps are still close to $300/t for Dec-21 and are better value than physical prices.

- It is a good time to make a start on a hedging strategy, with good prices and plenty of moisture.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: BOM, Mecardo