This week in lamb saw prices mostly track lower on the back of what appears to be more demand than supply at the moment. The exception is mutton however, which has held its own against the downward trend.

The national sheep and lamb indicators were mostly red this week, with falls right across the board, bar mutton. Heavy lambs lost 18¢(2%) to 783¢/kg, while trade lambs shed 12¢ (2%) to settle at 803¢ and merinos fell back 18¢(2%) to end the week at 718¢.

Restockers were pummelled the worst though, sacrificing 40¢(5%) to plummet down to 845¢.

The national mutton indicator bucked the trend however and gained 3¢ to end the week higher at 531¢.

Some prices in NSW went against the trend however- with the Merino indicator there climbing up 12¢(1%) to 746¢, while mutton gained a solid 25¢(4%) to reach 620¢

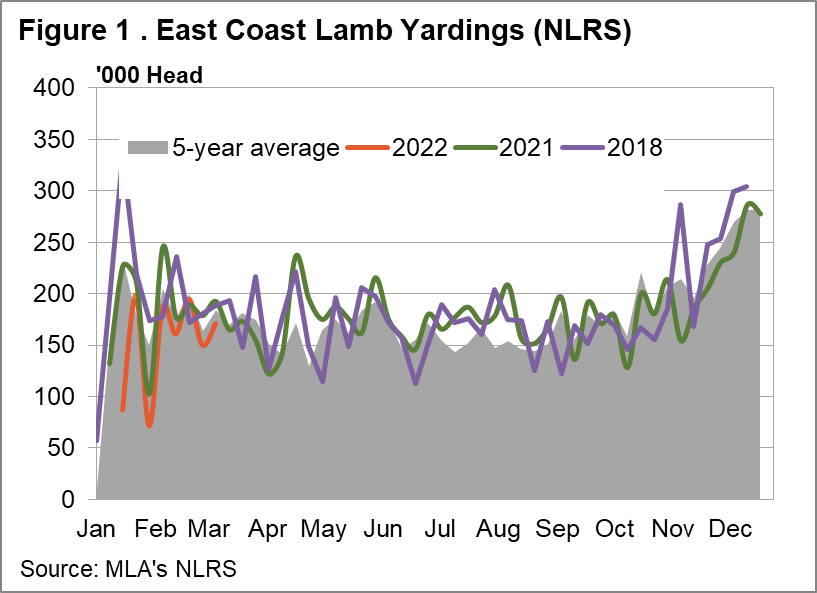

Lamb slaughter edged up 2% to 341,617 from last week, while sheep slaughter backtracked slightly by 1% to 98,665 head. There is no indication yet that sheep and lamb export processors are being presented with the same cold chain congestion difficulties as their northern beef processor counterparts, as the port of Brisbane which is causing the problems for the beef industry is not a significant outlet of export lamb.

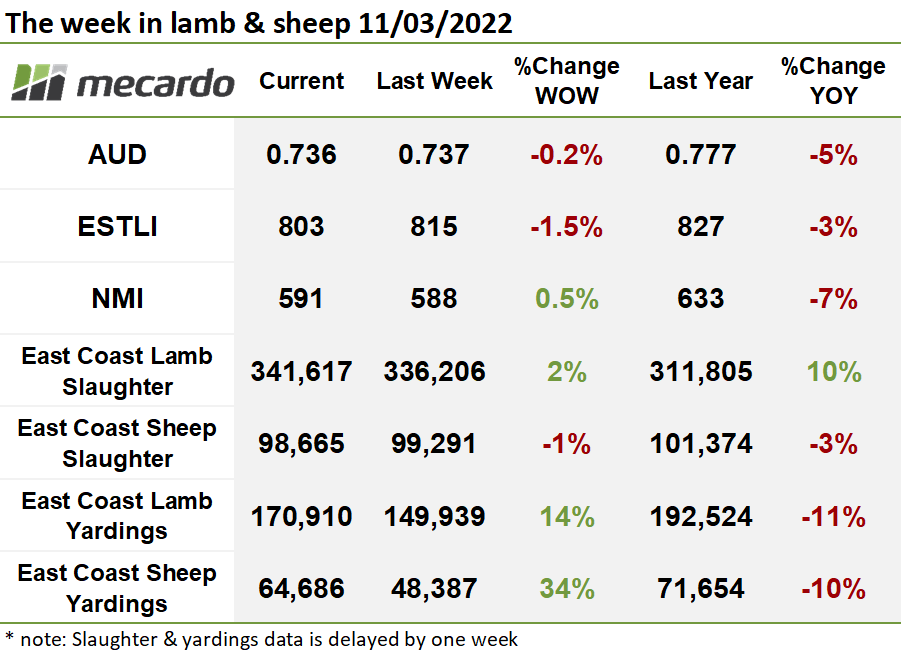

Last week’s yardings data revealed a substantial increase in supply of both lamb and sheep, with east coast lamb yardings up 14% to 171K head, and sheep numbers lifting 34% to reach 65K head.

NSW proffered an additional 20K lambs onto the market, accounting for the majority of the overall national lift, while sheep supply was uniformly higher across the states, with NSW, VIC and SA producers sending 30-40% more sheep than last week to market.

Looking at the historical yardings tends, increased numbers at this time of the year do not appear to be anything out of the ordinary.

The eligible yarding numbers for the national indicators provide a bit of a sneak peak at what the supply situation was this week. Across the board, volumes were down 20% on last week, particularly heavy lambs, which shed 11K head to 42,765. The price falls we have seen this week suggest that demand is weak compared to supply at present. Mutton was a different situation, with yardings lower this week than last, yet prices still retained firmness.

The week ahead….

This week saw prices fall across most categories of sheep and lamb despite probable lower supply than what we saw last week. This isn’t great news, as it suggests that supply is exceeding demand, creating overall downward pressure on price. If sentiment doesn’t change next week, or yardings fall substantially, A bit of a dip in market prices for lamb next week won’t come as a surprise, but the mutton market is looking relatively strong in comparison to lamb.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: MLA, NLRS, Mecardo