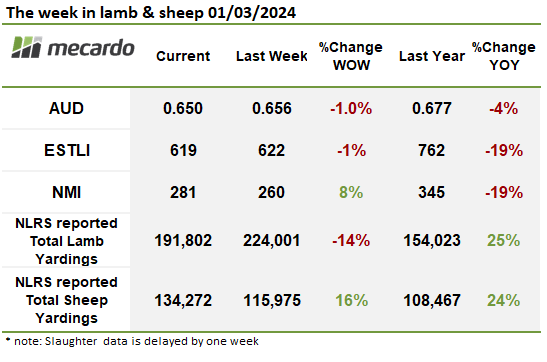

Movement in the sheep and lamb markets was minimal this week, with most indicators either holding firm or falling slightly. Mutton and restocker lambs showed some resilience for the week, but prices across the board remain well below month-ago levels. Yardings climbed back up following last week’s decline, and the latest slaughter figures are still historically very strong. This is set to continue, with Meat & Livestock Australia’s projections for the year forecasting lamb production to reach record highs, and mutton slaughter is also set to lift.

Despite a more than 40,000 head increase in

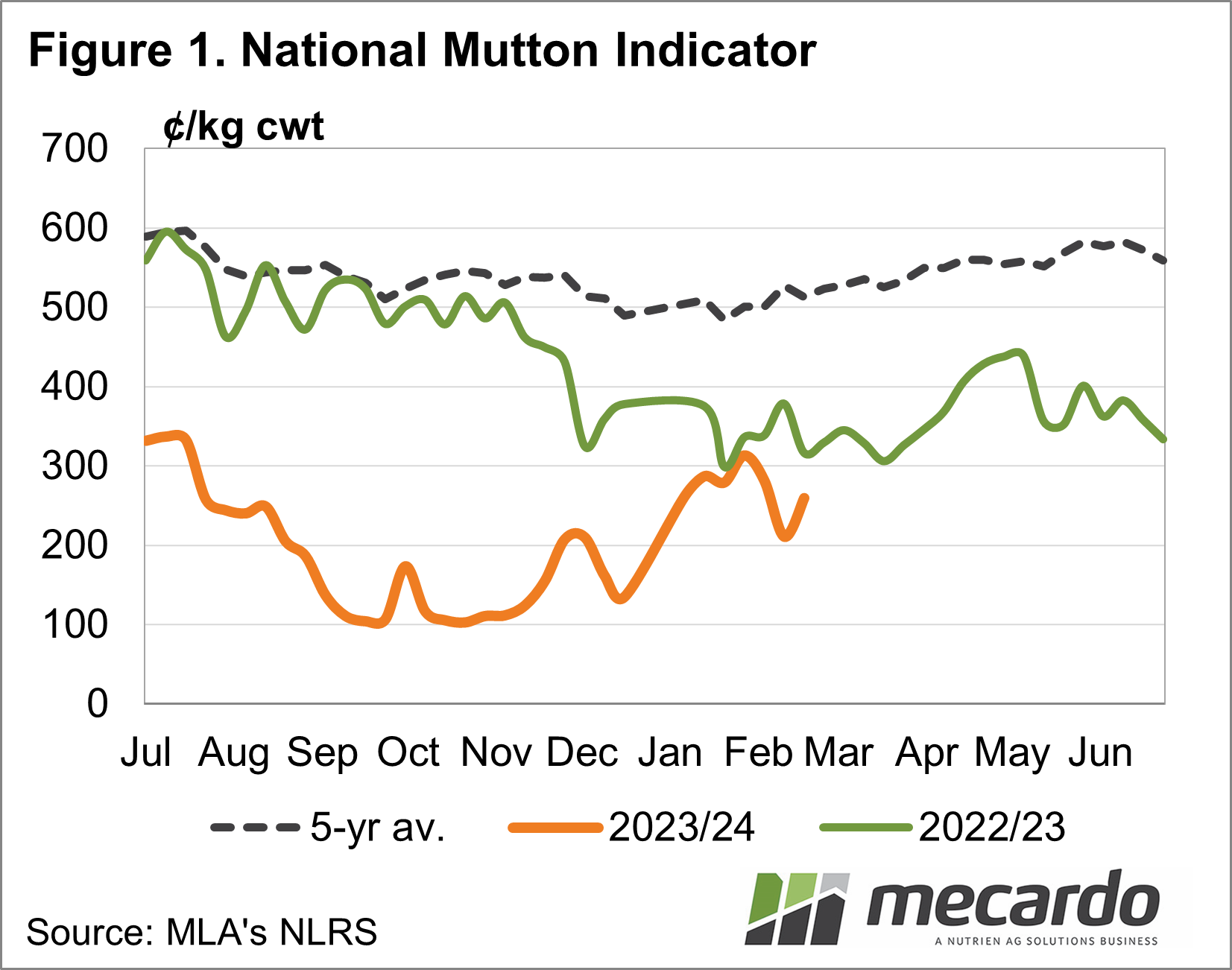

throughput numbers, the National Mutton Indicator just held on this week,

increasing by 20 or so cents from last week to finish at 281¢/kg. This

represents a 70¢/kg rise from where it bottomed out 10 days ago, and its lowest

point of 2024 so far. It’s currently operating at a 60¢/kg discount from the

same time last year. Hamilton, Victoria, and Wagga Wagga, NSW, had the two

biggest yardings of mutton and both operated at well below the price average of

the NMI. In contrast, Forbes, NSW, had the third-largest yarding and averaged

nearly a whole $1/kg above the average price. According to the National

Livestock Reporting Service, numbers of all categories of mutton increased at

Forbes, but good quality and strong competition had prices jump $15-$20/head.

Lamb prices remained lacklustre, continuing

the gradual decline they’ve been experiencing since the end of January. The

National Trade Lamb Indicator was averaging 615¢/kg today, having lost 88¢/kg

for the week. The Eastern States Trade Lamb Indicator isn’t trading much

better, at 618¢/kg, which is about 150¢/kg lower than the same time last year.

It is, however, still a $2/kg improvement on where the ESTLI sat back in

September. Ballarat, Victoria, yarded the most lambs this week and averaged a

5¢/kg premium to the average, but Wagga Wagga and Hamilton yarded almost as many,

and both traded at a discount. Forbes had more than 6% of the ESTLI throughput

and again bucked the trend, with prices well above the average at 666¢/kg.

Heavy lambs have lost $1/kg since January,

continuing to dip this week, and now sit at the largest discount to year-ago

levels of all the lamb indicators. At 617¢/kg, it is now back in line with the

ESTLI, having spent much of the past six months trading at a premium to it.

Wagga Wagga made up a big majority – 42% – of the heavy lamb indicator eligible

stock, and averaged just 580¢/kg, and was the primary yarding dragging prices

back. Light lamb prices fell 33¢/kg to 527¢/kg, while Merino lambs lost 35¢/kg

to land at 502¢/kg. These two categories were the only ones that had less

throughput week-on-week.

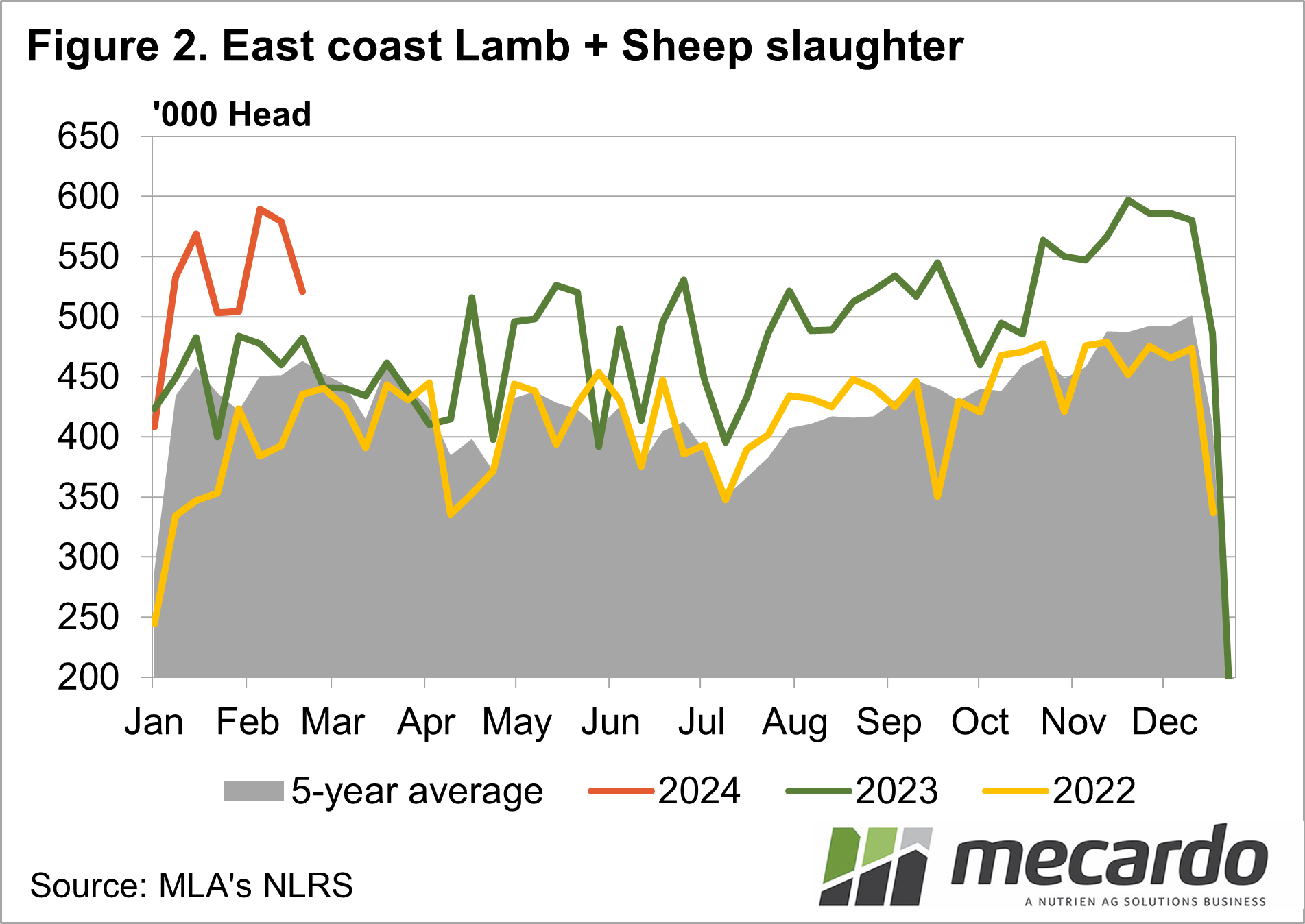

Total sheep and lamb slaughter fell by

more than 50,000 head last week, after the previous week reached historical

highs, but remained nearly that many – or about 9% – above the same week in

2023. Breaking that down, lamb slaughter was about 73,000 head, or 20%, higher

year-on-year, while sheep slaughter reflected the corresponding week’s lower yardings,

falling more than 30,000 head for the week and sitting nearly 14% lower than

the same time last year.

The week ahead….

Autumn has arrived, and historically sheep and lamb prices start to find some strength before peaking during winter. Seasonal conditions have been kind to most sheep-producing areas; however, it has dried off quickly, and we could be looking at continued high turnoff until the rain starts again. Slaughter volumes are seemingly able to keep up at the moment, which should mean little downside, but we might not see much upside this month either, with plenty of supply still around.

Have any questions or comments?

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: MLA, Mecardo