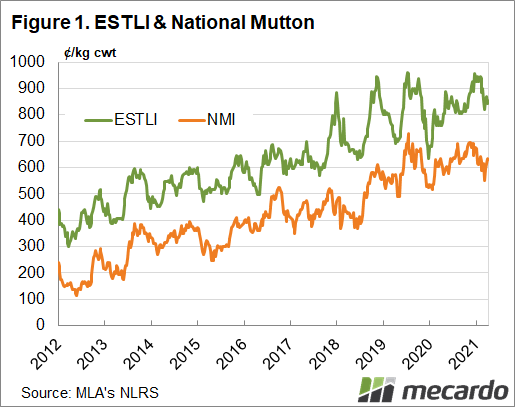

The mutton price has fallen since its mid-year peak, but remains resilient against increased supply, and the lamb price. The National Mutton Indicator is averaging 638¢/kg for the year-to-date, its highest annual average on record, and 31¢/kg stronger than the previous 12 months. An increase in sheep slaughter indicates the flock rebuild has reached a level that allows for more cull and adult sheep turn-off, and the extra numbers are finding plenty of demand from export markets, while restockers are also still willing to pay plenty for replacement breeders.

The eastern states saleyard price for mutton is averaging 651¢/kg for the year-to-date with limited trading days left in 2021, which is 18¢/kg, or 3% above last year’s average. The average national over-the-hooks price for medium mutton is significantly lower, at 625¢/kg for 2021, but has experienced more of an increase, up nearly 9% on the 2020 price. As mentioned, the NMI is at an average of 638¢/kg, up 5% on the previous year, and set to break the record annual average for the third year running. In the past month the NMI has gained nearly 80¢/kg, and has only been higher once since the start of September.

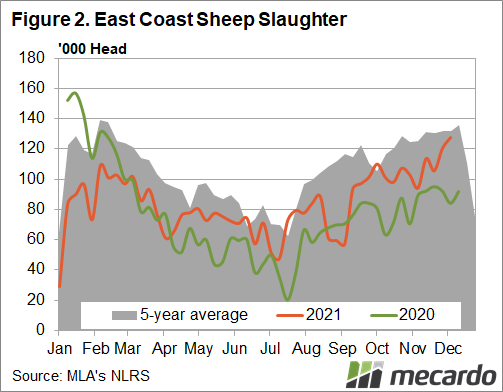

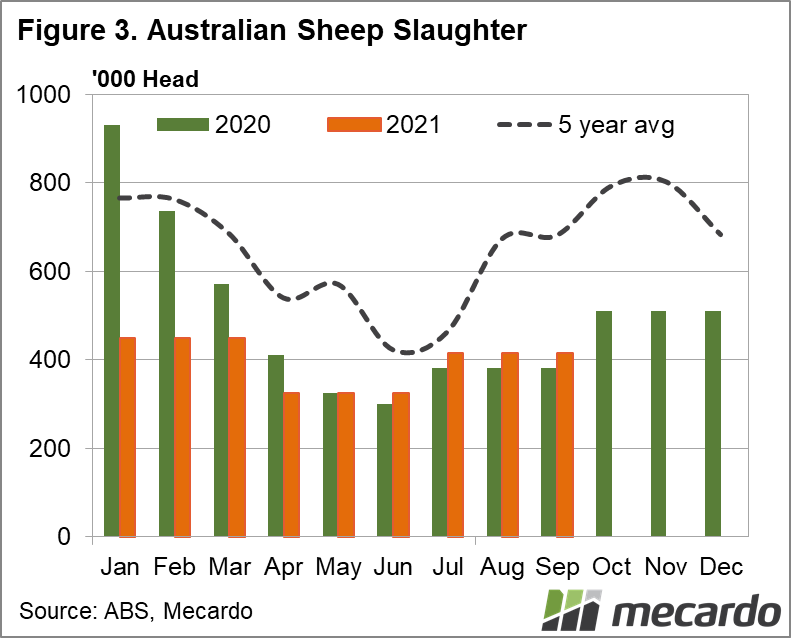

September quarter data released by the ABS last month shows sheep slaughter climbed to 1.25 million head, up 28% from the previous three months, its highest point since the March 2021 quarter. And according to Meat and Livestock Australia weekly figures, east coast slaughter numbers have remained higher year-on-year for the past two months as well and are currently around 10% higher than 2020 for the year-to-date. For the first week of December, east coast sheep slaughter rose 6% for the week, and was 51% higher than the corresponding week the previous year. The national mutton indicator didn’t mind however, finishing last week at 634¢/kg, up 2¢/kg for the week and 6% year-on-year.

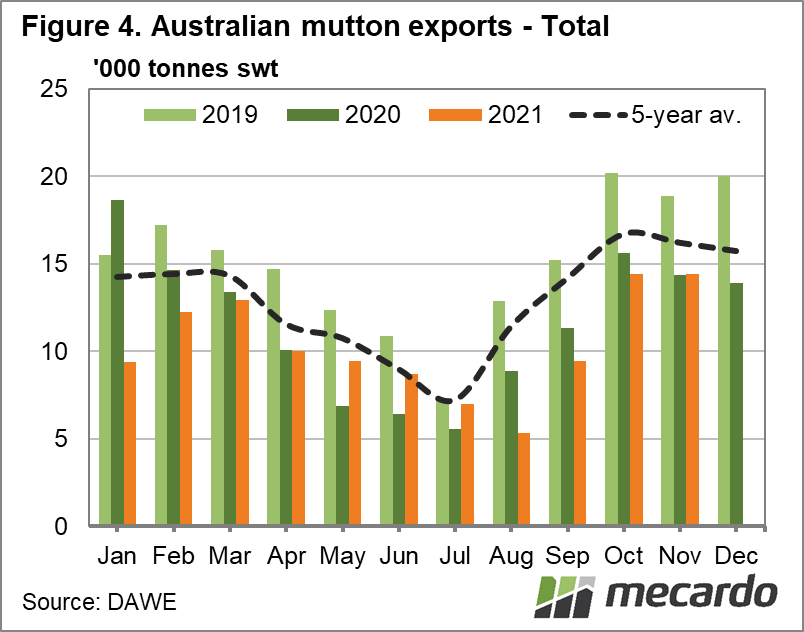

Export demand has strengthened, despite mutton exports to November are tracking 1% lower year-on-year, having been impacted by Covid-19 driven freight and demand restraints in key markets in the Middle East early on. However, exports to China and US have risen in the period, up 6% and 24% respectively. Total Australian mutton exports for November were up 15% compared to the same month in 2020, and in fact monthly exports volumes have been on-par or higher year-on-year for nearly every month since May, with October being the exception. Mutton exports destined for the US were up a whopping 149% in November – and this was the smallest monthly year-on-year increase to the US since July, with both August and September volumes more than 200% up.

What does it mean?

With more export markets moving towards their Covid-normal trading, and rainfall tallies and outlooks favouring livestock farmers, money for mutton won’t feel any extreme downward pressure in the short term. While the gap between the NMI and the Eastern States Trade Lamb Indicator has closed to about 25% in the past two weeks, it is still well above the 17% gap in June and the 18% gap at the same time last year, indicating there is room in the sheep market. We will look at what the La Nina might mean for mutton over the coming year later in the week.

Have any questions or comments?

Key Points

- Money for mutton holding above year-ago levels, with the NMI set to average 5% higher for the year.

- Sheep slaughter has climbed in the second half of the year, to the highest levels since flock rebuild began.

- Export demand also making up for a slow start to the year, up 15% in November.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: ICS, Mecardo