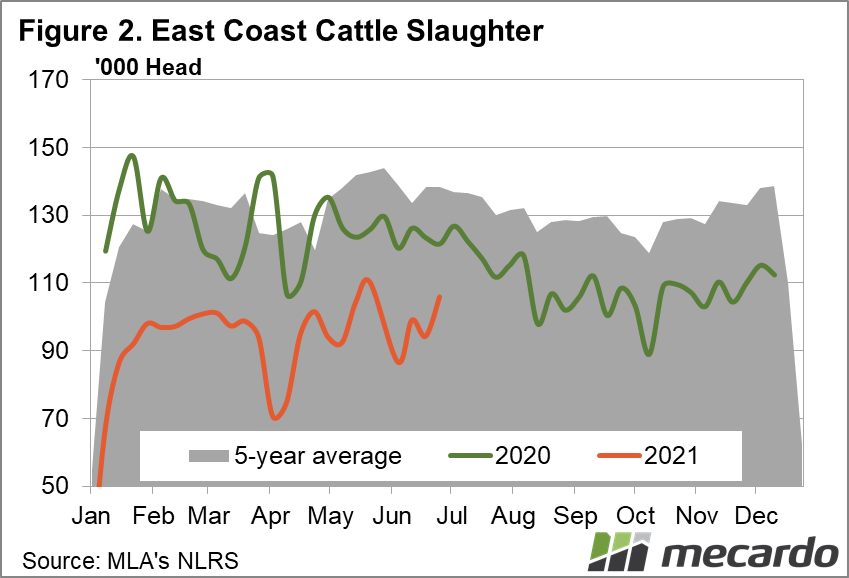

The cattle market finished the end of the financial year on a strong note, with robust demand from restockers and feeders continuing to corner the market. This pushed the Eastern Young Cattle Indicator to a new record of 942ȼ/kg cwt, while the 90CL beef price remains firm. Despite this exuberance, the National heavy steer price plunged 6%, which is worth keeping a close eye on.

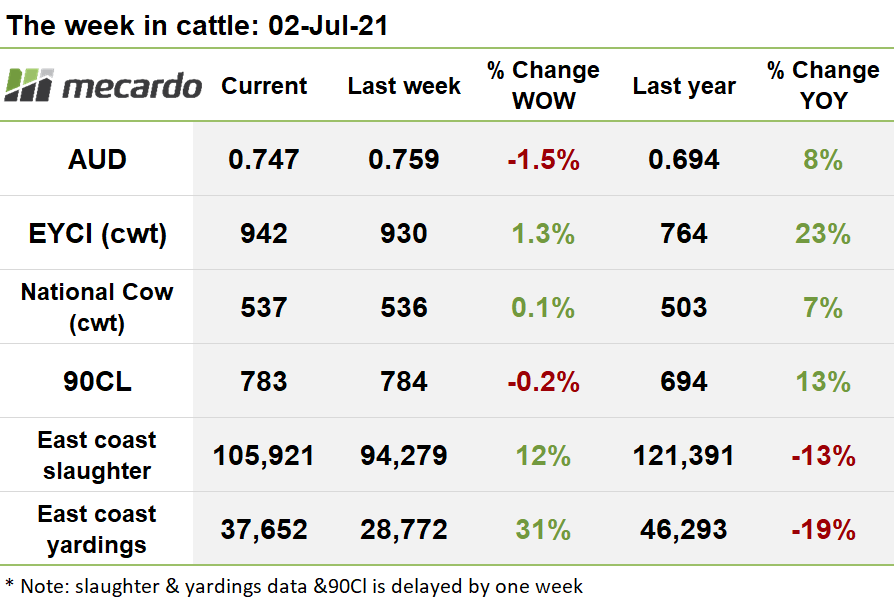

After a slight delay, the seasonal pickup in offerings to the saleyards as we approach the end of the financial year finally came to fruition, with yardings rocketing up 31% last week. All states saw a substantial surge in numbers put to market, but the most enthusiastic change came from NSW, which was up 57%, followed by VIC, which booked a 31% increase. A total of 37,652 head were yarded on the east coast for the week ending 25th June 2021.

AuctionsPlus yardings remained roughly on par with the prior week, at 14,405 head, and high clearance rates in excess of 90% were maintained for young cattle.

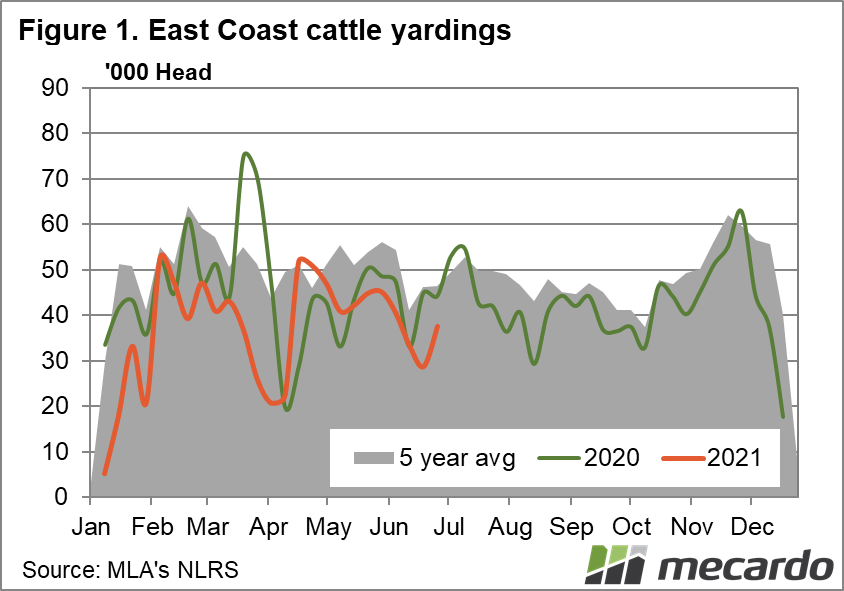

East coast slaughter also picked up the pace last week, up 12% from the week prior. QLD was the main contributor to the rise, gaining 14%, and it was backed up by VIC and NSW which respectively saw 20% and 7% increments. Overall, 105,921 head of cattle were slaughtered in the week ending 25th June 2021.

The Eastern Young Cattle Indicator (EYCI) just keeps stretching towards the stratosphere. The number of eligible cattle sales contributing to the index remains relatively low, at 9,317 head, with the high prices reflecting the tightness of the market, and persistently strong demand for young cattle. For reference, we were seeing volumes upwards of 15k a couple months ago. As usual, the rise was still lead by the northern selling centres which with Roma Store achieving average prices of 959ȼ/kg cwt, and Dalby 923ȼ/kg cwt- combined these two yearling focused saleyards represented 38% of EYCI volumes. Further south, Wagga recorded an average of 981ȼ/kg, with almost 800 yearling steers fetching 998ȼ/kg.

The stronger slaughter numbers clearly influenced the national indicators, but demand may also be impacted by the recent COVID-19 resurgence, as supermarkets take sales from foodservice.

The National indicator for processor steers lifted 19ȼ (4%) this week to 459ȼ/kg lwt, and medium steers followed, also surging 19ȼ (5%) to 417ȼ/kg lwt. Vealer prices followed the trend, advancing 13ȼ(3%) to close the week at 541ȼ/kg lwt, while medium cows pushed up 9ȼ(3%) to 299ȼ/kg lwt.

The feeder and restocker indicators lost ground, however, dipping 4ȼ (1%) and 1ȼ (<1%) to finish the week at 459ȼ/kg lwt and 555ȼ/kg lwt respectively. The wooden spoon for the week goes to heavy steers, which plunged 25ȼ (6%) this week to finish up at 384ȼ/kg lwt.

The Aussie dollar plunged 1.5% over the week to close at 0.747US. The dollar followed the weaker trend experienced by commodity currencies generally, and expectation of the imminent release of strong US employment figures lending strength to the US dollar.

90CL frozen cow prices were relatively steady last week, closing down a smidgen to 783ȼ/kg swt, however, we can expect that this weeks decline in the Aussie dollar will provide support to the price when numbers are released next week. The lead-up to the US independence day holiday later this week is likely to have provided a boost to demand, so some quieter weeks ahead in the US markets are on the cards.

The week ahead….

A solid 10-50mm of rain can be expected down a good proportion of the east coast in the next week, especially further north in QLD will help to keep moisture profiles well charged and maintain producer confidence. History suggests that yarding’s could well continue to climb as we come into July, but the seemingly bottomless demand for young cattle should underpin prices with solid support. The sharp fall in the national heavy steer price this week is a dark cloud worth watching though, as expectations of final turnoff prices are a key factor sustaining the market’s willingness to continue to pay up for young cattle.

Have any questions or comments?

Click on figure to expand

Data sources: MLA, Mecardo, BOM