The wheat market began the new year with more of a stagger than any kind of billion-dollar strut. We suspect the losses in market prices were more a round of profit-taking and position squaring ahead of, and now post, the festive season.

In the short term, the ag commodity markets have a lot of weather ahead that needs to be considered. We are likely to see elevated concerns around production given the tight nature of global stocks and this should give support to commodity prices as we navigate 2022.

Case in point, South America remains in the spotlight. Rains returned to some of the drier regions of southern Brazil but the forecast has again turned hot and dry. Key soybean producing states of Paraná and Rio Grande du Sol have already suffered irreversible yield losses. StoneX (prev FC Stone Intl) have slashed their production estimates from 144mmt to 135mmt. Industry analyst, AgResource more recently came out with a 131mmt production number. For reference, Brazils national analyst CONAB has production at 143mmt.

Black Sea crop prospects are pretty good with SovEcon increasing Russian wheat production estimates to 82mmt. It is an early crow but the season is progressing nicely after some recent rain and snow and temperatures relatively mild for this time of year.

The USDA released their crop condition updates yesterday. Most noticeable was the significant decline in crop health, especially through the key winter wheat states of Kansas and Oklahoma. For Kansas, just 33% of the crop was rated good/excellent with 25% rated poor/very poor. This compares to the previous month’s figures of 51% g/ex and 14% p/vp. Crop condition at this time of year has a poor correlation to final yield, but does place more emphasis on a kind spring. The US has been experiencing some pretty wild weather over the past couple of weeks, ranging from extreme wind, bush fires (in winter), tornadoes and blizzards.

Next week…..

It also looks like we will be dealing with some of the same macroeconomic issues in 2022 that we wrestled with through 2021. COVID-19 is still the elephant in the room, inflation, oil and energy prices, fertiliser cost etc etc. Throw in escalating geo-political tensions in the Black Sea, as well as China, could all make for a very interesting couple of months.

Have any questions or comments?

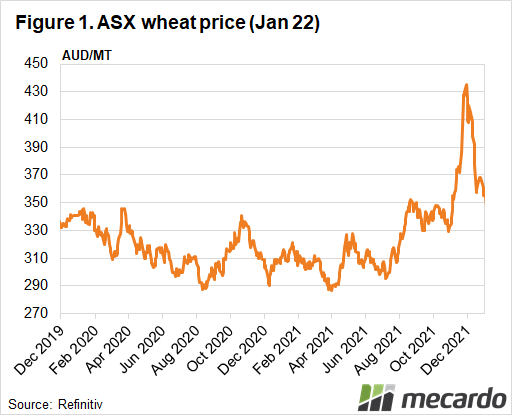

Click on graph to expand

Data sources: Refinitiv, Mecardo