The demand for RWS accredited wool continues to develop, with large premiums paid in the greasy wool market in South Africa, Australia and presumably also in both New Zealand and South America. This article takes a look at Australian premiums for non-mulesed and RWS merino wool (albeit including New Zealand wool sold in Melbourne).

RWS accreditation is concerned with animal welfare and not with wool quality, so determining the effect of RWS accreditation on all lots is not practical as the range of wool qualities runs the full gamut of what is produced. In this article wool for comparison is restricted to categories where there is sufficient volume to give some confidence of the price effect identified.

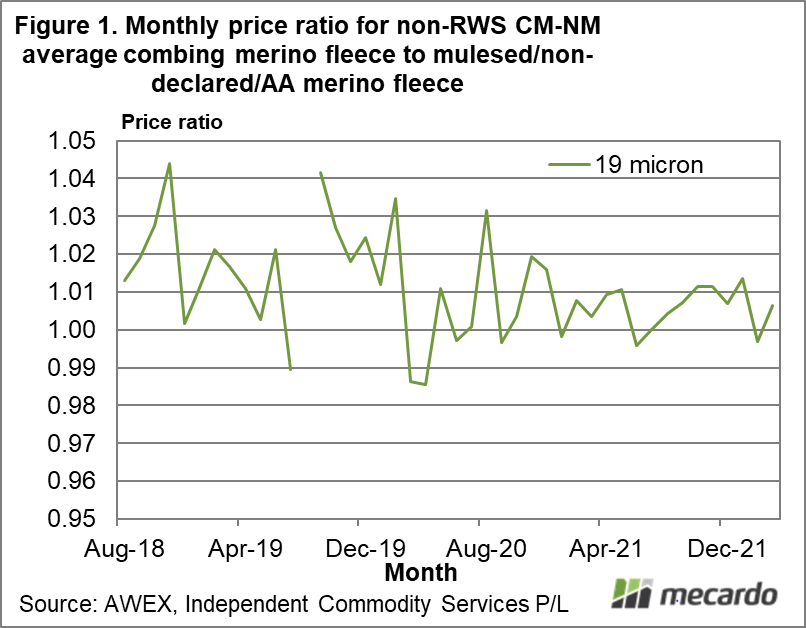

A lack of mulesing is a critical part of RWS accreditation for Australian farmers. Non-mulesed wool has been identified in sale catalogues since 2008. Figure 1 shows a monthly ratio for 19 micron fleece wool declared to have ceased mulesing or be non-mulesed compared to wool which had no declaration or was mulesed. The series include average combing fleece (less than 2% vegetable fault, sound, eastern selling centres only, no subjective fault, no interlots or bulkclass) which covers a wide range of qualities but we are looking for a trend in the data. The graphic runs from mid-2018 to this month, with a median ratio of 1.01, which is a 1% premium. The ratio jumps around, partly due to the nature of the price series, with perhaps a small trend to a lower level in the past couple of seasons.

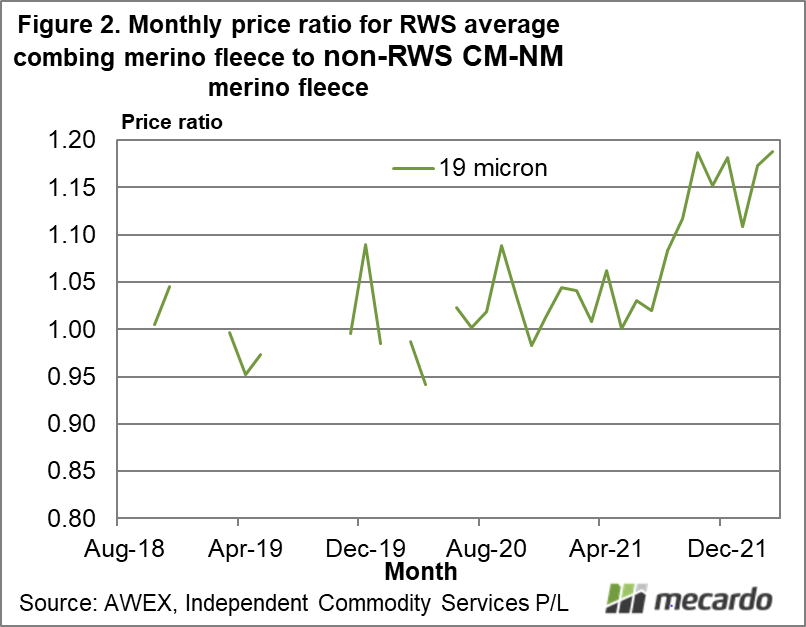

Figure 2 repeats the analysis; this time comparing RWS accredited 19 micron fleece wool to CM-NM non-RWS fleece wool. There are plenty of gaps in the period to mid-2020 reflecting minimal supply of 19 micron RWS wool in Australia. Up until mid-2021 there is no great trend in the ratio. In October 2021 (when Cape Wools began to publish RWS premiums for wool sold at auction in South Africa), the ratio suddenly jumps to the range of 1.15 to 1.2 (a premium of 15% to 20%). This time last season there were some premiums in the market for RWS wool, averaging around 4%. Now the premiums are around 15% to 20%. It has been a quite a change in the price structure for the greasy wool market.

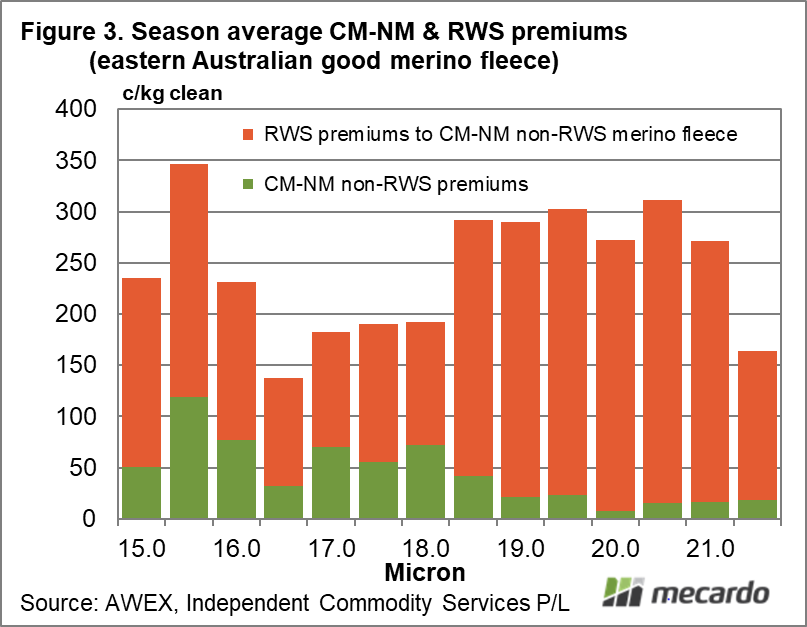

To get around the variation in calculated premiums Figure 3 shows median premiums in cents per clean kg for non-RWS CM-NM and RWS accredited good quality merino fleece (38+ N/ktx staple strength, 70-110 mm, 0-1.5% vegetable fault, eastern selling centres, no subjective fault, no ASF lots and no New Zealand lots) by half micron. The CM-NM premiums are shown at the bottom as it assumed the RWS lots will pick up this premium. The methodology is not perfect so do not assume 15.5 micron is receiving 200 cents extra premium to 16.5 micron – look for the average which is in the range of 200-250 cents for the finer micron categories and 250-300 cents for the broader micron categories.

In Figure 3 the finer micron categories have a smaller calculated premium compared to the broader categories. This is quite possible as the finer micron categories are currently trading with extreme micron premiums, so adding substantial premiums on top of these prices will be stretching demand.

What does it mean?

From a small, variable premium in the greasy wool market RWS has emerged as a large premium this season. While some 28% of the South African clip since September has been accredited to RWS, in Australia the volumes remain small. For March to date only 2.2% of merino fleece sold at auction has been accredited RWS. The high premiums currently in the market continue to be paid on small volumes. The question is what happens when the volume increases markedly.

Have any questions or comments?

Key Points

- There has been a sea change in RWS premiums this season.

- Non-RWS CM-NM wool continues to receive small premiums on average.

- In cents per kg terms the broader merino micron categories are receiving higher premiums than the finer micron categories.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: AWEX, ICS, Mecardo