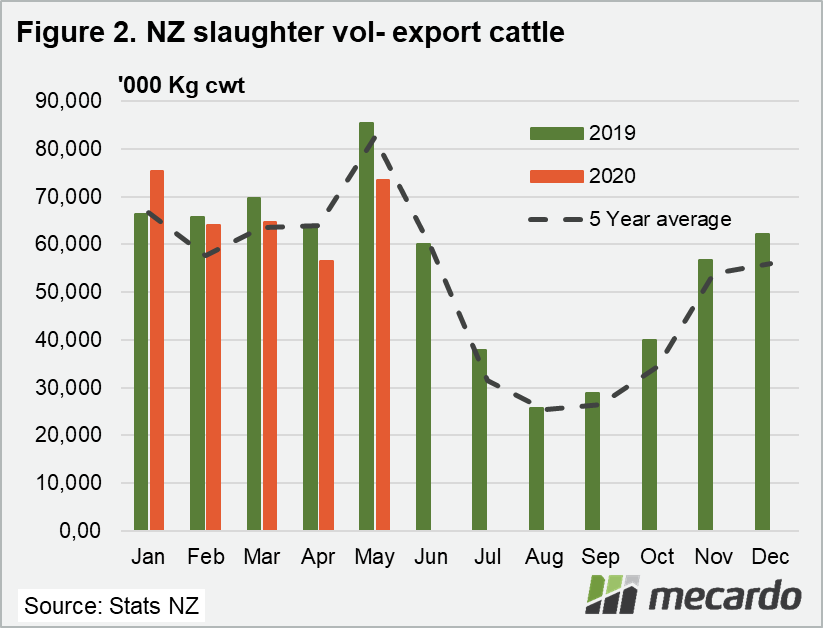

The highly seasonal Kiwi slaughter cycle suggests that New Zealand beef export potential will most likely halve over the next few months, with export-grade slaughter already at a historically low level this year as it is. With NZ a significant competitor in Australia’s key export markets such as the US, this reduction in supply will help support export beef prices. Competition from Mexico is rising, however.

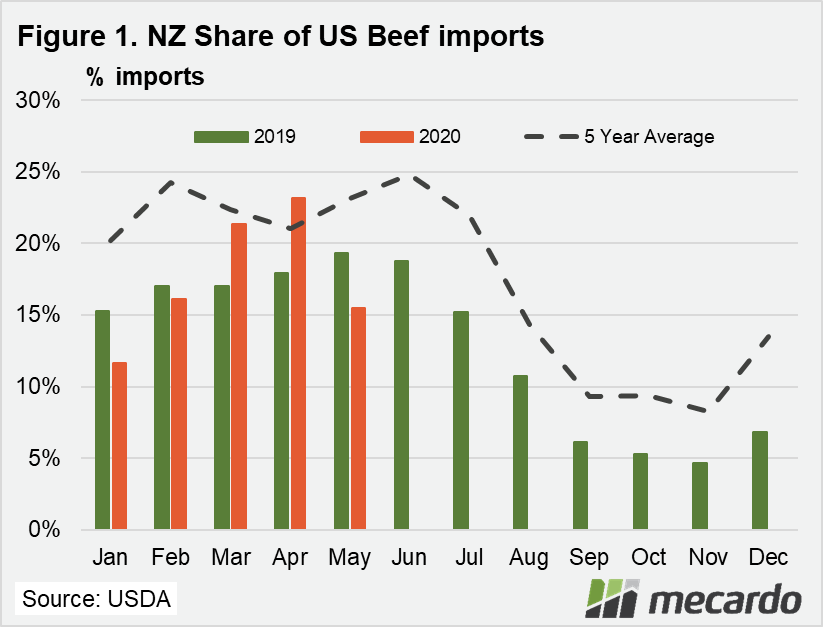

NZ accounted for 15% of US beef imports in May , (Figure 1) with Australia at 17%.

NZ’s US market share typically dips down 50% come August, in line with its steep seasonal decline in slaughter numbers until recovery in the new year (Figure 2).

As such, the drop in available NZ product should help soak up the impact of increased supply pressure from Australia in November, when yardings typically pick up again.

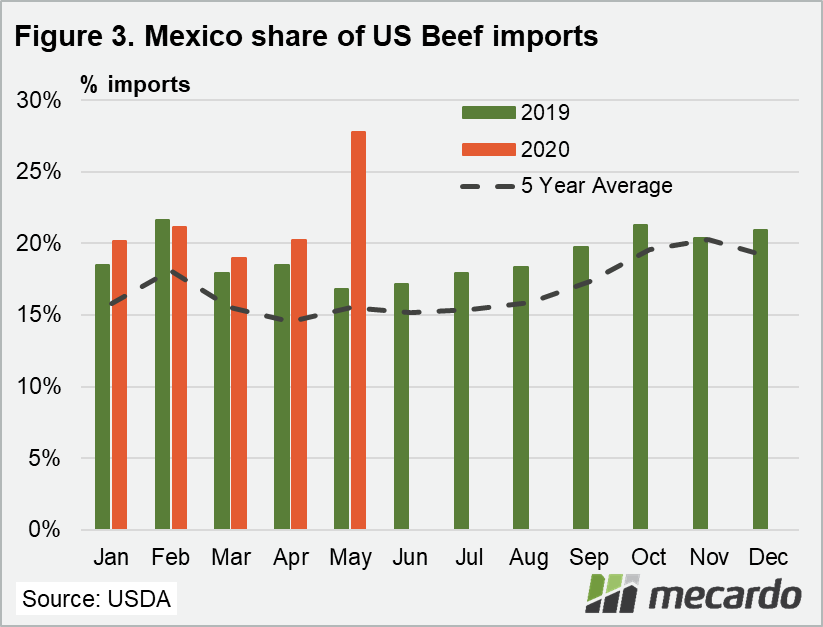

A new development in the US export market is that Mexico’s prominence is rising though, reaching an all-time high of 33,845 metric tonnes in May, or 28% of total US beef imports (Figure 3).

The Mexican story looks like an important factor to watch as US destined export volumes and market share have been well above average and trending steadily higher since the start of the year. Conversely, Australian export volumes and market share have been falling.

A recently weakened currency provides an advantage for Mexican exports to the USA, where the peso has lost over 17% against the US dollar since March 2020, having slid from 18.61 peso /US to 21.96 peso /US. The devaluation is driven by a poor economic outlook in Latin America generally, plus Mexican central bank rate cuts, and the country’s economic dependence on oil revenue.

86% of Mexican beef exports are destined for the US, representing around 17% of US beef imports on average, but also services the Japanese and Asian markets to a minor extent.

According to the USDA, Mexico maintains a herd of around 17 million head of cattle, with the southern states of Mexico employing grass-fed beef production systems, producing a lean, low-fat product similar to Australia’s. Other areas produce grain-fed feedlot beef of small size cuts of the style that appeals to the US market, and is marketed as a healthier alternative. Mexican exports have historically focused on the higher value cuts such as loins and sirloins, however. The USDA forecasts Mexican beef exports to rise around 50% to 463,000 MT cwt by 2025.

Under the USMCA, or NAFTA 2.0 free trade agreement, Mexico enjoys continued unrestricted access to US beef markets, tariff free, also comparable to Australia’s arrangement with the US. Mexico is also a significant importer of over 230,000 MT p.a. and rising, of mostly cheaper beef cuts from the US, but Australia’s opportunity and access to this emerging market are limited by steep 14-18% tariffs, according to MLA.

What does it mean?

NZ export volumes falling off sharply will provide support to beef imported into the US from August until December, until NZ slaughter begins to pick up again. However; Mexico’s contribution to US imports of beef is trending upwards, fuelled by a weak peso, and growing production.

Have any questions or comments?

Key Points

- NZ monthly export cattle slaughter numbers expected to fall 60% by August.

- NZ Beef export volumes wll also halve from August to December.

- US imports of Mexican Beef at record levels fueled by weak peso.

Click on graph to expand

Click on graph to expand

Click on graph to expand

Data sources: USDA, Statistics NZ, INEGI, NCBA, MLA, Mecardo