Early stage processor machinery is designed and adjusted to fit the average dimensions of wool produced. Wool, as a naturally produced commodity, varies from year to year in response to seasonal conditions so the supply chain adjusts its relative pricing to these supply changes. This article takes a look at discounts for over length merino fleece.

Mecardo looked at staple length in the merino clip last week, showing how the supply of long staple wool has increased in recent seasons, as eastern Australian wool growing regions have recovered from drought. The expectation is that with increased supplies of long wool, discounts for wool significantly longer than the average staple length will increase.

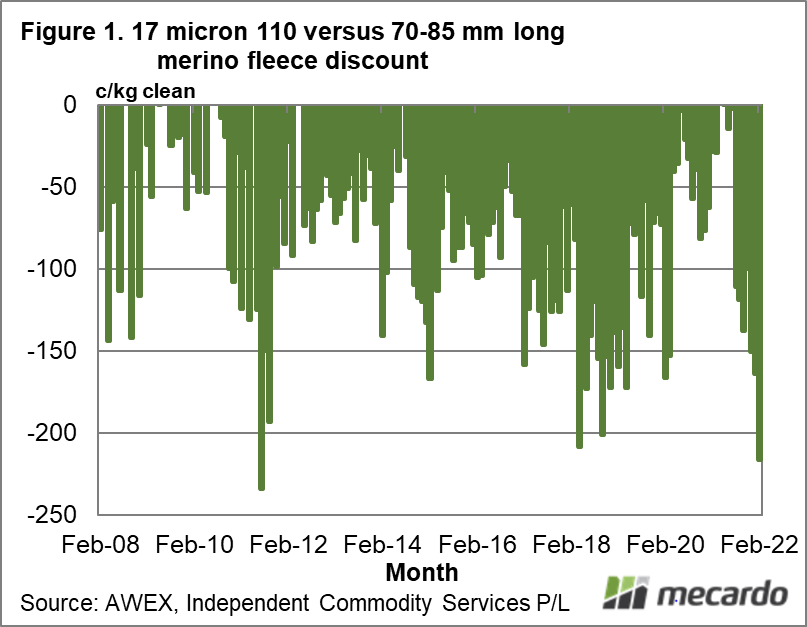

To look at discounts for long staple length, the data must be split into micron categories as what constitutes over length varies with micron (the average staple length becomes shorter as fibre diameter falls) in addition to varying levels of demand between micron categories. With this in mind Figure 1 shows the monthly average discounts in cents per clean kg for 17-micron, 110 mm long merino fleece in relation to 70-85 mm length fleece from 2008 onwards. The discounts have ranged from negligible levels to 200 cents, with the discount in February back up to over 200 cents.

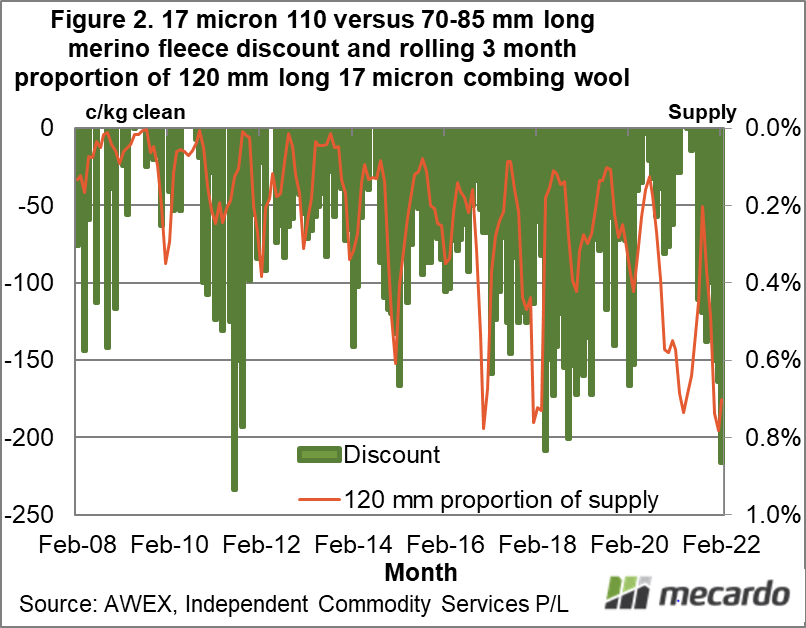

In Figure 2 we look at supply and discounts for over length wool in the 17 micron category. It shows the discount from Figure 1 along with a rolling three month average of the proportion of 120 mm length fleece of 17 micron combing length wool sold at auction. There are many periods where the discounts widen at the same time as the proportion of 120 mm (it is a small proportion) but there are also periods where the supply and discount do not seem to be linked at all such as in 2018 and 2021. Overall the correlation between the supply and discount shown in Figure 2 is low, so while change in supply is a factor in determining long staple length discounts, it is only part of the story.

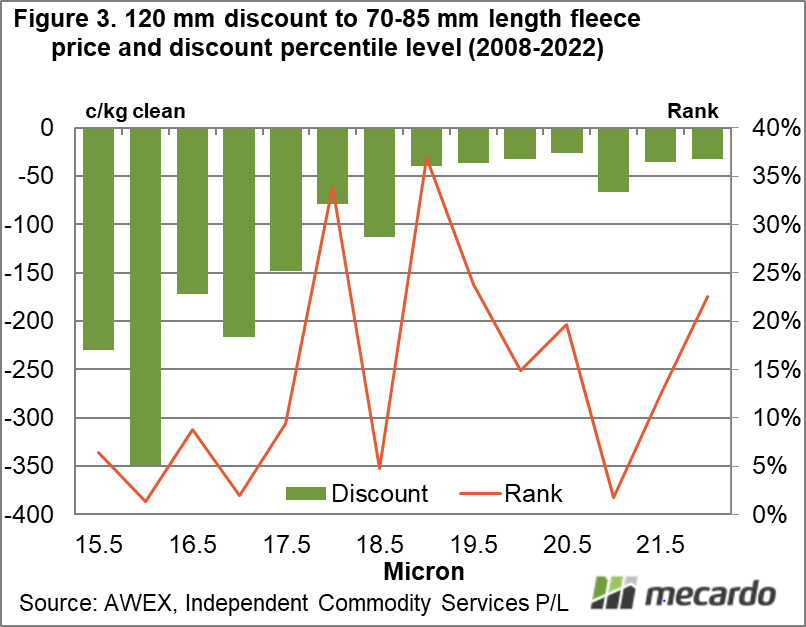

So how do over length discounts currently look across the merino micron categories? Figure 3 shows the discount for 120 mm length fleece versus 70-85 mm length fleece for February 2022 from 15.5 through to 22 micron, with the percentile rank (2008-2022) for each discount shown. For 19 micron and broader the discount is negligible in cents per kg terms, although only in the 15th to 35th percentile levels. Below 19 micron the discounts increase as fibre diameter becomes lower with the rank falling away to very low levels indicating an extreme discount.

What does it mean?

Over length discounts are more serious for fine wool where the average staple length has been historically shorter and the preferred staple length of European processors is tailored to shorter length wool. Discounts for fine merino are currently large with plenty of supply of the long wool although, for 17 micron at least, the supply of over length wool has a patchy record in explaining discount levels. Beyond 19 micron, on the broader side, over length discounts while relatively low in percentile rankings are not that large in cents per kg terms.

Have any questions or comments?

Key Points

- Discounts for over length sub-19 micron fleece are sizeable to very large at present, with the discount increasing as fibre diameter becomes finer.

- Discounts for 19 micron and broader are not that large in cents per kg terms.

- Changes in over length supply have a variable record at explaining changes in discounts.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: AWEX, ICS