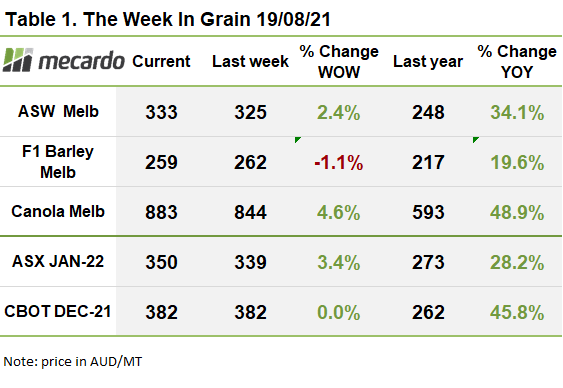

After the excitement of last week’s USDA report and the undeniably bullish enthusiasm it generated, this week has been a little more subdued. The past week has seen a fairly sharp correction with CBOT Dec ’21 giving up all its gains to be down 22ȼ/bu for the week In AUD terms however, the dip has only resulted in a $1.50/t correction courtesy of a sharply weaker AUD.

Bare in mind though, the fundamentals haven’t changed. Wheat, especially milling wheat, is getting tight. A broader downturn in commodities this week was the catalyst for speculative investors to lock away some profit. Gold, iron ore and crude oil all fell sharply as did most stock exchanges around the world on the back of weak economic data out of the US and China as well as surging COVID cases in Japan and Australia.

The question is how high can this market go? After last week, my gut feel was there was more upside but it was not infinite. Major exporter stocks are getting tight and that will add support to wheat prices until inventories can start to rebuild. Certainly, from a demand perspective, Australia is in the box seat in terms of supplying wheat and barley to the SE Asian buyers – which is a market we had lost some market share to the Canadians and the US during our drought years. The Middle East is another market that Australia should be well positioned to participate in. The fact that Canadian supply of high protein wheat will be short, is already seeing demand swing to Australia and the US for replacement origins. There will however, be a point that buyers slow down purchases because of price.

Europe is also having a horrid run with harvest weather. Already 25-35mm has fallen over France and Germany in the past week with more forecast to come. There are concerns that this will inevitably lead to low test weights and falling number issues.

The cash basis will have to do some of the heavy lifting if prices are to improve. As it stands, the cash basis in most port zones is heavily negative. This is because we are currently not seeing huge demand for new crop and the trade know there is a big crop coming (combined with some carryover old crop still available in WA and NSW). It may just take some time for this to flow through.

The week ahead….

As I said at the start, the fundamentals for wheat haven’t changed, but the moves in this week’s market serve to remind us that nothing can be taken for granted.

Have any questions or comments?

Click on graph to expand

Data sources: USDA, Reuters, Argus Commodities